One thing that I have heard many times before is that we are in an ETF bubble. Personally, I kinda see both sides of the coin on this topic, but I know that it’s something that we should really think about it when we’re investing.

First off, what is an ETF? Per Wikipedia, it is “an exchange-traded fund (ETF) is a type of investment fund and exchange-traded product, i.e. they are traded on stock exchanges.”

Another name for ETF is an index funds as they are really used for synonyms for one another. Some common examples of ETFs include the following:

- Total Stock Market ETFs

- VOO – S&P 500 ETF

- IWM – Russell 2000 ETF

- QQQ – Nasdaq 100 ETF

- DIA – Dow Jones ETF

- Market Sector ETFs

- JETS – Airline Stocks ETF

- Specific Goal ETFs

- TQQQ – Triple leveraged Nasdaq ETF

The different ETFs that you can find are honestly endless. Personally, I like to use ETFs for two different reasons:

1 – If I am investing some money in an account that I want to be “safer” than picking individual stocks. This primarily is just my HSA just in case something tragic happened and I needed to rely on that money for health reasons.

2 – I am starting to look at a specific type of stocks that I want to get some exposure in but don’t feel confident enough to pick an individual stock. I just went through a really thorough example of this when I invested in WCLD while looking for some cloud exposure.

Other than that, I typically will stay away from ETFs. Not because they’re necessarily bad but mainly because I like to think that I can outperform the market if I spend some time analyzing companies and making sure that I am picking companies that are undervalued today vs. what I anticipate their future value being.

But the question remains – are we in an ETF bubble?

And honestly, I do really think that it’s a valid question to ask.

Michael Burry, who has become famous for his role in the Big Short, which is one of my favorite stock market movies ever, says that this ETF investing by so many people might also be a bubble in itself!

As he was quoted on this Investors.com article, Burry says:

“This is very much like the bubble in synthetic asset-backed CDOs before the great financial crisis in that price-setting in that market was not done by fundamental security-level analysis, but by massive capital flows.”

Honestly, I kind of get what he’s saying! So many people will simply invest a certain percentage of their paycheck into the stock market every time they get paid, and while I think that’s an amazing think for the individual, they’re blindly buying a group of stocks without having any idea about the valuation of the market.

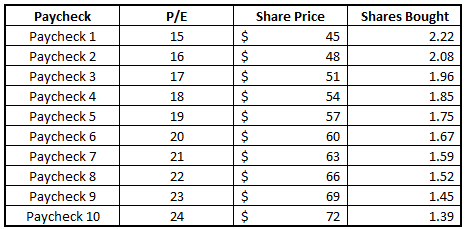

To make it clearer, let’s think about it with just one stock, let’s say the ticker is OUCH (this is made up).

I get paid every 2 weeks from my employer and I decide that I want to put in $100 into OUCH every time that I am paid. I don’t worry about the company at all – I simply just put my money into that stock and let it ride.

Well, let’s also pretend that the P/E of the company is currently 15 but the true value of the company is something that is higher than this, let’s say at a P/E of 18.

*Side Note – if you’re unfamiliar with P/E, or the Price/Earnings ratio, checkout these valuation ratios before proceeding with this example. It’s a key concept to understand with all investing*

Basically, the situation that I have described would play out just like this:

The thing that I love is that you’re consistently putting money to work in the market! The thing that’s scary in this example is that the share price is continuing to go up by $3 every time that you invest, and assuming that earnings of the company aren’t changing, that means the company slowly reached the “properly valued” status and now is way overvalued by your last paycheck.

“Andy – who cares if it’s overvalued as long as the share price keeps going up?”

I don’t disagree! If the share price keeps going up, then being overvalued means nothing. But the reason that we care about if a stock is overvalued or not is because if it is overvalued, then chances are it’s going to come crashing down back to reality at some point!

So how does this impact you?

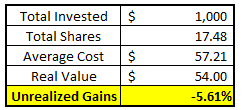

Well, let’s pretend that after Paycheck 10 the stock crashed back down to its properly valued level of 18, meaning a share price of $54. $54 is still 20% above the price you initially bought in at – a great win!

But since you continued to blindly invest into the stock, you were buying shares of the company when it was way overvalued as well:

In total, your $1000 bought you just under 17 ½ shares at an average cost of $57.21, meaning that you actually are losing nearly 6% on your investment when your initial purchase was a 20% winner!

Truthfully, this is one of the main reasons why I recommend lump sum investing over dollar-cost averaging because these situations are not that uncommon, but the reason that I walk through this example is because this is what people are doing with index funds as well!

People blindly put money in every time they’re paid and for the individual investor, I love the simplistic mindset!

I get paid à I invest for my future without thinking about it. It’s an amazing concept and a great routine to get into!

The issue is that people will blindly put their money into index funds without really even thinking about anything at all. They don’t think about what’s going on in the market and it can lead to them buying ETFs that buy companies that are primarily invested in overvalued stocks, meaning that a downturn is inevitable!

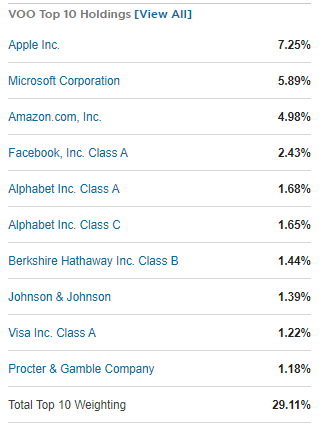

But do you know what you’re even buying? If you buy $100 worth of VOO, a very common S&P 500 ETF, over $18 of that $100 is invested in Apple, Microsoft and Amazon:

I’m not necessarily saying those are bad companies, and in fact I am really saying the opposite because if they have grown to such large positions in the S&P 500 then that means they’re doing something right, but that doesn’t mean that they’re not overvalued, either.

But the fact that 9 companies make up 29% of an S&P 500 ETF, meaning that the remaining 491 make up the last 71%, is a bit scary to me! What happens if Apple suddenly was crushed? You’re going to see the entire “market” drop just because Apple was hit hard.

So, to keep a bit of a running tally here – my concerns so far about ETFs are:

- People buy into them blindly without regard for valuation

- The top holdings are way too concentrated amongst a few companies

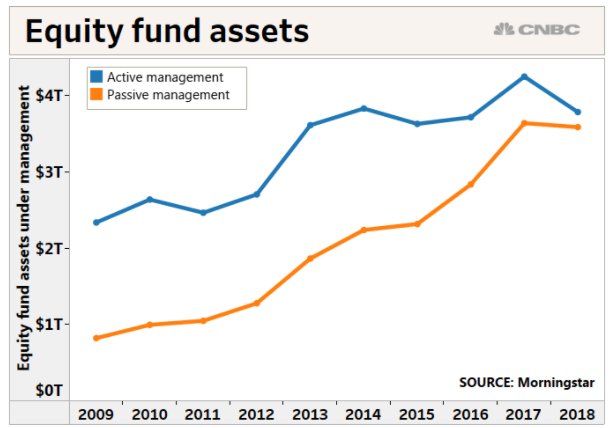

The next thing that is really concerning to me is that the amount of funds that are invested into the stock market through passive management (ETFs, Index Funds, Mutual Funds, etc.) is growing at a SUPER rapid pace.

The chart below from CNBC shows that the amount of passively managed funds has grown from under $1 Trillion in 2009 to about $3.5 Trillion as of 2018!

Now, the actual dollar amounts that are being invested actually makes me really happy because that says that more people are investing now than in 2009, which isn’t a huge surprised because of the Housing Market Crash of 2008, but still good to see.

The area that I am concerned with is that the distance between the “Active Management” and “Passive Management” lines has shrunk so far to being nearly nothing, and for all intents and purposes, I would say that it’s a 50/50 split.

So, again, that means that 50% of the market is buying into funds that are meant to mimic the returns of the stock market…which might be super overvalued because we just keep pumping and pumping and pumping more money into the market…blindly!

It’s almost like a Ponzi scheme lol. I mean, I obviously don’t believe that, but if you get a new investor to put money into the market, then the demand goes up and the share price should reflect that, right?

Conspiracy Theory Andy is coming out today… ?

I mean, it’s a known thing that when a stock is added to the S&P 500, and therefore the S&P 500 ETF like VOO, the stock is going to get some sort of a bump from that. Investopedia explains it better than I can, but in essence, shares have to be bought of this new company that is joining the S&P 500 that didn’t previously have to be bought.

If OUCH is added to the S&P 500, then everyone that owns VOO now is going to own some OUCH as well, despite it being a small amount, so it’s simply increased demand that is continuing to drive the value of these companies up.

So, let’s recap now with my updated concerns:

- People buy into them blindly without regard for valuation

- The top holdings are way too concentrated amongst a few companies

- Funds that are invested into the stock market through passive management is growing at a SUPER rapid pace

And now we’re off to my last thought, which has no data, but just pure experience from myself and my peers that I talk to regularly – the experience of the investor.

A newer investor is more likely to invest in an ETF because they might want to completely avoid trying to be a stock picker, and I don’t blame them! I mean, I talked about how when I am learning a new industry, I will buy an ETF that has some exposure to that industry prior to picking individual stocks because it feels safer while I can get my feet wet.

The issue with this is that newer investors also tend to be the most “panicky” per se. They’re the ones that are most likely to sell at a low point and then buy back in at a high point. They don’t have the experience and faith that the stock market does always go up…in the long-term!

Sure, I have some short-term, speculative, “fun money” investments, but a LARGE majority of my portfolio is based on the long-term and is one that I will actually try to buy even more when the market drops.

If Apple drops by 30% then I am not selling my shares – I am actually going to “borrow” from my emergency fund and buy even more Apple shares and then replenish my emergency fund later. Basically, I am just trying to take advantage of what the market is giving me.

But newer investors will not do that. Newer investors will get sick seeing their portfolio drop and sell out, only to never invest in the stock market again. Selling low and then not getting back in?

Double Whammy!

Instead, they should be adding more funds to their portfolio, even to ETFs. But, just as when someone buys $100 of VOO and $7.25 of that goes to Apple, when they sell their VOO, they’re selling those Apple shares as well – it goes both ways.

That blind buying is also the same on the downside when it comes to blind selling. Nobody is evaluating every single company in the S&P 500 and going, “Oh, I’d like to buy 2.43% of Facebook and 1.39% of Johnson & Johnson, and I don’t know…maybe 1.22% of Visa!”

People are just buying the market and trusting those historical returns of 10%+ that they have become used to!

And that’s completely fine – I’m not advising against using ETFs to invest. What I am advising is for you to understand some of these potentially dangerous pitfalls that could come from this rapid trend towards passive investing.

Is it a bubble? I don’t think I would go that far…but is it something that could drastically affect your returns? Yes, I 100% think it is.

Do me a favor and just use ETFs the way that I do – some introductory exposure to new industries and once you become familiar with that industry, pick individual stocks. It might sound hard, but it’s not – let me show you!