When looking for a new job, it isn’t just about salary anymore. Companies with the best 401K match can be equally attractive as a strong salary.

When you begin your career, it’s very easy to look at the salary offered by a company and start making decisions based on that. But if you ever start looking for a career change, you typically start realizing that the salary is important, but there are other huge factors to look at when making a decision.

If you are looking to start your career or thinking about changing directions, remember to think about the full picture. It’s not just salary that companies are using to lure in talent. It’s benefits as well, which include insurance, retirement, and taxes.

I get it, as a young employee it’s hard to look past anything but salary, but I can assure you that some of these companies with the best 401K match should be strong contenders when making a decision. Remember, if your investments do well, you could easily retire three or four years earlier than anticipated which is a huge benefit.

It’s totally up to the employer on what type of 401K plan they want to offer to employees, but there are typically two different options they can choose from.

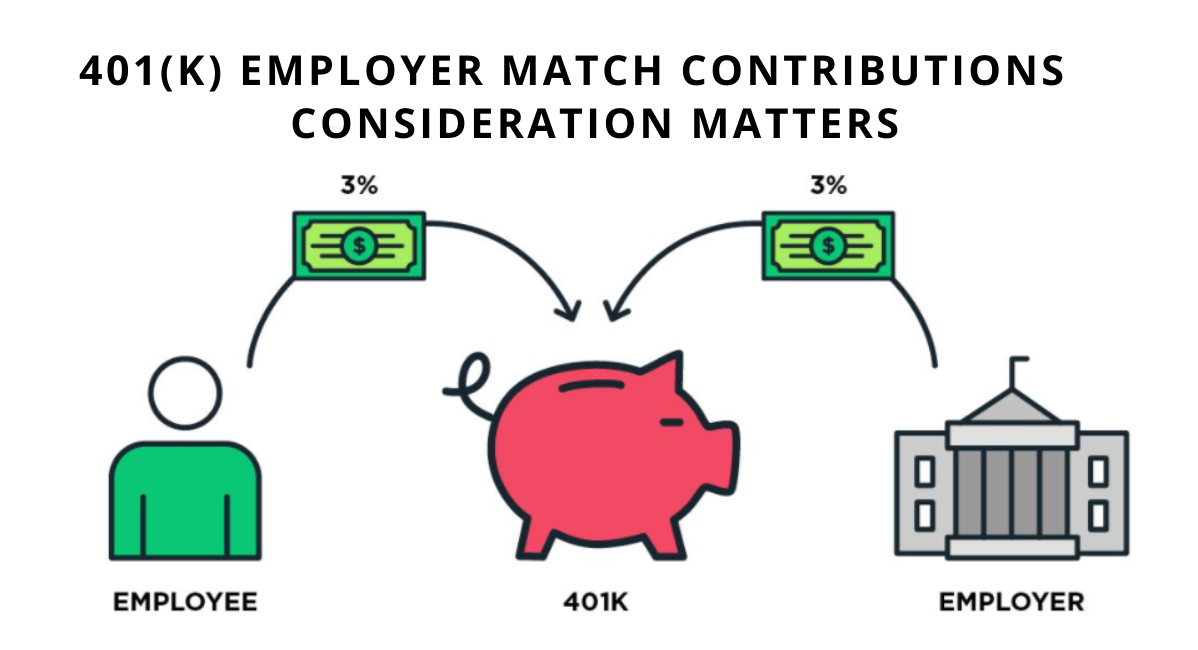

The first option is a partial match. That is exactly what it sounds like and is typically structured at a 50 percent match compared to employee contribution.

For example – let’s say you make $100,000 a year and the company offers a 50 percent dollar-for-dollar match up to six percent of your annual salary. If you maximize the full benefit and contribute six percent or $6,000 per year, the company will give you $3,000 in return.

Please keep in mind that this isn’t a one-time deposit. They will give this portion of the money back on each paycheck throughout the year. This money from the company will typically go to whatever company handles their retirement account and will be invested.

The second option is a dollar-for-dollar match 401K program. At this point in time, anyone offering a program like this would have to be considered one of the companies with the best 401K match around. It’s not an uncommon find but is certainly a huge benefit for employees.

For example – Let’s say you still make $100,000 per year, but your company offers a dollar-for-dollar match 401K program for up to five percent. That means if you maximize the program and give $5,000 per year, the company will match the full five thousand.

It’s easy to see the difference. The company gives a smaller percentage, but in the two scenarios above it costs you $1,000 less per year with the dollar-for-dollar match, and you still come out each year with $1,000 extra dollars.

Now I just want to put both examples above into perspective for everyone. Not only are you saving $1,000 per year of your own money with the dollar for dollar example, compound interest is also going to be your friend.

In example one with an assumed seven percent return, your initial investment of $9,000 would be just under $125,000 after year ten. This is assuming exactly a seven percent return and no raises. Keep in mind, a good company should also give a raise each year, but I wanted to keep this as simple as possible.

In example two, not only are you pocketing $10,000 more, over a ten-year period, the additional money from the company will be valued at more than $138,000 over a 10-year period. So, a $13,000 increase in value, and a $10,000 increase in take-home pay.

The bottom line is companies with the best 401K match can trump a salary very quickly. It may be a hidden value that doesn’t hit your pocket immediately, but you must always consider the long-term benefits when evaluating an opportunity.

Not only are companies with the best 401K match great to seek out, but another hidden benefit (that is few and far between nowadays) is a pension plan. This is just an added way of getting retirement income and can be based in a couple of different ways.

The most standard way is a monthly payment based on a percentage of your salary. There are a thousand different calculations for this, but a very generous program may be 85 percent of your seven years of highest salary, whereas others may be 50 percent of your average salary over your entire career.

To be honest, if you find a company that still had a pension program, you should consider it a huge factor when making a decision on employment. I would also recommend asking the human resources department what the “grandfather” clause looks like in case the plan ever goes away.

I’m fortunate enough to work for a company with a pension plan, and it changes often. Typically, the percentage of income goes down, but I’m grandfathered in to keep the exact same program that was in place the day I was hired if I never leave the company.

If there is ever one thing that you should take away from something that I’ve written, please let it be to always take the free money. A company pension or 401K program is the closest to free money you’ll ever receive. Not only is the company willing to match a certain amount to fund your retirement, but they are also investing it for you and letting the money do the work for itself.

To not maximize a company offered match program for any type of retirement fund is silly. I know that $50-100 per check (after it’s taxed) may seem like a lot, but trust me, your future is worth it. One day when you are 60-years old you’ll be thankful that you went without a few items early in your career to make sure you were set up for a successful retirement plan.

When I was in college, I had a really awesome job setup. I could go in whenever I wanted during the week between the hours of 6 AM and 6 PM, and as long as I worked at least two hours straight and no more than 30 hours total for the week, the company was fine. This gave me a ton of flexibility with my class schedule and also put some spending money in my pocket.

This particular company offered a company matching 401K program of five percent. For a factory-type atmosphere, this was a great perk for the full-time guys who were lifers, and for me, who was just college help.

I remember my buddy who worked at the same place telling me that he wasn’t going to participate and that he was just going to take five percent more pay each week. I told him that he was silly, and he should take the free money.

Anyway, for four years I worked an average of 15-20 hours per week (working closer to 30 in the summer and 10 during school), and when I left that job I had over $4,000 in a retirement account that I was able to take with me.

$4,000 may not seem like a ton of money, but to me, it was huge. Not only was it the first money that I earned for my retirement account, but it also forced me to roll it into another account, which got me working with a financial advisor that I still use to this day.

The money has been in its own account for another eight years and has grown to nearly $10,000. This isn’t money that I’ll ever be desperate for, but just some added fluff for when I retire because I chose a company with a great 401K match program.

A recent article published in U.S. News covers a few companies with the best 401K match, and a few other incentives they are using to incentivize employees to come to them, and retain them.

Citigroup:

U.S. News shares that Citigroup still offers a dollar-for-dollar 401K match program of up to six percent. That is a fantastic benefit and is about as strong an offer as I have heard recently. When I first started working eight years ago, my company was initially offering seven percent, but that quickly went away.

Where Citigroup really separates itself is they give two percent of eligible pay, regardless of if you are in the program or not. Now, I’ve already said take the free money no matter what, but this company won’t even let you opt-out and force you to take at least two percent, which is a huge benefit.

Farmers Insurance:

Like Citigroup, Farmers Insurance also offers a dollar-for-dollar match via their 401K program up to six percent of eligible pay. To take this program to the next level, Farmers will also offer a four percent base contribution in addition to the dollar-for-dollar match.

You got that right. In the right scenario, you would be getting a 10% match from your employer while only giving six percent yourself. That is a highly incentivized program.

Southwest:

Any employee eligible for the 401K plan at Southwest Airlines can get a dollar-for-dollar match of up to 9.3 percent of eligible earnings. Now that is a huge chunk to take out of your check every week or every other week, but if a company is going to match it, you just have to do it.

This is the type of program that can allow you to retire at age 55 vs. age 65 if you play your cards right.

There are plenty of other companies with fantastic 401K match programs, these are just a few examples published recently. With the mindset of the younger generation putting “work, life, balance” in front of mind, you are going to see more and more decisions on employment made from benefits and retirement, not just salary.

It’s easy to fall in love with companies with the best 401K match, but remember, there are a couple of small items and “fine print” details that you should be sure to look at before agreeing to anything.

The first is the vesting schedule. Vesting simply means when the money is completely yours. There used to be a lot of employers that made you stay with the company for at least 12 months before becoming vested in the retirement program, but that has gone away to an extent.

It’s great to be vested right away or within 30-days, but don’t let a 12-month commitment hold you back either. Truthfully, you should give an opportunity at least a year before giving up anyway. You just want to make sure there isn’t a five-year amortization schedule or anything like that. I have seen a few places that vest your retirement account at 20 percent over a five-year period, which is a fairly punitive standard.

You should also take a look at the loan or withdrawal provisions of the company’s 401K program. Companies with the best 401K match and a forgiving withdrawal program are clutch. I’ve stated 100 times that you should never plan to withdraw from your retirement unless it’s an emergency, but emergencies happen.

My wife worked for a company where she could withdraw up to $5,000 a year with no penalty or interest, as long as it was paid back within 12-months. They would actually not even give you a chance to default and would take it right out of your check.

So, you did lose the gains from the investments that the money was in, but other than that it really didn’t cost you anything at all. I know a few guys who have gotten really creative with credit cards and 401K loans and have paid for their master’s degree with absolutely no interest. That’s a dangerous game, and certainly a next-level conversation.

Times are certainly changing; folks want to work from home, they want to only put in 40 hours, and they want to know that they will be set in retirement. Plus, they aren’t afraid to go to a few different places to find exactly what they are looking for.

Companies that pay the most salary may not always win, but companies with the best 401K match may start winning more and more battles to attract young talent.