If you’ve been following along with my posts lately, you know that I am getting in deep with understanding Momentum Investing because it really sparked my interest from a few podcasts that I listened to. In the last few chapters of Dual Momentum Investing, Gary Antonacci, author of the book, tells us that Momentum Investing works because you’re essentially capitalizing on the behavioral finance biases of others.

I’ve always been one that’s a big-time value investor, but I’d be lying if I said that the concept of Momentum Investing didn’t really stick out to me. I’m only 4 chapters into Dual Momentum Investing, but it really seems like the reason that it works is because you’re essentially playing the people that are investing in the stock market rather than actual picking stocks.

While I admit, this is the definition of being speculative and goes against my normal investing philosophy, but ALL I AM SAYING is that it catches my eye. Like I said, I’m only four chapters in, but while in my first review of the book I was super skeptical, I do find myself drinking a little bit more of the Kool-Aid now that I am a couple chapters in.

So, why does Antonacci say that it works? Well, essentially, you’re preying on the weak! I laughed as I was reading this chapter because a lot of the biases fell into my 7 deadly sins, a lot of which I have fallen into before, so in a way it almost felt like things were coming full circle.

According to Graham and Dodd:

“The prices of common stocks are not carefully thought out computations, but the resultants of a welter of human reactions.” And in my eyes, if you can try to predict the way that humans are going to react to certain news and changes, then you can play them, in a sense, for your own benefit.

So, let’s not waste any more time and get into some of the major behavioral finance tendencies that make momentum investing work!

Behavioral Finance Tendency: Loss Aversion

This simply is that investors feel worse about a loss in their money than they do in a gain. So, a 10% loss would hurt much more than the enjoyment that you might get from a 10% gain. To me, this really isn’t surprising at all.

Nobody ever does anything because they expect to lose money. The S&P 500 has historically increased at a clip of 11%/year since 1950, so of course losses will hurt more – they were unexpected!

But what if it’s with gambling? You know the odds are against you but you still expect (or hope) to win, so even if you do win, you won’t be as happy as the sadness if you had lost, and you knew you had awful odds going into this.

Personally, I am at the point that I love bear markets because I am focused on the Long-term (for the most part) so cheap prices today mean way better values tomorrow. In other words, I’ll take a worse performing portfolio to get me some bargain deals. A lot of people don’t view it this way and instead won’t take advantage, so try to stay neutral and not let loss aversion ruin any future opportunities for you!

Anchoring and Underreaction

Anchoring is when you hold onto the first thing that you learn and essentially use it as a means to justify everything else with the company. An example would be if I was to look at a company like SHOP that has just consistently gone up through the coronavirus pandemic. At one point, I was pretty speculative and bought in on SHOP as a “Momentum Investment” per se.

In other words, I saw that the company was much cheaper than how it had been in recent months, and I loved the business model, especially during the pandemic, so I dabbled a bit as pure speculation. The value-investor part of me would’ve killed me for making this investment trade.

Taking a look at the company’s YTD chart below, the 2020 low was right around $320 and had been as high as the low-500’s:

I felt like somewhat of a big shot since I bought in at what I thought was a great price, purely on a MOMENTUM Investment, of just under $377:

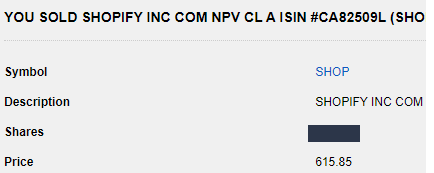

I then later sold that stock at a much higher price of nearly $616, locking in a gain of 63% in less than a month on this investment:

That’s a pretty solid gain, right? Well, the issue is that I used ‘Momentum Logic’ to purchase the stock and then when the share price started to rise, I started to use ‘Value Logic’ and legit told myself things like, “why would you buy a stock with a 40 P/S ratio?”

Now, that question was valid even when I bought it, but the thing is, Momentum Investing is very different than value, and both can be right. But you need to have clearly defined goals and strategies. Mine got intertwingles and cost me a lot, as I sold at $615 and SHOP is now selling at well over $1000.

But let’s get off of my personal stories, and me simply sounding like a greedy investor because 63% in a month is amazing lol, and let’s go back to the book!

Antonacci says that “Anchoring of whatever kind leads to inertia. This can cause investors to underreact to news, which keeps prices below their fair value.” In other words, if a company seems overvalued but has some really good news come out about it, people might not continue to pile in on the stock because it seems like they’re bound for a correction.

This is how you can lose out on Momentum Investing gains because once the traction finally all clicks with investors, the inertia is going to be hard to stop!

Behavioral Finance Classic: Confirmation Bias

This is one of my favorite ones! I have found myself a victim of confirmation bias probably 100+ times, not only in investing, but also in other areas of my life.

Confirmation bias is “the tendency to overemphasize the importance of information that confirms our views.”

For instance, maybe the company has an insane ROIC like Visa or Mastercard. You might then take that information and sweep other things under the rug such as the some of the short-term financials of the company or maybe even the fact that they have a pretty high P/S ratio, especially for a value-investor!

If you think that ROIC is the end all be all, then you very well could be willing to overlook things that you normally wouldn’t.

I have done this with SHOP as I mentioned before by thinking about the big picture, qualitative aspect about them in a pandemic environment and totally ignored P/S, which honestly is probably a top 3 most important metric for stocks that I evaluate.

You might have an initial reaction on a company that they’re absolutely killing it and then you go out there and try to find information that supports this claim.

I won’t lie – I’m an open book. I recently did this with ROKU. I have loved ROKU, again as a Momentum/Speculative company, for a couple years now. I have had a position with them for the last couple years, before I really became super focused on the analytical side of investing, and I was considering adding to my position.

I simply looked at everything that I could to try to decide if there was literally anything at all that I could find to justify adding to my position, and I think that’s the perfect summary. I was looking to JUSTIFY an investment rather than coming at it with a completely open mind.

My mind was cloudy before I even looked at a 10k. At the end of the day, I do think that the company is poised for great success, but I determined at that time that I already had enough of a speculative investment in them and I needed to keep with my value approach.

Now, of course that can change in the future, but regardless of how that decision turns out, I am happy that I wasn’t a victim to confirmation bias.

Herding, Feedback Trading and Overreaction

Herding is essentially those that are bandwagon traders (cough cough Tesla, Virgin Galactic, “stay-at-home stocks”, etc.) that just don’t want to miss the boat.

Feedback trading is those that simply will trade based off the news that comes out. Good news means buy and bad news means sell.

Overreaction is generally caused by the previous two because so many people have either piled into a stock or sold out of it, causing it to be way overvalued or undervalued, even for momentum investing.

I guarantee that you have all been a victim of this – I know that I absolutely have. The FOMO (fear of missing out) of a stock is the literally WOAT (worst of all time…think Yasiel Puig before he played for the Indians ?).

I have sometimes just sat there and looked at stocks go higher and higher and felt absolutely sick that I didn’t get into them when they were cheaper, so I inevitably will end up overpaying for the position. Personally, I am ok with overpaying if you think the long-term of the company is good and you’re in it for the long-term.

As Buffett has said, “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” This resonates with me and it means that if you find that amazing performer, it’s ok to put a bit of a premium on them. Say, maybe Apple is one of those companies. For me, it’s Visa, which I have talked about many times before.

The note that I had written down on this chapter in my book is that it “doesn’t matter if you’re right – be in the herd”. I’m not saying that I agree with this, but basically it was me trying to say that if you’re in the herd before everyone else jumps in, you can benefit from some monster price increases.

Antonacci also touches on hindsight bias and self-attribution in this chapter. Hindsight bias is when you look at something after the fact and it just seems so obvious while self-attribution is when you get all the credit if things work out and none of the blame, because you claim it wasn’t your fault, if the investment didn’t work.

Say you bought Clorox in February – an example of self-attribution would be that you knew the COVID-19 Pandemic was coming. Maybe you looked at China and had a gut feel and maybe you got lucky, but you need to be honest with yourself and not let your biases get in the way.

Disposition Effect

The disposition effect is “the tendency of investors to sell their winners too early in order to lock in gains, while holding on to losers too long in the hope of making back what they have lost.”

In general, this somewhat seems like value-investing, if a company has a strong run and becomes under-valued. Just as if a company was worthy of a buy and then the share price drops – as long as nothing has permanently impacted the business, then are they just even more of a value than when you bought the company?

But it’s the exact opposite with Momentum Investing, and the data shows that! Antonacci has cited some great studies that show that buying the top performers actually has generated better returns than focusing on the laggards, and while a bad performing stock doesn’t necessarily mean value, I do think that it’s a very interesting study!

Antonacci ends the chapter essentially saying that Momentum Investing works because of all the flaws that people have in their own investing. You can capitalize on their own behavioral finance tendencies to take advantage of stocks when people are underreacting or overreacting to them and then properly place your money into those companies.

In other words, the actual company performance doesn’t even matter – it’s all about playing the people! In a way, I kinda love this…and in a way, I’m also kinda terrified for how this is going… stay tuned!