Updated 4/21/2023

Cash is king, and finding companies that generate cash is the holy grail of investing. The basic cash flow statement provides answers to the question, does this company create free cash flow?

In our ongoing series of learning basic accounting as a new language, today, we are going to dive into the basic cash flow statement.

Interesting tidbit, the cash flow statement didn’t come into existence until 1987! Wrap your brain around that, as some of the great investors we look up to didn’t have this statement to help them determine how companies used their cash.

Investors such as Buffett, Munger, Lynch, and Graham didn’t have that statement available for their analysis of many of the great companies they analyzed. Referred to as “flow of funds”, the accrual basis we love and know today wasn’t available then.

In today’s post, we will learn:

- What is a Cash Flow Statement

- Components of the Cash Flow Statement

- Cash Flows From Operations (CFO)

- Cash Flows from Investing Activities (CFI)

- Cash From Financing Activities (CFF)

- How Cash Flow is Calculated and Other Metrics Used to Analyze the Cash Flow Statement

- Final Thoughts

Ok, let’s dive in and learn more about the basic cash flow statement.

What is a Cash Flow Statement

As defined by Investopedia:

“The statement of cash flows, or the cash flow statement, is a financial statement that summarizes the amount of cash and cash equivalents entering and leaving a company.”

The cash flow statement measures the effectiveness of a company in managing its cash. That means how well a company generates cash to pay its debt and fund the operations of the business.

The cash flow statement is the third of the required financial statements for all public companies. The others are the income statement and balance sheet, and all have been mandatory since 1987.

In today’s article, we will break down some of the parts of the cash flow statement and how we can use it to our advantage as investors.

The cash flow statement is the last of the three financial statements, and it ties together both the income statement and balance sheet. As we will see, they are all tied together, and it helps explain the other statements and their impacts. It helps bridge between the income statement and balance sheet by showing how money moves in and out of the business.

The cash flow statement is probably the least read and understood of the financial statements, but I would argue aside from the balance sheet is one of the most important of statements, as it highlights the profitability of the company.

Companies that are unable to create cash flow or free cash flow must rely on other forms of financing their activities. After all, you have to have money to pay for things such as salary, inventories, dividends, and more.

There are two methods for creating a basic cash flow statement.

- Direct method

- Indirect method

It is the norm for companies to report their cash activities on an indirect method. The direct method or cash method records activities as they occur, whereas the indirect method reconciles accounting entries on a cash-in and cash-out basis.

Let’s move on to the structure of the basic cash flow statement.

Components of the Cash Flow Statement

The basic structure of a cash flow statement contains three sections:

- Operating Activities

- Investing Activities

- Financing Activities

We will break those sections down a little more in the upcoming sections.

It is important to understand that the cash flow statement is different from the income statement and balance sheet because the cash flow statement doesn’t deal with future incoming and outgoing cash on a credit basis, as do both the income statement and balance sheet.

That difference means that cash is not the same as net income, which on the income statement and balance sheet are inclusive of cash sales and sales from credit.

The purpose of the cash flow statement is to give us a detailed picture of what happened to the company’s cash from a specific period, usually on a quarterly or annual basis.

The cash flow statement tells us how profitable a company is and how well they operate the business both in the short-term and long-term, as evidenced by the amount of cash flowing in and out of the business.

Ok, let’s move on to the three separate sections of the basic cash flow statement. Remember, as we move from each section, we can read them from top to bottom; in other words, the cash flows from section to section until we reach the bottom of the statement.

Cash Flows From Operations (CFO)

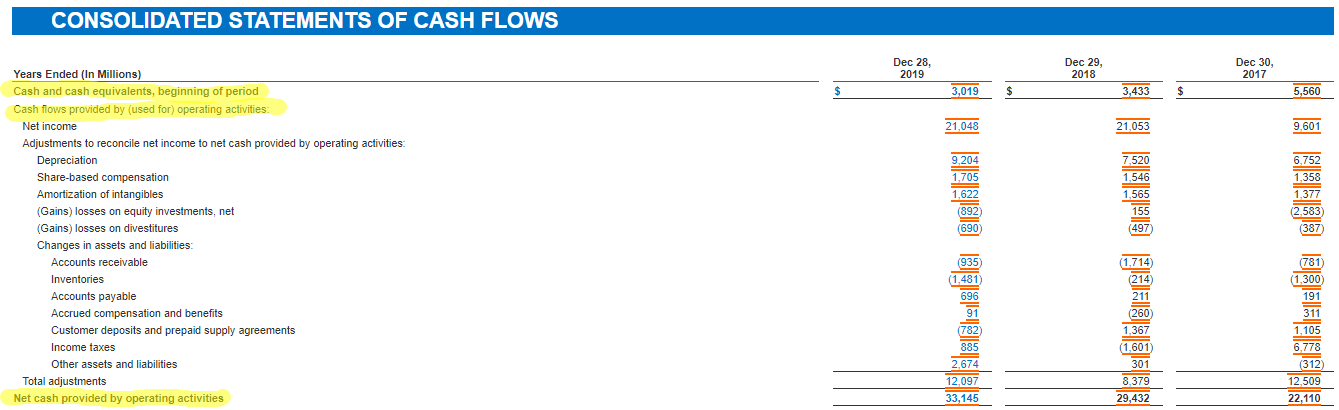

For reference today, we will use Intel’s (INTC) statement of cash flows from its 2019 annual report.

The cash flow from operations is probably the most important component of the cash flow statement. It helps tie together the income statement and the use of cash for the operations of Intel, for example.

If you look at the last line of the income statement, you will see the net income, and as you look at the first line of the cash flow statement, you will notice the same number from the income statement.

As we work through the cash flow statement, you might have questions about the different line items that I mention, if you would like deeper definitions of each item, please check this post out from Cameron Smith below:

Interpreting the Statement of Cash Flows

The basic structure of the cash from operations is the following:

Net Income

Depreciation

Amortization

Impairment Expense

Stock Based Compensation

Change in Working Capital

Accounts receivable

Accounts payable

Inventory

Change in Provisions

Interest Tax

Tax

Operating Cash Flow

As you work down through the cash flow from operations, you can see how Intel spends money from the net income that the company created from the income statement.

It is not unusual to see negative numbers as we walk down through the section, those negative numbers we see in Intel’s statement tell us about cash outflows, and the positive numbers indicate a cash inflow.

You start with the net income and then add or subtract each item as you work down through the statement.

The easiest way to think about the cash flow from operations is like your personal checking account. As money comes in, you pay it out for the bills you owe.

If you arrive at the bottom line and that figure is negative, that indicates Intel is not creating enough income to fund the basic operations of the business. This means as you move down to other sections, you will see additional funds added in the form of additional debt or selling equity or shares to raise cash.

A few important notes to several line items, such as depreciation.

Deductions such as depreciation are considered an expense and deducted from profit in the income statement, but it does not impact the cash flow of the company as depreciation is a non-cash expense. And as such, we add depreciation back to the cash flow statement, as you can observe in Intel’s statement.

Other items you will see in the cash flow from operations section include:

- Rent payments

- Salary and wage payments to employees

In the cash of investment companies such as brokerages, you will find items like receipts from the sale of loans, debt, or equity. From banks, you might see items like provisions for credit losses, changes in the fair value of marketable securities, and net changes in debt and equity securities.

As always, companies such as banks, insurance agencies, and brokerages speak a different accounting language, and to understand them, you must understand their language. For today’s purposes, we will stay away from those types of businesses to avoid additional confusion.

An important note for calculating free cash flow or cash flow from equity, you will use line items from the cash flow from operations to calculate both calculations.

Many companies outline how they calculate free cash flow and will highlight those figures in the notes section of their financials.

For now, numbers to keep an eye on for those calculations:

- Depreciation / Amortization

- Change in working capital

- Net Cash from operations

Ok, let’s move on to the next section of the basic cash flow statement.

Cash Flows from Investing Activities (CFI)

The next section on the cash flow statement is the cash flows from investing activities. The investing activities section includes any sources and uses of investing cash from the company.

Items such as:

- Purchase or sale of an asset

- Loans to vendors

- Payments for mergers or acquisition

- Additions to property, plant, and equipment

The old PP&E is an old friend and is a part of any free cash flow calculations. Also known as expenditures on cap-ex, or investments in computers, chairs, printer paper, anything that relates to operations of the business that creates revenue.

PP&E is the actual cash spent on those items known as cap ex, which can consist of maintenance cap-ex or monies spent on repairs of equipment. Or monies spent to continue operations.

The financing section connects with the long-term assets on the balance sheet that are investments, and thus they flow through a different section of the cash flow statement.

Usually, cash flows from investing are cash outflows or “cash out.” That is because of the use of cash to purchase new equipment, buildings, or marketable securities. But, when a company divests or sells an asset, the transaction is a cash inflow.

Cash flows from investments will usually be a negative number because, at this stage of the cash flow statement, the company is using cash to sustain the business, either with capex purchases or buying or selling investments to create more income.

Again, if the cash from operations is a negative number, then all of these transactions will need funding from additional sources, other than from operations of the company. Which helps illustrate the positivity of a company that can generate cash flow from operations.

Cash From Financing Activities (CFF)

Cash from financing activities is a fun section; here, we will discover how much money the company pays out in dividends, share repurchases, debt payments, or taking on more debt.

Changes in cash in the financing section are cash inflows when raising capital from activities such as selling shares of the company or taking on more debt. And likewise, they are cash outflows when a company is paying out, such as items as dividends or share repurchases.

For example, if Intel issues a bond offering to the public, the company would receive cash inflows with the sale of each bond. On the other side, the interest payments the bond creates are a cash outflow with the interest payments due to the customers purchasing the bonds.

In this section, it is not uncommon to see cash as a positive number, as in the case of Intel, who took on additional bond financing during the fiscal year of 2019.

As we come to the end of the three components of the cash flow statement, you will see at the bottom line, the term cash, and cash equivalents.

To arrive at this number, you simply add all three components together and arrive at this number. And in Intel’s case, we arrive at cash and cash equivalents of $8,736 million, and if you take a quick peek at the balance sheet, you will see the very same number at the top of the balance sheet. All of which perfectly illustrates how the cash flow statement ties together both the income statement and balance sheet.

The basic flow, if you will, is the net income comes into the cash flow statement, the company pays for all the bills it requires to generate that net income, while also creating more cash in the form of liquidation of assets and paying down liabilities. Finally, we arrive at the end, which equals the cash and cash equivalents.

How Cash Flow is Calculated and Other Metrics to Analyze the Cash Flow Statement

As we arrive at the end of the cash flow statement, the next activity needs to be analyzing the statement, and the easiest way to do this is through metrics such as:

A widely discussed metric is free cash flow, which is simple to calculate. You take the cash flow from operations and add back the depreciation/amortization line items and then subtract the CapEx or PP&E from the cash from the investing section.

A quick example from Intel.

Free Cash Flow = Cash From Operations + Depreciation/Amortization – PP&E

From Intel’s cash flow statement:

- Net Cash from Operations – $17,315 million

- Depreciation – $5,248 million

- Additions to property, plant, and equipment – ($6,676)

Plugging in the numbers to our formula

Free Cash Flow = 17,315 + 5,248 – 6,676

Free Cash Flow = $15,887

If you want to learn more about the above formula, and other methods to analyze both the free cash flow of the business and the ratios to help you analyze your company, please follow the links above.

Final Thoughts

As discussed in our ongoing series on learning the different financial statements, the language of business is accounting. And to understand how to analyze companies both from a financial aspect but also from an operational basis, we must understand accounting.

Like learning any language, it takes practice and repetition of the activities. As I attempt to learn Portuguese, I am learning that in spades.

But I have found the best way to learn anything is to put the learning into practice. And I think learning accounting falls into that category as well. Only by reading through the financial statements will you learn not only accounting but also how that company works.

Understanding the basic cash flow statement will help you learn how profitable a company like Intel, Amazon, or Apple are, but also it will give you insight into how the company generates that profitability.

That is going to wrap up our discussion on the basic cash flow statement today. Here are links to the other two financial statements if you are interested:

- Simple Income Statement Structure Breakdown (by Each Component)

- Simple Balance Sheet Structure Breakdown (by Each Component)

I also highly recommend learning about putting all of this valuable information together, by mastering your ability to analyze the entire annual report (10-k).

As always, thank you for taking the time to read this post, and I hope you find something of value on your investing journey.

If I can be of any further assistance, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave