Updated 9/25/2023

Some parts of GAAP accounting rules can be more tricky, and software and how it is depreciated can be one of those.

Most software is depreciated over a useful life, but there can be a type of software that is not depreciated (if it is considered R&D software).

First, let’s talk about depreciation and amortization, and then fixed and intangible assets– and how it all fits into software as an asset.

Table of Contents

- What is Depreciation? Amortization?

- Is Software a Fixed Asset?

- Is Software Depreciated or Amortized?

- GAAP Useful Life Table for Software (Examples)

Grab a cup of coffee, and let’s dive into this detailed, but important, accounting measure.

What is Depreciation? Amortization?

Depreciation, in its simplest explanation, is the spreading out of the cost of a big expense for a business.

You may also hear the word depreciation incorporated with amortization, which is essentially the same thing as depreciation but for intangible assets.

The deprecation of an asset does two things:

- Represents the (real) depreciation (or loss) in value of an asset over time

- Gives a more consistent representation of a company’s financials from year to year

Assets can lose value over time for a variety of reasons.

A more traditional physical asset, such as a piece of equipment or machinery used to manufacture products, breaks down over time as its parts get old—and must eventually be replaced.

Even a non-physical or intangible asset can lose value over time—a brand may become less popular with younger consumers, or a proprietary technology may lose value as emerging tech takes its place.

As such, companies need to reflect this reality in their financials, and so they depreciate the asset on the balance sheet over time. This reduces its value on the balance sheet as the years goes on.

Remember all accounting must reconcile, and so changes in the balance sheet need to be reflected in other financial statements. To reconcile this particular loss in value, the company takes a depreciation expense on its income statement.

The depreciation charge reduces Net Income for that year, as it is an expense.

Eventually, as the asset’s value approaches zero, the asset reaches the end of its useful life and no longer accrues depreciation charges.

Deprecation Is Useful: Example

Another benefit of depreciation in GAAP accounting is that it also provides more consistency, especially for earnings from year to year.

Say that a company wanted to expand its bubble gum production. They have a wildly popular new branded gum. So, they spend all of this year’s earnings on three new machines to increase output by 25%.

If there was no depreciation on this investment, the company would report $0 in Net Income for the year, because the money was all reinvested.

However, that doesn’t reflect the reality of the business. The company actually did earn a profit this year, and even though they are sacrificing profits now (large asset purchase), they were still profitable.

If it wasn’t for depreciation, the company would report very lopsided earnings over time. There would be huge profits in years with no reinvestment and then little earnings in the years with heavy reinvestment.

That’s why depreciation is a GAAP standard and becomes helpful in understanding the long term profitability of a company from year to year.

Is Software a Fixed Asset?

There are many types of assets that get depreciated over the years, and they can be defined either as a long-term fixed asset such as Plant, Property, and Equipment, or as an intangible asset / Goodwill.

These can include assets such as:

- Plant, Property, Equipment

- Land

- Buildings

- Machinery and Equipment

- Software

- Information Technology Assets

- Intangible Assets

- Brand power

- Intellectual property

- Patents

Accounting for intangible assets and goodwill is a little tricky as it relates to acquisitions, and its treatment for depreciation (amortization) is different than for fixed assets.

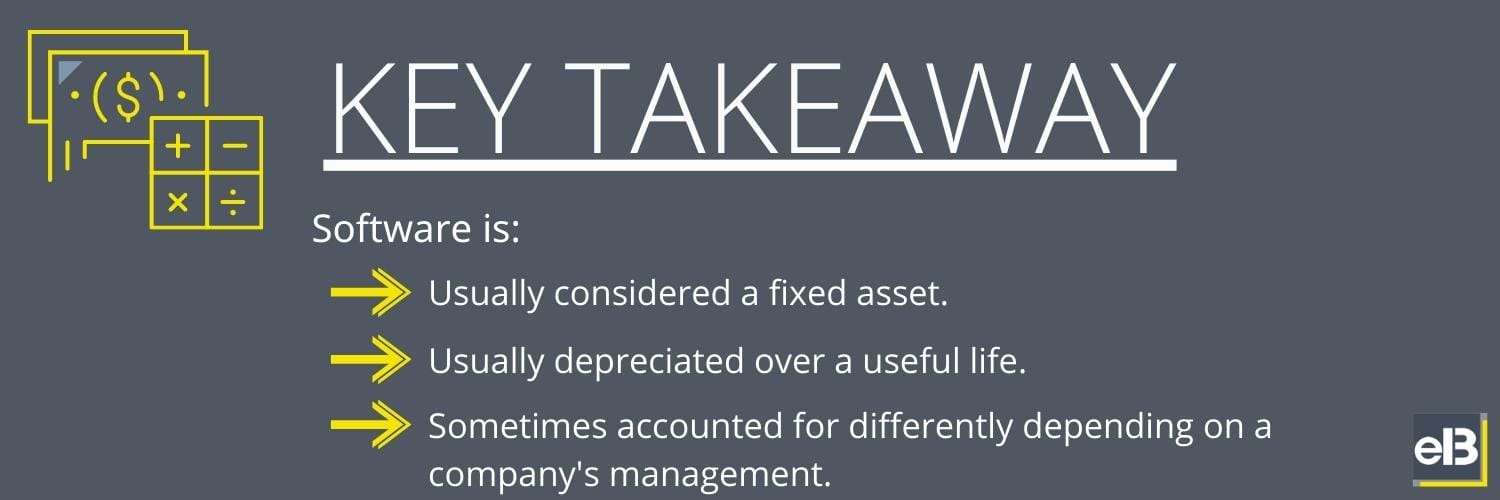

However, in the case of computer software, most companies report that as part of their fixed Plant, Property, and Equipment assets. Therefore, most companies consider software as a fixed asset.

Is Software Depreciated or Amortized?

Because software nowadays has become an integral part of business, it is now included as a fixed asset on most company’s balance sheets and is depreciated over a useful life. The depreciation is expensed in the income statement over time.

Other long-term assets such as intangibles, can be amortized unless those assets are considered to be “indefinite-lived”. Since the software is considered to be like a physical fixed asset with most companies, it is depreciated instead of amortized.

That said, companies like Apple have indicated that they amortize their internal use software (over 5-7 years), so it can really depend on how management decides to categorize the asset.

Caveat: R&D Software Is NOT Depreciated

However, if software is purchased for R&D (research & development), it is not allowed to be depreciated or amortized, since R&D expenses aren’t depreciated either. However, if the software can be proved to have other uses outside of R&D, then it can placed as a fixed asset and depreciated like previously discussed.

Acquisitions throw another wrench into the R&D capitalization conversation if a product was in the middle of being developed (In-Process R&D Expenses), but in general it’s good to know this important distinction between R&D software and “long-term asset” software.

GAAP Useful Life Table for Software (Examples)

Because there’s no GAAP standard for software depreciation, there’s also little in the way of clean datasets to filter metrics such as “useful life” or tangible vs intangible asset classification.

Taking some of the biggest companies in the S&P 500, and sifting through their annual reports (10-k’s) for 2021, I found the following “useful life” categorizations for software:

| Company | Software “Useful Life” (2021) |

|---|---|

| Apple | 5-7 years |

| Microsoft | 3-7 years |

| Johnson & Johnson | 3-8 years |

| Procter and Gamble | 3-5 years |

| Home Depot | 3-7 years |

Note that not every company will disclose the useful life of their software assets, or may not depreciate them at all, even if they seem to obviously drive a lot of value from it.

Companies like Facebook, Amazon, Netflix, and even Google and NVIDIA have no disclosure in their 2021 annual reports about software depreciation useful lives, and either say that they don’t capitalize any software development costs, or don’t disclose any specifics at all.

Investor Takeaway

GAAP accounting can get confusing when you go past the general metrics and dive into the specifics. But much of the mystery and ambiguities can be found right inside the Notes to the Financial Statements, which really emphasizes their importance.

When it comes to computer software depreciation, it seems like the business world is becoming more and more digitized every single day.

And with these encompassing greater portions of business models, the accounting rules around software will become that much more critical in evaluating the fundamentals.

Like with many other key details of reading a company 10-k, understanding software depreciation is one of those things that’s important when it’s important.

Meaning, applying your knowledge about the topic won’t make a difference most of the time. But when it does come time to either spot irregularities, or evaluate real earnings power on large depreciation charges, the information here can be priceless.

Or, you could even say, intangible.

Andrew Sather

Andrew has always believed that average investors have so much potential to build wealth, through the power of patience, a long-term mindset, and compound interest.