A 401k is a wonderful thing as long as you’re using it correctly. Something that I have learned over the years is that so many people are making 401k mistakes and they don’t even know it.

Sometimes I get asked questions from coworkers about what they should do regarding their 401k and it:

- Makes me nervous that my coworkers, who are extremely intelligent people working for a Fortune 50 company, don’t know how to do something as simple as use their 401k in the most effective way possible, and…

- Makes me happy that I can spread education to people so that they can reach their financial goals sooner.

In essence, that is why I write these blogs. Tons of people have no idea what they’re doing when it comes to their retirement, and if people don’t know what to do then guess what, they’re not going to do anything. That is the absolute worst case my friends.

And I love that I can help educate people on this. I have a legitimate passion to help others get to their goals. If you ever have questions then please, do not hesitate to email me at [email protected]. I would be thrilled to help.

If you have been reading or listening to people write or talk about financial independence for a while then you’ve likely heard of some major 401k mistakes, like:

- Don’t ever withdrawal from your 401k before retirement!

- Always increase your annual contributions!

- Don’t take a loan from your 401k!

While I do really agree with all of those (for the most part, there are always exceptions), those are BORING.

And obvious.

I wanted to give you a look behind the scenes as to what I think are the five most underrated 401k mistakes that someone can make.

So, in reverse order, starting with number 5…………drumroll please……………I said please!

5 – Not taking the bull by the freaking horns

This is not a mistake that I can give a concrete example but more of a mindset. A lot of people that I talk to will tell me that they invest in their 401k, but they have no idea how much they invest, what they invest in, what fees they pay, or anything about their account! This is YOUR retirement. You have to know what is going on in your account. This affects literally nobody except for you.

It would be damn shame if you get to age 60 and you can’t retire for 5 more years because you’re just now looking to see how much you’re investing each year and you’re not even close to where you need to be. Or, maybe you’re total invested in bonds when you’re 25 and should be much heavier into stocks.

The fact of the matter is that this is your 401k and it’s your personal finance – it’s called personal because it’s personal! So, take some ownership of it and understand your account.

4 – Being invested in a contradictory fashion to your retirement goals

I hinted at this a bit in the past comment, but your goals need to be aligned with your portfolio, and I think this deserved its own mistake. When I first started with my company, I was investing for over a year and when I opened my account (which was being managed by the brokerage company) I noticed that my risk tolerance was “average”.

WHAT.

I was 24.

That thing needed to be asked risky as humanly possible. I had 41 years before I was going to need that money, so I wanted to be very risky, as is common for a new investor. I understand why Fidelity couldn’t make that decision without me saying that, but if I hadn’t looked then it probably still would be a medium risk tolerance.

This is probably even more important as I’m getting closer to retirement to make sure that my portfolio is becoming more conservative, so the volatility is significantly decreased. This all ties in with number 5 of taking the bull by the horns, but you HAVE to make sure that your portfolio is designed in a way to set you up for success.

If you haven’t done this yet, then make sure you are stopping reading this and going to your 401k website right now and checking it. Even if someone else manages it that doesn’t mean that they have your own goals in mind, because you might not have ever told them your goals.

3 – Not considering using a Roth

Typically, a 401k is usually setup to be a pre-tax account. So, money will go in pre-tax and then when you reach the minimum age of 59 ½, then you can take that money out, but you will have to pay taxes on it.

If you’ve been in the investing/financial community at all, then you’ve likely heard the topic about what you should invest in – Roth or traditional, but that typically refers to an IRA.

Essentially, there is no right or wrong answer.

People that prefer a Roth like it because they know that once their money is in, it won’t be taxed again. They pay the piper upfront and then whatever their account says is theirs.

People that prefer the traditional prefer it because they can put more money in faster, since it’s pre-tax, and if they intend to have a smaller income or a lower tax rate when they’re pulling it out, then it might make sense to do that.

But, that’s a risk, so just depends on what you think will happen in the future!

In short, there is no right or wrong answer. Typically, I prefer a Roth because I think it allows me to save more money now. For instance, I can only put $6,000 in my IRA in 2020 – so $6,000 pretax is exactly that – it’s $6,000 out of my paycheck but it will be taxed later on.

But if I do a Roth, then I’m putting in $6,000 post-tax which is about $8,000 or so of pre-tax money. In essence, I am using the Roth as a way to force myself to save more so that I max out that IRA.

Now when it comes to my 401k, my goal is simply to make sure that I’m taking a well-rounded approach. I’m not trying to hit it big necessarily and am more focused on making sure that my goals are staying on track. So, I literally put half of my 401k into a Roth and half into a traditional. That way I’m perfectly balanced and am making sure that I am being conservative for the future.

The mistake is not knowing that this option exists. I worked a solid 5 years of my career before knowing that I could put my 401k contributions into a Roth account. I was already investing in a Roth IRA at this point, so I clearly thought that a Roth was a good option – I just didn’t know.

This really boils down to the overarching lesson that I’ve already touched on a bit that it’s important to take the bull by the horns and knowing what your account is, what you’re investing is, and just understanding the entire process like the back of your hand.

2 – Being invested primarily in your company’s stock

This is one that I see all too common with people. Chances are, you work for a great company and you want to invest in that company – and that is a great thing! I highly encourage people to invest in the company that they work for IF that company is poised for a great future and is a role model type of company in the industry that they’re in.

If they are, then you’re golden. If not, trouble could be on the horizon.

Let me paint a picture for you – you have worked for the same company for the last 30 years, since college, and now you’re 52 and getting close to thinking about retiring. You’ve been saving steadily, and your 401k is looking prime because you’ve primarily invested in your own company and their stock has blown up over your career.

And then…Boom! Something tragic happens and the company goes bankrupt. Not only have you now lost most of your 401k now, but you’ve also lost your job. You’re now sitting there with without a job and a 401k that is cut in half, at the age of 52, as your children are likely about to go to college and you’re scrambling for answers.

Pretty scary, right?

Like I said, I highly encourage investing in your company if they’re a great company, but that’s literally the only time, and that your position in that stock needs to not be overweight compared to the rest of your portfolio.

1 – Not maxing out company match

Aren’t you surprised?! Chances are, you’re not. This likely seems obvious. Everyone always says that you always should max out your company 401k match because it’s a 100% return, right?

WRONG!

It is a 100% return for the day that you earn it, but it’s much, much more than that in all reality.

It is not uncommon for a company to offer its employees a 401k match. It’s typically a 1:1 match, or maybe a 1:2 match, and then it’s capped around maybe 4-8%. So, if it was a 1:1 match, then for every X percent that you put in, the company would also put that same amount into your 401k.

And if it was a 1:2 match, then maybe you’d put in 6% and the company would put in 3%. In that case, the instant return would be 50%, but again, the actual return is much, much higher!

Let’s take a look at the following scenario:

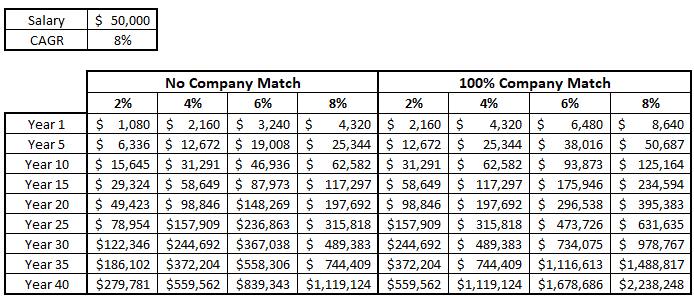

You make $50,000/year and your company will match at a 1:1 ratio up to 6% of your income. So, if you put in 6% of your income, which is $3,000/year, then your company will also put in 6%, or $3,000/year.

Unfortunately for you, you don’t think that you can afford it so you only put in 4%, or $2,000, which then means that your company will also put in that same amount. If you were to make that same $50,000 for your 40-year career, and you realized an 8% CAGR (Stock Market average is 11%), then after 40 years you would have $1,119,124! That’s pretty dang good, right? Well, it is, but not really…

If you had maxed out your 401k match (which is only an extra $83.33/month), then your total after 40 years would be $1,678,686. So, basically you “saved” $40,000 over your career by only investing 4% instead of 6% but when it was time to retire, your total was now $560,000 less than what it would’ve been if you’d maxed out your match the whole time. So, your short-term focus gave you $40,000 but cost you $560,000 – that’s not a good deal.

In fact, your total at 6% was 50% more than it if you only invested the 4% match. That is absolutely stunning!

below shows some different scenarios if you were to take advantage, or not take advantage, of your company at a 1:1 ratio using that same $50,000 salary and 8% CAGR.

So, did you not max out your company match cost you 100%? Nope! It actually cost you 1400%!!! $560,000 is what you missed out on just to save $40,000, which you likely blew on stupid stuff (I know that I would’ve).

This might seem harsh, but I’m coming at this from an angle of teaching. I have made a lot of these mistakes before, including #1, so I don’t want you to make the same mistakes that I did. Do yourself, your family, and your future self a huge favor and really take these mistakes to heart.

One amazing thing about the internet is that it’s so easy for people to share their stories. The difference between a wise man and a fool is that a fool doesn’t learn from his mistakes.

Fortunately for you, I was a fool that has now become a wise man by learning from these mistakes – If you learn from my mistakes, then I think you can argue that you are the wisest man, or woman, in the world!