Do you have a 403b? Isn’t it frustrating how in the personal finance world always talks about a 401k but not your 403b? Don’t worry – I’m here to help make sure you’re on track with a 403b calculator!

First off, what even is a 403b?

A 403b is very, very similar to the 401k but it is for people that work for the government or nonprofit organizations, such as teachers, professors, police, firemen, etc. Most of us won’t qualify for a 403b as we’re not selfless enough to do this type of work, but we do have a 401k to fall back on.

What actually is the difference between a 401k and a 403b?

Honestly, not much.

- Both have a 2020 contribution limit of $19,500 for an individual and $57,000 for a total contribution

- Both require you to keep your money in the account until you’re 59.5 and if you don’t, you’re subject to a 10% fee

- Both will likely have a matching contribution

- Both will likely have a Roth option, meaning your contributions are post-tax, and then a pre-tax option

- Both likely have fairly high advisory fees, so it’s very important to keep this in mind, but remember that fees are absolutely not a reason to invest, especially if you’re getting any sort of matching.

I recently wrote a blog post about some of the biggest mistakes that you could make when you’re investing in a 401k and since it’s so familiar with a 403b, I recommend you check it out, especially #3 and #1, which talk about understanding your investment options and then not matching out your match.

You see, any sort of match that you get is completely free money. Like, no strings attached, cold hard cash. I say no strings attached, but you do have to wait until you’re 59.5 years old, but that really isn’t much of a string…I’d say that it’s much more of a rule that is just protecting you from yourself and inevitably emptying your retirement savings and using it for non-retirement things.

But of course, you likely know what a 403b is if you’re reading this article because you likely have one – but how do you actually know if you have enough money to retire? Well? I think it’s a few different steps:

1 – Determine Your Retirement Number

This likely seems like an impossible thing to do but trust me, it really isn’t that hard! Let me introduce you to the 4% rule.

In essence, the 4% rule says that if you are to invest your money into a stocks and bonds portfolio, and you remove 4% of your starting portfolio for the first year, and then that same amount every year, then you should never run out of money.

Let me explain with an example:

- You retire with $1 million

- You will withdrawal 4% the first year, which is $40,000, and then you will withdrawal that same amount every year after that

- You should theoretically never run out of money

I know that this might seem hard to believe, but it really isn’t when you put the pen to pad. Believe it or not, the results will actually shock you. I went back and looked at many time periods since 1928 when I used a portfolio that was a 60/40 ratio of stocks and bonds, the portfolio literally never ran out of money.

Insane, right?

While this is great, how can you actually apply it to your portfolio? Well, if you’re going to take out 4% every year, then you need to make sure that you have enough saved to cover that, right?

Let’s pretend that you think you’re going to need $50,000/year to maintain your quality of life. To be able to take out $50,000 each year, you’re going to simply take $50,000/4%, or you can multiply $50,000 by 25, to get $1,250,000.

So, if you save $1,250,000, then you can safely withdrawal $50,000 every year, as the data shows, and never run out of money! Pretty dang cool to have a very, very concrete goal like that, isn’t it? But that’s only part of it!

2 – Determine if You’re on Track with a 403b Retirement Calculator

This is the really fun one if you ask me! As you all know, I am a huge numbers nerd and absolutely love digging into the data. I am guessing that you’re the same, and even if you don’t like getting in really deep, I created a very easy 403b calculator that you can use in a few easy steps to make sure you’re on track:

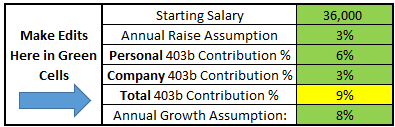

All you need to use the calculator are a few different pieces of information:

- Your Starting Salary

- Annual Raise Assumption – this is simply the amount that you think your salary will raise. Maybe it’s common to get a 3% raise, or 10%, or no raise at all. Obviously, the lower number that you input, the more conservative the amount will be.

- Personal 403b Contribution % – this is simply the amount that you plan to contribute.

- Company 403b Contribution % – this is just the match that you receive. Plan the match around the amount that you plan to contribute. For instance, if the match is 1:1 up to 5%, but you only plan to put in 3%, then you need to put in 3% for the company match. But if I can get one thing through to you in this article…please, please please – match out the company match. So, if it’s up to 5%, do 5%…at a MINIMUM! It’s literally free money!

- Annual Growth Assumption – the S&P 500 average since 1950 is 11%, so I like to use 8% as a conservative estimate. If you think the market will be even worse than that, go lower! Try 6%! Again, the lower number that you put in here, the more conservative, which is only going to help you in the long run!

Let’s run through a real-life example:

- Your Starting Salary – I am going to put in $36,000 as that is the average starting salary in Ohio, where I life

- Annual Raise Assumption – I am going to assume 3%, which is slightly over the average inflation rate of 2%.

- Personal 403b Contribution % – I’m going to say 6% here, because I am assuming that I will get a company match of 50% up to 3%, meaning I have to put in 6% to get the full match

- Company 403b Contribution % – as I just described, I am assuming a match of 50% on the 6% that I’m putting in, so a total of 3%

- Annual Growth Assumption – I am going to assume 3% here since, as I noted above, I think this is a conservative assumption

Take a look below at the inputs and how they will look in the calculator:

Believe it or not, that’s the end of what you need to do to use the calculator! You can then look at when you might retire and simple scroll down to that year and look at what your estimated total might be! For instance, below shows just how the first five years might look:

Click to zoomAs you can see, the beauty of investing is that in Year 1, you’re really only getting the 8% return on your initial investment and the company match. But the longer you invest, the more that you get to start earning that same 8% on not only your investments but the returns that you have already made!

That, my friends, is the beauty of compound interest, and it’s why Einstein said, “Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.”

What he means in this saying is that if you really understand compound interest, then you’re going to be very motivated to take advantage as much as you can and if you don’t, then you’re really going to be paying for it in the long run.

If you already have a 403b and aren’t starting from scratch, simply input all of the same numbers but change the first cell to the amount that you currently have. For instance, if you have $10,000, you would input $10,000 into cell C11, or Year 1, Month 1, as I have shown below:

Below, I have included some more results, in 5-year increments, based off the inputs that we discussed above in the original example where we are starting from scratch:

You’ll likely narrow into the yellow highlight, which you might notice is just slightly over the $1.25 million goal that we also talked about previously. So, that means if all of these assumptions were true, then you would have to work 4 months into your 40th year to be able to retire and hit your retirement goal!

Whether or not that’s actually what happens is going to be up to you and the market performance, but if you don’t have this in mind when you’re planning your retirement, then you’re starting off behind the eight ball!

Now that you know where your plan is going to put you, and when you’re able to retire, the part that you can truly impact is beginning – let’s head to step 3!

3 – Evaluate Your Plan

Let’s stick with this same example that we’ve laid out above – if you’re starting teaching after graduating college, say at age 22, this means you’re going to retire around age 62. That might be right on for you, or 3 year early if you’ve planning on age 65, or maybe it’s even, oh I don’t know, let’s say 7 years too late if you were hoping to retire at age 55.

What do you do?

Easy – regardless of which situation you find yourself in, increase your contributions! If you can, that is. If you’re ahead of schedule or on schedule, you obviously don’t need to do this, but why not do it if you can?

The issue with FIRE, or Financial Independence, Retire Early, is that it implies that you’re working so hard to retire early. I like to say just FI, or even financial autonomy, and then do whatever I want. So maybe the acronym is FADWIW (Financial Autonomy Do Whatever I Want). Hmm – I don’t like that acronym as much…

But the thing is, you don’t have to retire early. Maybe you love your job. Or, maybe you want to get to this point in life and then do a different job that is more fulfilling, or even start your own business!

This all starts with financial freedom, so the key to achieving this as early as you can is that it simply just opens more doors for you to decide later what you want.

So, let’s go back to that example where you want to retire at age 55. You basically have three options:

- Get a better annual return

- Get higher raises

- Increase contributions, either if your employer does or if you do

You have the ability to do all of these, although the first two are indirect (if you can outperform the market with your investments or if you’re a boss at your job and get promotions) but you’re also limited to a product of the environment to a point.

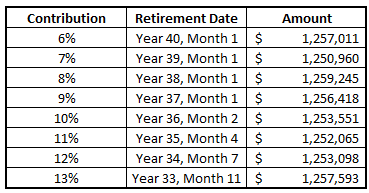

The third way is 100% on you. Even if your employer match doesn’t change, you can always put more in, up to $19,500 in 2020. So, let’s do just that. I’m going to increase the contribution by 1% and see how that changes the retirement date:

I know that it might seem daunting for you to contribute 13% of your salary to retirement, but if you can start doing this from day 1 then you’re never going to know the difference.

If you start from the beginning, the difference of 6% and 13% on a $36K salary is only about $96/paycheck assuming you’re paid biweekly. And that’s pre-tax! If you were to actually receive that money, it would probably be closer to $70.

The question is this – would you rather have that extra $70 every two weeks or have the ability to retire 7 years early? There is no generic right or wrong answer – it’s 100% what is best for you, and that is why it’s called personal finance!

I urge you to download the 403b calculator, play around with it a little bit, and see if you’re on track for your goals. If you have any questions, please don’t hesitate to reach out to me at [email protected], and if you know of someone else that might benefit from this article, share it with them, or send them the link to my 401k calculator!

We’re all in this together – good luck in your journey!