Updated 9/3/2023

“Capital allocation is a senior management team’s most fundamental responsibility. The problem is that many CEOs don’t know how to allocate capital effectively. The objective of capital allocation is to build long-term value per share.”

Michael Mauboussin

As we will see, job number one for CEOs remains capital allocation because those decisions drive returns for the company and shareholders. Many CEOs remain skilled leaders, operators, salespeople, and administrators, but few operate as skilled capital allocators.

One of Warren Buffett’s strengths remains his capital allocation skills; he has built Berkshire Hathaway from a small textile company to one of the largest corporations in the world by market cap.

Many CEOs and investors would be wise to study his ideas and thoughts on allocating capital because whether it is investing in a new product, ala the iPhone, or buying a business such as GEICO, there are many ways to go with allocation, and each can generate greater returns for investors.

In today’s post, we will learn:

Okay, let’s dive in and learn more about capital allocation.

What is Capital Allocation?

Capital allocation, according to Investopedia:

“Capital allocation is about where and how a corporation’s chief executive officer (CEO) decides to spend the money that the company has earned. Capital allocation means distributing and investing a company’s financial resources in ways that will increase its efficiency, and maximize its profits.”

Every company generates excess capital above their operational needs, at least hopefully. And what the company decides to do with that capital determines where it will go and how it will grow.

All companies want to grow and increase their presence, and allocating their capital wisely will help them achieve that goal for both the company and their shareholders.

Allocating capital is hard, and there is a lot of pressure to perform, especially with the increased scrutiny of the media today. To allocate well, the company’s management must see clearly through their “crystal ball.” And determine what the best use of its hard-earned capital is.

A few facts for you: internal financing, or the money the company generates, has funded more than 90% of capital uses, and the top three uses of capital are:

- Mergers and acquisitions

- Capital expenditures

- Research and Development

More on those in a moment, but since the 1980s, those have been the big three of capital allocation.

The proper use of capital is to grow long-term value despite the noise from Wall Street. The real goal is to build value over time and let the market reflect that value instead of juicing that short-term share price, which leads to deteriorating value over time.

A simple test to remember is the $1 invested in the business worth more than $1 invested in the market. The only way that occurs is if the long-term value of the cash flow is worth more than the original cost.

If a company can create more wealth from the investment over time, it will build value. Some great examples of this are:

- Costco

- Amazon

- Walmart

- GEICO

To name just a few, using the idea of finding great capital allocators can lead to finding great management teams. These management teams are like great coaches or chefs; success follows them wherever they go. Looking at the shortlist above, all those companies had outstanding capital allocators running the ship.

Consider this idea from Buffett’s 1987 Letter to Shareholders:

“This point can be important because the heads of many companies are not skilled in capital allocation. Their inadequacy is not surprising. Most bosses rise to the top because they have excelled in an area such as marketing, production, engineering, administration or, sometimes, institutional politics.

Once they become CEOs, they face new responsibilities. They

now must make capital allocation decisions, a critical job that

they may have never tackled and that is not easily mastered. To

stretch the point, it’s as if the final step for a highly-talented musician was not to perform at Carnegie Hall but, instead, to be named Chairman of the Federal Reserve.

The lack of skill that many CEOs have at capital allocation is no small matter: After ten years on the job, a CEO whose company annually retains earnings equal to 10% of net worth will have been responsible for the deployment of more than 60% of all the capital at work in the business.

CEOs who recognize their lack of capital-allocation skills (which not all do) will often try to compensate by turning to their staffs, management consultants, or investment bankers. Charlie and I have frequently observed the consequences of such “help.” On balance, we feel it is more likely to accentuate the capital-allocation problem than to solve it.

In the end, plenty of unintelligent capital allocation takes place in corporate America. (That’s why you hear so much about “restructuring.”).”

If job number one is to deploy capital, it makes sense to discuss where that capital comes from and how the management used it in the past.

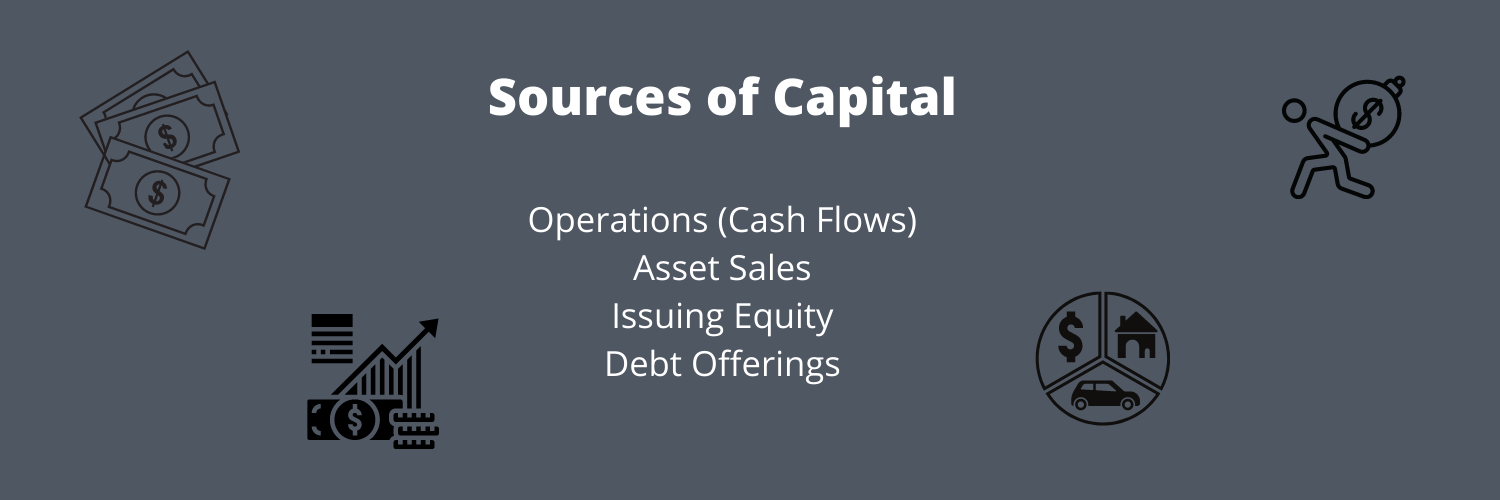

Different Sources of Capital

Companies have four main sources of capital:

- Operations (cash flows)

- Asset sales

- Issuing equity

- Debt offerings

Companies that grow quickly need large amounts of capital. For example, imagine a successful shoe store; to meet the growing demand, they need to expand to new store locations plus grow their online presence. All of those expansions, both physical and the internet, require large amounts of capital to expand. A company that grows faster than those costs of expansion generates higher returns.

Companies that can use internal cash flows to expand tend to grow faster than those that have to go outside. A great example is Amazon, which used its internal cash flows to grow exponentially without turning to outside funding sources.

Suppose a company cannot generate enough cash flow to power its growth. In that case, they must turn to external forms of capital, such as selling equity or shares or borrowing against their equity (debt financing or bonds).

The usual pecking order, if you will, is that companies prefer to use internal capital cash flows first. Then, if they need additional capital, they will turn to debt financing and equity financing.

Always remember that CEOs have an opportunity cost tied to each decision. Internal capital remains the cheapest financing available, followed by debt and equity. With interest rates historically low, debt financing remains extremely cheap, whereas equity financing equals expensive as the market values continue to skyrocket.

The greater the difference in returns on invested capital (ROIC) and the cost of that capital, the greater the long-term value the company creates.

Capital uses dictate where the money goes, and how do we follow? The next section will discuss how a company can use its capital to grow.

Seven Types of Capital Allocation

From 1980 to 2015, the greatest use of capital, far and away, equaled M&A (mergers and acquisitions). In the chart below, Michael Mauboussin shows how this data has trended over those 35 years.

Okay, let’s discuss each of these capital uses a bit.

Mergers and Acquisitions (M&A)

As stated above, mergers and acquisitions are far and away the largest sources of capital allocation. M&A is also one of the quickest, easiest, and most expensive ways to expand strategic goals.

M&A strategies tend to follow the market trend; as markets trend up, M&A starts to pick up, continuing until there is a market peak.

Generally, the early adopters of this trend tend to be the most successful, and those at the end of the curve tend to spend the most and receive the least.

When a company buys another, there are three ways to go about it: with all-cash deals, use of stock, or a combination of both. The market tends to react favorably to all-cash deals and less to any combination of stock deals.

M&A strategies tend to come about for various reasons, such as adding new technologies or offerings to their solutions, cornering the market, removing competition, or boosting lagging sales.

The two synergies, or combining powers most commonly used, are cost and sales, with costs easily becoming the most successful. Sales synergies take time and often don’t materialize, making that M&A activity risky. About 70% of all revenue synergies fail to come to fruition.

Because M&A activity is the largest dollar amount in capital allocation, it is important to understand how it works and the likelihood of success. It is also important to analyze the past success of “serial” acquirers such as Cisco to assess its allocation efforts. Not all acquirers will be successful, and we need to weigh the pros and cons of success.

We could write a series of M&A strategies and assessments in and of itself rather than focusing on how the company does and how they have done in the past.

Capital Expenditures

Capital expenditures are the second-largest amount of capital allocation.

Capital expenditures refer to buying office furniture, new computers, upgrading software, building upkeep, or maintenance. These expenditures offer the unsexy aspects of capital allocation but remain necessary to keep the lights on.

A new trend continues distinguishing between “maintenance” capital expenditures, considered the minimum necessary to keep the company going—in contrast, “growth” capital expenditures equal monies spent on expanding or growing the business.

When analyzing the capital expenditures, it is best to compare them to their sales and distinguish between maintenance and growth. You can consider depreciation a rough proxy for the maintenance cap-ex.

As companies move towards a capital-light business model, the traditional idea of capital expenditures changes. The once tried and true idea of spending on the upkeep of warehouses or factories is being replaced by upgrading software systems or investing in new computers.

A great practice remains to look at each industry or segment you want to analyze, determine what seems relatively average for the industry, and determine whether your company spends enough or needs more capital expenditures to compete.

Research and Development

Unlike other types of capital allocation, such as M&A and capital expenditures, research and development (R&D) shows up on the income statement rather than the balance sheet.

Because of old-fashioned accounting rules dating back to 1973, R&D costs are expensed rather than capitalized, which would make much more sense considering the current use of R&D in today’s business world.

R&D represents a group of activities designed to develop new products and services; the likely benefit of those costs realized years later. Consider that Intel spends billions yearly to develop new products that take years to market.

Since 1980, R&D has grown from 1.3% of sales to over 3% in 2021. And as businesses continue to invest in creating new and better products and services, these rates will likely continue.

I would argue that companies such as Facebook, Amazon, Apple, Microsoft, and many others are using a large portion of their cash flows to create new and better services and products, and these are certainly capital allocations. For example, in the TTM (trailing twelve months), Facebook has spent $21.2 billion in R&D, compared to $17.1 billion in capital expenditures, and the numbers have been trending that way for several years. And when you listen to CEO Mark Zuckerburg talk about the future of Facebook, he considers R&D spending crucial to the company’s long-term value.

Net Working Capital

The net working capital consists of inventory, accounts receivable, and accounts payable, and they are required to operate the business daily. Most definitions exclude any cash or interest-bearing assets in consideration of working capital.

A good rule of thumb is to look at the change in net working capital instead of the overall amount. The efficiency with which the company turns its capital will go a long way toward its profitability.

For example, companies such as Amazon and Walmart, which turn their inventories, quickly capitalize on this by freeing up cash flow for use elsewhere. By leveraging their just-in-time inventory systems and technology, they can buy when they need to sell and leverage their relationships with vendors to extend payment cycles, freeing up more cash.

Net working capital is a far smaller proportion of capital allocation than the first three uses.

Divestitures

Divestitures refer to the idea of selling off your company’s assets or adjusting your company’s portfolio—actions such as selling off divisions and spin-offs being the most common.

Companies will divest when they think the asset offers greater value to another company or focus more on their core operations, which they believe will improve results over time.

While this aspect of capital allocation receives far less scrutiny than M&A, over the last decade, it has averaged over 3.8% of sales, comparable to buybacks, and exceeding dividends and R&D spending.

Spin-offs are the most common use of divestitures, with the parent company distributing shares of a wholly-owned subsidiary to shareholders. For example, VF Corporation spun out its subsidiary to be named Kontoor Brands. The shareholders received ownership in both companies, receiving one share of the new company for every seven parent shares.

Dividends

A dividend is a cash payout to shareholders from profits. Both dividends and share buybacks are the main ways companies distribute cash to shareholders.

Once they establish a dividend, most companies feel honor-bound to continue and grow that dividend.

Often considered on the same level as capital expenditures, dividends remain one of CEOs’ major capital allocation decisions. Compared to the idea, share buybacks equal more on an as-cash-is-available basis.

To learn more about dividends and how to measure them, check out this post:

The Big Guide to Little Dividends

Share Buybacks

The share buyback or repurchase is the second main way companies return cash to shareholders.

Gross buybacks have grown substantially over the last 30 to 40 years, from less than $50,000 million in 1985 to $550,000 million in 2015.

The attitude behind share buybacks differs from dividends; many companies feel they will only pay buybacks after exhausting all other forms of capital allocation, including dividends.

CEOs also tend to use share buybacks as a means of “lazy” capital allocation, meaning we have nowhere else to put the money, as we might as well repurchase our shares.

Share buybacks tend to follow market trends; companies buy back shares and vice-versa as the market improves. It also matches the idea that buybacks use excess cash and that management tends to buy high and not buy low.

A Golden Rule for buybacks: We should assess when companies repurchase their shares and determine if they buy above or below their value. A company should only repurchase its shares when the stock trades below its value and no better investment opportunities are available.

Investor Takeaway

As we have seen, capital allocation is a huge part of the CEO’s job and arguably the most important role to play. Where to spend its money goes a long way toward value creation for both the company and shareholders.

Poor capital allocators might survive for a short time in the market, but the best will rise to the top over long periods. Part of assessing a company is judging the capital allocation skills of its management.

To learn more about capital allocation, please check out the seminal paper by Michael Mauboussin, which was instrumental in creating this post:

Capital Allocation: Evidence, Analytical Methods and Assessment Guidance

My hope for this post was to provide a framework for individual investors to understand what capital allocation is and what decisions CEOs and management must make to continue to grow their companies.

In the future, we will discuss more aspects of this critical decision-making skill to help us assess management teams.

With that, we will wrap up today’s discussion.

As always, thank you for taking the time to read today’s post, and I hope you find some value in your investing journey. If I can further assist, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave

Dave Ahern

Dave, a self-taught investor, empowers investors to start investing by demystifying the stock market.