The following is a list of our most influential posts and guides in the Investing 101 category. We hope you’ll find these lessons to be incredibly valuable and most importantly, take action on what you learn to create wealth in your life.

A list of essential posts for investors to internalize:

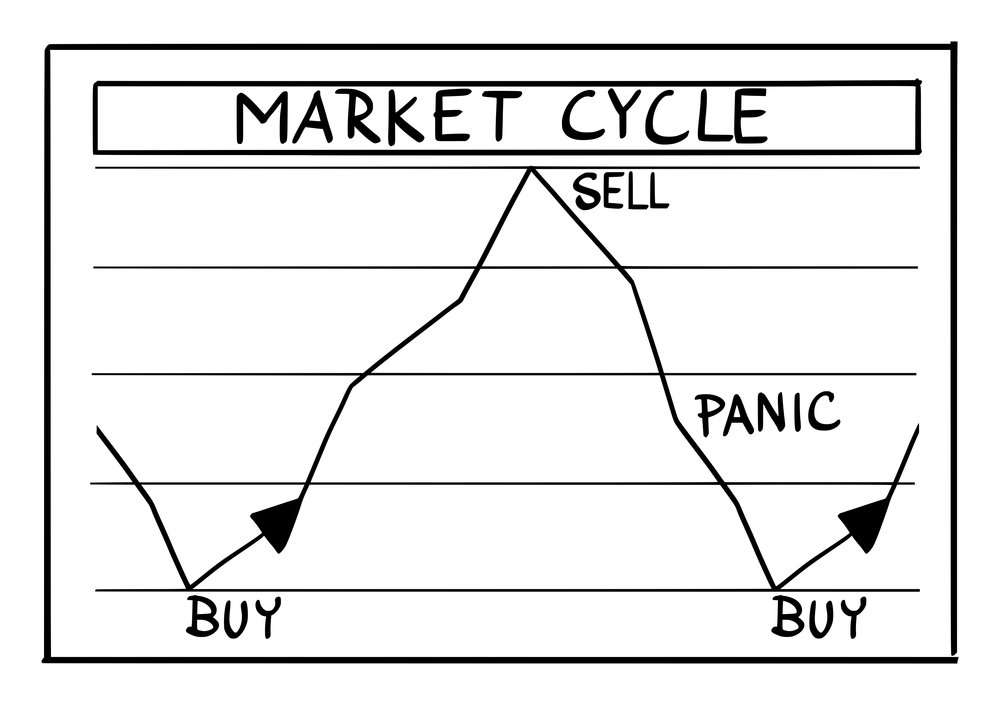

- How the Mr. Market Metaphor Helps Investors Buy Low and Sell High

- 20 INCREDIBLY Eye-Opening Investing Truths for 20 YEAR Olds ?

- The 7 Deadly Sins of Behavioral Finance (Common Biases that Investors Face)

And of course, about America’s favorite investor… Warren Buffett:

- The 7 Ground Rules for Warren Buffett’s Partnership that Led to 24.5%+ Gains

- Warren Buffett Investing Quotes on Simplicity, Price, Value, and Wisdom

More great posts about legendary investors (including interviews):

Here’s 2 deeply in-depth guides on mastering investing strategy:

- Circle of Competence: Maximizing Results by Identifying Biases and Strengths

- Second-Order Thinking: A Critical Component of Smart Investing