The economy moves in cycles. Good times and bad. Because of this, the stock market also tends to move in cycles. A cyclical industry is simply one where profits move up and down along with the economy.

Examples of cyclical industries include ones which depend on consumer spending or business investment.

They include, to name a few:

- Retail, Home Builders, Travel Services

On the other hand, a non-cyclical industry is one where profits aren’t generally tied to the economy. In other words, they will generate revenues regardless of whether the economy moves up or down.

Examples of non-cyclical (“defensive”) industries include the bare necessities of life:

- Grocery stores, Tobacco, Farm products

Big themes will tend to drive many cyclical industries. You can usually tell if an industry is cyclical if they depend on the real estate market, discretionary (non-essential) spending, or business investment for growth (such as marketing).

Which Industries Are Cyclical?

In the stock market, companies are categorized by sectors and industries. According to Morningstar, there are 11 sectors which an industry will fall into, and are either cyclical, non-cyclical (“defensive”), or somewhat cyclical (“sensitive”):

- Basic Materials

- Tend to be cyclical because they are tied to construction and industrial expansion.

- Examples include commodity metals and miners like BHP Group Ltd, Rio Tinto, and Freeport-McMoRan.

- Examples include chemicals companies like Sherwin-Williams, Air Products and Chemicals, Dow Inc, and DuPont de Nemours.

- Financial Services

- Tend to be cyclical because they tend to fund increased expansion, investment, and liquidity.

- Examples include payment processors and credit cards like Visa, Mastercard, American Express and Discover.

- Examples include banks like JPMorgan, Bank of America, Wells Fargo, and Morgan Stanley.

- Consumer Cyclical

- Is very cyclical for obvious reasons; when customers have more money they spend on these goods and services.

- Examples include retailers like Amazon, Home Depot, Alibaba, and TJX Companies (“TJ Maxx”).

- Examples include auto makers like Tesla, Toyota, Ford and GM.

- Real Estate

- Is usually very cyclical because consumers tend to buy or upgrade their homes when the economy is booming and incomes are high.

- Examples include real estate investment trusts (REITs) like Prologis, American Tower, Simon Property Group, and Digital Realty Trust.

- Examples include real estate services companies like CBRE Group, CoStar Group, and KE holdings.

- Communication Services

- Are cyclically sensitive because they can depend on business investment like marketing, but include communication necessities like cell phones.

- Examples include internet content companies like Google (now “Alphabet”), Facebook (now “Meta Platforms”), and Twitter.

- Examples include telecom services like AT&T, Verizon, and T-Mobile.

- Energy

- Is more cyclically sensitive because demand tends to be higher in good times, but can also be more profitable depending on supply, which can have nothing to do with the economy.

- Examples include oil & gas majors like Exxon Mobil, Chevron, and Shell.

- Examples include oil & gas midstream companies like Enbridge, Enterprise Products Partners, and TC Energy.

- Technology

- Tends to be cyclically sensitive because some of these companies supply critical business services, while others are more tied to discretionary consumer spending.

- Examples include software companies like Microsoft, Adobe, and salesforce.com.

- Examples include semiconductor companies like NVIDIA, ASML Holding, and Broadcom.

- Industrials

- Are cyclically sensitive because some of these industries rely on economic expansion, while others provide the backbone of everyday life.

- Examples include freight and logistics companies like UPS, Union Pacific, and Fedex.

- Examples include aerospace and defense stocks like Raytheon, Lockheed Martin, and Northrop Grumman.

- Consumer Defensive

- Is non-cyclical because it includes goods and services which are necessities for everyday life.

- Examples include discount stores like Walmart, Costco, and Target.

- Examples include household and personal products like Procter & Gamble, Estee Lauder, and Colgate-Palmolive.

- Utilities

- Is non-cyclical because people need to power their homes regularly, and that demand doesn’t fluctuate like the economy does.

- Examples include major regional utilities Duke Energy, The Southern Company, and Dominion Energy.

- Examples include renewable energy producers like NextEra Energy, First Solar, and Brookfield Renewable Partners.

- Healthcare

- Is non-cyclical because people always need to take care of their health regardless of what the economy is doing.

- Examples include health insurers like UnitedHealth, Aetna (owned by CVS), and Anthem (Blue Cross Blue Shield).

- Examples include biotech and drug manufacturers like Johnson & Johnson, Pfizer, and Moderna.

Why Are Certain Industries So Cyclical?

This great explanation in McKinsey and Co’s textbook on Valuation explains:

“Cyclical companies are characterized by significant fluctuations in earnings over a number of years. Earnings of such companies, including those in the steel, airline, paper, and chemical industries, fluctuate because of big changes in the prices of their products. In the airline industry, for example, cyclicality of earnings is linked to broader macroeconomic trends. In the paper industry, cyclicality is largely driven by industry factors, typically related to capacity.”

When businesses tend to compete on price instead of any other characteristic of a product or service, that price can fluctuate at a much higher rate.

The reason behind this is that when there’s no differentiation between a product, then a customer’s only logic is to buy the one at the cheapest price.

Understanding Supply, Demand, Capacity, and Cyclicality

Products with no differentiation, like commodity inputs, will all have to lower their prices to capture customers.

At a certain point though, a price can’t fall forever or it will put all of its producers out of business. So, a floor gets set to cover the costs of producing/manufacturing.

If price drops so low to be unattractive to new competitors, supply drops and only the strongest producers survive.

Once the weak players are flushed out and the survivors ramp up supply again to fill demand, prices can start to rise again as demand outpaces the lowered supply.

This continues in a virtuous cycle, up and then down and then up again as supply and demand move in their own up-down cycles.

These cycles do not tend to happen over days but years, especially in industries with long construction times and investment costs.

When to Buy Cyclical Stocks

Cyclical stocks can be hard to invest in, especially those that are super cyclical. That’s because you generally want to buy super cyclicals when they are in a period of bust rather than boom.

This is tough because when the economy is strong and profits are healthy, these stocks might seem to trade at better value precisely because their profits are so high.

It’s up to investors to differentiate between earnings that are lasting versus those that are cyclical.

For example, if you buy a stock with a low P/E ratio but cyclical earnings, you might see those earnings disappear in the next downcycle, making future growth weak and bringing down the true intrinsic value of the company.

Some industries are much more cyclical than others; you have to factor that in.

For an easy way to determine the cyclicality of an industry, look at a 20-year time period of earnings and notice how much they swing.

I like to use the premium version of Quickfs to instantly download a 20-year history of a stock’s financials. Looking over a longer time period helps you observe both an up cycle and a down cycle, which is key to knowing when to buy a cyclical stock.

In general, a company with average cyclicality will drawdown this much:

- Revenues = -15%

- Operating Income = -30%

Drawdown simply means the maximum amount it will fall, and these numbers are based on a wide range of companies over the last 20 years.

So, if a company has bigger revenue and operating income (“EBIT”) drawdowns than those averages, then they are probably more cyclical.

And vice versa.

Example of Measuring the Cyclicality of an Industry

To get really nuanced with it, I used some historical data to compare stock returns and DCF valuations.

If you don’t know the meaning of DCF, click here to skip this section.

Then I used a correlation coefficient function in Excel to measure companies’ previous results and valuations.

A company whose Free Cash Flows (FCF) did not correlate with higher stock prices would have a correlation coefficient around 0, those negatively correlated would move closer to -1, and those that are positively correlated would be closer to +1.

In other words, a super cyclical company might have FCF negatively correlated with stock returns, because buying with high FCF represents buying at the top of an up-cycle.

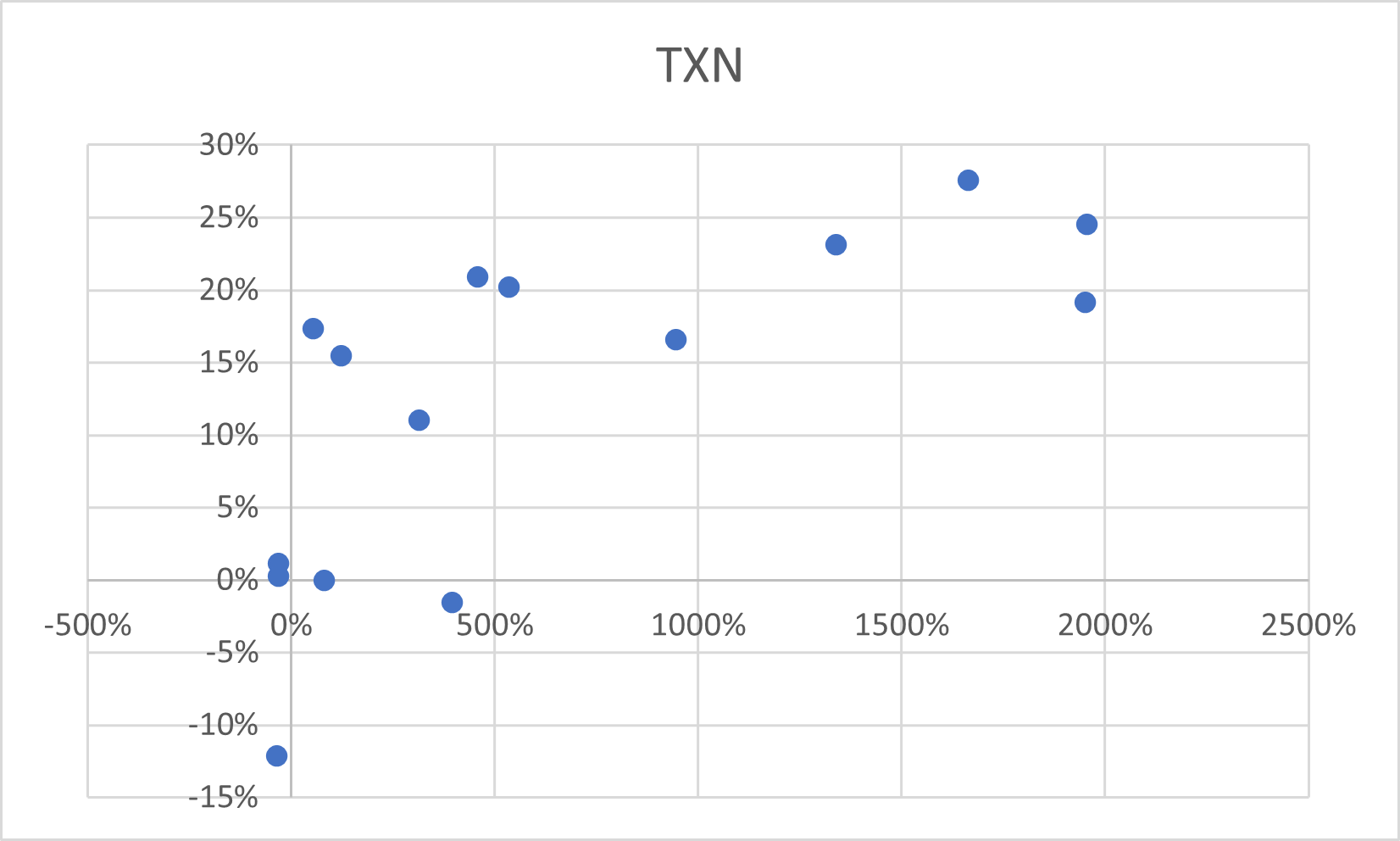

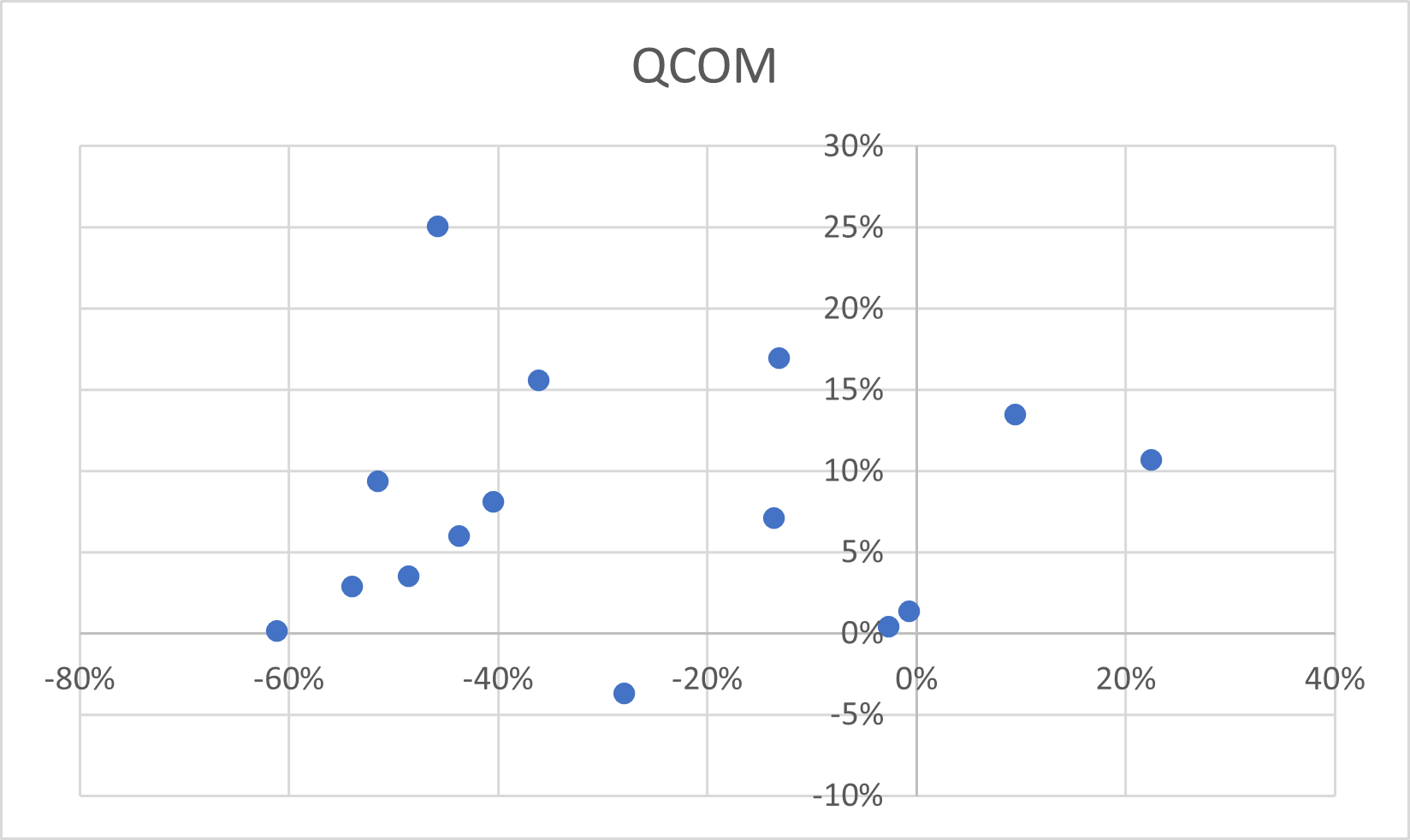

Here’s my results for the semiconductor industry:

(I adjusted the DCFs to account for changing interest rates, which affect the discount rate and overall valuation. The x-axis represents a Margin of Safety, where +100% means the company came back undervalued on a DCF. The y-axis represents stock price returns).

NVIDIA (NVDA)

- correlation coefficient= 0.53

- NVIDIA’s history seemed to suggest average cyclicality. Sometimes higher FCF meant higher stock returns, sometimes it meant lower future returns.

Texas Instruments (TXN)

- correlation coefficient= 0.70

- Texas Instrument’s FCF was very tied to future stock returns, which suggests that traditional valuation metrics like P/E and a DCF worked very well for investors “buying low”.

- Texas Instrument’s revenue and operating income drawdowns were also much lower than average, suggesting the company is less cyclical than some of its semiconductor peers.

Qualcomm (QCOM)

- Correlation coefficient= 0.07

- Qualcomm’s historical earnings and FCF results had pretty much nothing to do with its stock price returns. This suggests a company with super cyclicality, and one that would be extremely hard to value.

How to Value Cyclical Companies

At the end of the day, you want to be careful about getting too excited about low valuation ratios with a company in a super cyclical industry.

Instead of looking at last year’s earnings, you can look over a longer period of time and use that in your valuation ratio.

One way that the great valuation teacher Aswath Damodaran recommends is to look at a company’s operating margin over a long period of time, over an up-and-down cycle, and average it out. A company’s long term operating margin is their “normalized” margin, and you can apply that to its latest revenues as a starting point to estimating its future Free Cash Flows.

You can also use a longer term historical growth rate to project its future Free Cash Flows, so that you are accounting for the higher growth cyclical upswings and the lower growth down cycles.

Investor Takeaway

There are many different ways to look at valuing a company in a heavily cyclical industry, and it comes down to the fact that their earnings and free cash flows are much more volatile than a non-cyclical company.

I’ll leave with a great quote from Peter Lynch, which pertains to the valuation of companies in a cyclical industry quite well:

“In cyclicals, a period of silly prices is followed by a period of sobriety.”

The great value investor Benjamin Graham also had a great quote related to this, where he said:

“You do not gain as much from periods of unusual prosperity as you lose in periods of depression when you are in business. That is almost an axiom”.

Do you think cyclical companies make for great investments over the long term? Do you agree with Benjamin Graham and Peter Lynch’s assessment of business cycles? Reply to this thread on Twitter:

For more advanced thoughts on the topic of valuations (how to value a stock), be sure to check out some of our more popular posts, such as:

- How to Calculate P/E Ratio: The Most Widely Used Valuation

- Explaining the DCF Valuation Model with a Simple Example

Good luck out there, and I hope you now have more insight on cyclical and non-cyclical industries.