“Using precise numbers is, in fact, foolish; working with a range of possibilities is a better approach.”

Warren Buffett shares much of his investing wisdom in his annual letters to shareholders, including his thoughts on calculating intrinsic value.

His favorite analogy is the Aesop fable that a bird in the hand is worth more than two in the bush. Buffett spends a lot of time explaining his investing philosophy to those interested in learning. It stems from the ideas he learned from Benjamin Graham and The Intelligent Investor.

Graham lays out his ideas surrounding investing in the book both from a defensive and enterprising viewpoint. Graham, conservative and aggressive investors must build safety margins in the case we are wrong about our analysis.

Remember that using formulas to find the intrinsic or fair value is the starting point of research. Graham only mentions his formula and spends multiple chapters laying out his investment framework.

As Buffett and Munger like to relay, it is better to be approximately correct than precisely wrong.

In today’s post, we will learn:

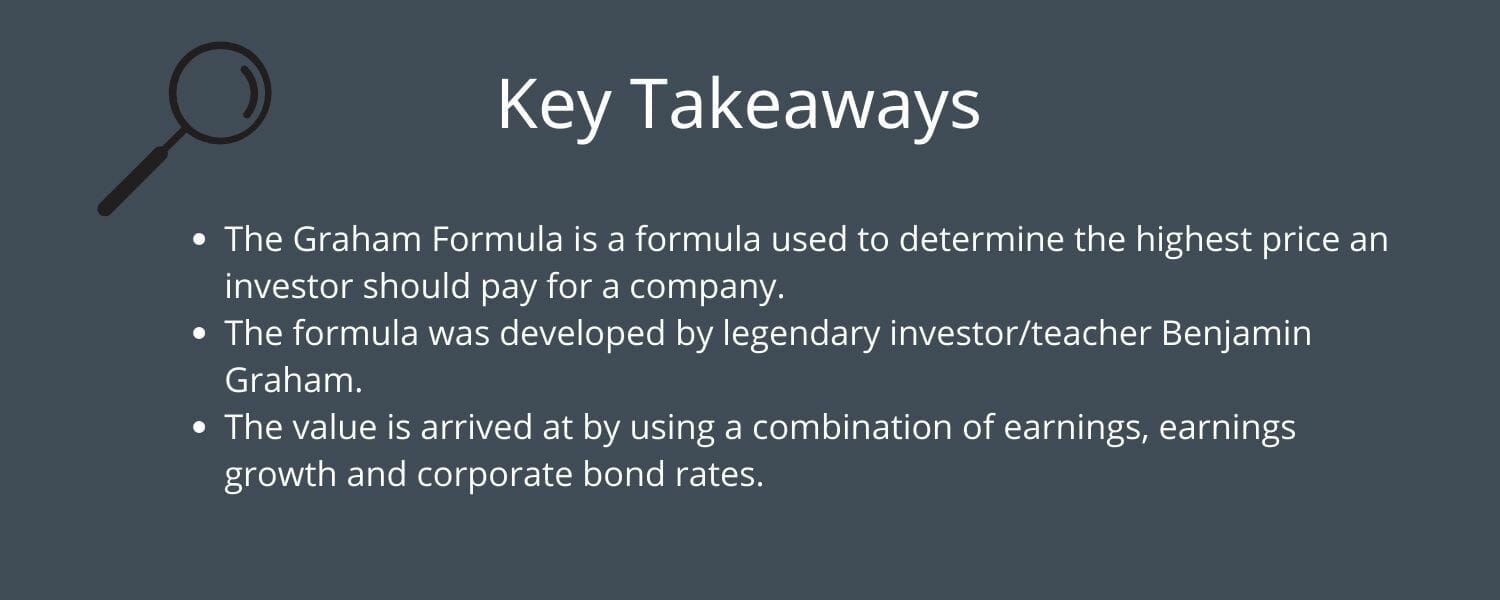

- How Does Benjamin Graham Value Stocks?

- What is the Graham Formula?

- How to Use the Graham Formula with Examples

- Investor Takeaway

Okay, let’s dive in and learn more about the Graham Formula and how to use it to value stocks.

How Does Benjamin Graham Value Stocks?

For those unfamiliar, Benjamin Graham was a portfolio manager and professor who wrote the seminal book, The Intelligent Investor. Most consider the book the bible of value investing and laid most of the framework that investors such as Warren Buffett, Walter Schloss, Mohnish Pabrai, and Seth Klarman use today.

According to Graham, value investing determines a company’s stock’s intrinsic or fair value separate from the market price.

Graham uses publicly available information such as assets, earnings, liabilities, and dividends to determine the company’s intrinsic value and then compares that price to its market price.

If the intrinsic value exceeds the current market price, the investor should purchase its stock, as it is selling at a bargain.

The above idea spells out the idea of a margin of safety. Graham refers to a margin of safety in Chapter 20 of The Intelligent Investor. He details the idea of finding and buying securities for less than their intrinsic value.

The reasoning behind the idea is that humans are fallible creatures, and we make mistakes in judgment, carry biases and tend to get overzealous about ideas we love.

By building in a margin of safety, we don’t allow those human frailties to greatly harm our investments.

Think of it this way: when we buy a car, we spend time researching the car, its safety record, reliability, and long-term value. And when we arrive at the dealership, armed with the knowledge about what we hope to buy, we all want to buy more car value for the dollars spent.

The easy way to think about value: we all want a deal. Everyone wants to buy something of value and pay less for the item.

The same rules apply regarding the stock market, or at least they should. Ben Graham understood this, so he created his rules to help all investors find the margin of safety and avoid overpaying for stocks.

In addition to using a formula to find a margin of safety, Graham also mentions that investors can achieve the same results by buying companies with good dividends and low debt and diversifying their portfolios.

The whole idea behind the margin of safety is to reduce the potential losses from bankruptcy, which is the total loss of investment.

For more on Benjamin Graham’s idea of investing and his rules, please check out the two posts below:

Defensive Investors: Rules from the Classic Book, The Intelligent Investor

The Enterprising Investor Portfolio Policy – Ch 7 of the Intelligent Investor

What is the Graham Formula?

The original formula that Graham highlights in the book are:

V = EPS x ( 8.5 + g ) / y

Where:

- V equals the intrinsic value

- EPS equals the earnings per share on a trailing twelve months (TTM)

- 8.5 is the P/E ratio of a stock with zero growth

- g equals the growth rate of the earnings over a long period, such as seven to ten years

- y equals the current yield on AAA corporate bonds

In 1974, Graham adjusted the formula to include a risk-free rate of 4.4%, the average corporate bond yield in 1962. The other inclusion was the current yield on AAA corporate bonds, represented by the letter y:

As we can see from above, the formula is essentially the same, with a few tweaks.

The first is the risk-free rate, which during Graham’s time was 4.4%, which is why we divide that by the AAA corporate bond rate to adjust that formula to the present day.

Calculating intrinsic value in twelve months can lead to miscalculations; using longer periods, such as five or ten years, remains far better. Using normalized earnings over at least five or ten years will help smooth the results. Using a one-year could lead to over-exuberance if the company had a spectacular year. Likewise, a poor year could lead to high pessimism.

I have seen other adjustments moving the company’s P/E ratio to a more reasonable number. If you feel that the zero growth of a more conservative stock is reflected with a P/E of 7, then by all means, use that number.

The growth rates you use will have a huge impact on the output of the formula. We can use the analyst projected earnings from your favorite website, Stratosphere, Gurufocus, Seeking Alpha, or whoever.

Make sure to use longer periods such as five years; another great way to utilize growth rates is to look at the five-year historical growth rates.

Second, the Graham formula is the upper limit of companies’ valuation, and if we adjust the formula, we can find more comparable values.

How to Use the Graham Formula with Examples

Let’s start to put the formula to use to find the value of a few companies. While doing the calculations, we will look at various values to determine what we think is the best.

Remember, valuation remains part art, part science. The science part remains easy, plugging in numbers and doing calculations. The art part is far more difficult because it is qualitative, and much of the final decisions are up to your intuition and experience.

Okay, let’s start to put this into practice.

I will walk through the first several examples to find the intrinsic value using the Graham formula, with both variations, to see which we think is more realistic.

Visa Graham Formula example

The first step is to find the 30-year corporate bond rate. To do this, I use YCharts; to track these rates.

The current rate is 3.94%, which we will use for all our formulas.

The next step is to find the earnings for Visa over five years. For me, I will use Seeking Alpha to gather my data.

2018 | $4.44 |

2019 | $5.33 |

2020 | $4.90 |

2021 | $5.64 |

TTM | $6.38 |

The third step is to normalize those earnings above, adding up the totals and dividing by the years, which is five.

After normalizing the earnings, we arrive at a value of $5.34 per share.

Next, we look at the earnings growth, both from analysts and historical data and then we can plug all of our numbers into the formula to find the fair value of Visa.

Earnings growth:

- Analyst estimates – 17.52%

- Historical five-year average – 15.90%

Now, we can plug our numbers into the Graham formula:

Normalized earnings | $5.34 |

Analyst earnings | 17.52% |

Historical earnings | 15.90% |

30-year AAA bond rate | 3.94% |

V = 5.34 x ( 8.5 + (2 x15.90% ))x 4.4 / 3.94%

V = $240.94

Now, let’s do the same with the analyst estimate of earnings growth.

V = $5.34 x ( 8.5 + (2 x17.52% )) x 4.4 / 3.94%

V = $254.94

Now, let’s compare those results to the current price of Visa.

Historical | $240.24 |

Analyst | $254.54 |

Current Market Price | $200 |

Based on our calculations for Visa, the company might be undervalued, but we always have to do more due diligence before pulling the trigger.

On another side note, I created a new calculator you can use for free with a download here:

Microsoft Graham Formula Example

First, let’s figure out the historical growth rate for Microsoft over the last five years.

Year | Earnings per share |

2018 | $2.15 |

2019 | $5.11 |

2020 | $5.82 |

2021 | $8.12 |

TTM | $9.65 |

The normalized five-year earnings for Microsoft is $6.17, and the historical growth rate is 11.6%, with the analyst’s estimated earnings growth of 15.97%.

Now that we have our numbers, we can plug those into the calculator.

V = $6.17 x (8.5 + (2 x15.60%))x 4.4 / 3.94%

V = $218.42

And if we use the analyst earnings growth estimates:

V = $6.17 x (8.5 + (2 x 15.97%)) x 4.4 / 3.94%

V = $278.65

If we compare the above results to the current market price of $260.7, Microsoft is selling more than it is worth.

The two examples appear overvalued or undervalued depending on which earnings we use, but as noted earlier, the Graham formula was created before either company existed. Let’s try it with more established companies that would have existed during Graham’s time.

Aflac Graham Formula example

The first step is the earnings growth for Aflac, which is trading at $55.90.

Year | Earnings per share |

2018 | $3.77 |

2019 | $4.43 |

2020 | $6.67 |

2021 | $6.39 |

TTM | $6.09 |

The normalized earnings for Aflac over the five years is $5.47, with the historical growth rate based on the difference between the starting year, 2018, and the normalized five-year rate resulting in a growth rate of 6.59%.

The reason for using the normalized earnings is that Aflac had a historical outlier in 2020, with earnings more than doubling, which would have given us a historical outlier of 13% earnings growth for an insurance company.

The analysts’ earnings expectations for Aflac are 7.03% over the next three years.

Now that we have all of our numbers, we can calculate the fair value of Aflac.

V = $5.47 x (8.5 + (2 x 6.59%) x 4.4) / 3.94%

V = $132.53

And if we use the analyst estimates:

V = ($5.47 x (8.5 + (2 x 7.03%)) x 4.4 / 3.94%

V = $137.91

As we can see from the above calculations, it appears that Aflac is undervalued and has some serious share appreciation possible. Again, valuing the company without doing our due diligence is not advised.

Northrup Grumman Formula example

For the last example, I would like to use Northrup Grumman. Looking at the normalized earnings for the last five years, we have a value of $26.10, with the historical growth based on the normalized earnings of 5.58%. The analysts estimate Northrup Grumman will grow earnings by 5.14% over the next five years.

V = $26.10 x (8.5 + (2 x 5.58%)) x 4.4 / 3.94%

V = $573.12

And the analyst estimates:

V = $26.10 x (8.5 + (2 x 5.14%)) x 4.4 / 3.94%

V = $547.47

Both show Northrup might appear undervalued compared to the current market price of $459.62, with a margin of safety if our calculations are wrong.

Investor Takeaway

The intrinsic value calculations we performed are easy to use, with simple inputs. However, Graham never intended that the formula be used as the main source of investment analysis.

Instead, he created the seventeen different rules outlined in Chapters 14 and 15 in The Intelligent Investor. The rules he outlines in the chapters cover the gamut of ideas he proposes, such as security analysis using the companies’ financials, plus reading through all available literature regarding the company.

Graham understood there are two types of investors, defensive and enterprising, which he equates to conservative and aggressive. And with that understanding, he created two different frameworks for both types to outline the depth of analysis each should perform.

All of this was done before behavioral economics or finance was even a thing; he understood that not everyone wants to spend their time analyzing stocks to the degree needed to succeed.

Graham himself said:

“Note that we do not suggest that this formula gives the “true value” of a growth stock, but only it approximates the results of the more elaborate calculations in vogue.”

He also warns the material is to be used as an illustration only because the projection of future earnings growth is a guess at best. He warns us basing any investment solely on future growth estimations can lead to failure.

Graham highlights that growth estimates have no high relation to reliability and can sometimes be wrong.

Instead, Graham suggests we pay much more attention to the guidelines he establishes in Chapters 14 and 15 as our framework for finding great investments.

Some hindrances regarding the Graham formula don’t account for assets, liabilities, debt, or free cash flow. It only focuses on earnings and their growth, which allows for manipulations of earnings.

The considerations of these items are quite important to the analysis of any company. The Graham formula should indicate whether earnings growth will increase the company’s value.

Next, let’s return to the idea of valuation as an art. Say we give five different people a box of crayons. All five people will draw different designs and use different combinations of colors.

The crayons and paper we draw on are the quantitative side of valuation, the tools we use to find the best investment.

We use the different colors and images to create our masterpiece as the qualitative or subjective side of valuation.

We put both sides of the equation together by interpreting our numbers, projecting the company’s possibilities forward, and determining our narrative for the company.

It combines all that is the art of valuation, part numbers, and part narrative.

Many new investors get bogged down in finding the “perfect” number. The number doesn’t exist because of so many moving parts involved in running a company, plus the trading variables in the stock market—all of those line up to give us a moving target.

Far better is to look at a range of possible values and create narratives on possible upside and downside for the company. You are basing everything on the financials and what you know about the company.

Professor Aswath Damodaran understands more than anybody; he knows the numbers and how to make it all work. But years ago, he discovered building the narrative to think through the numbers was just as important.

In fact, he wrote a whole book on the subject, Narrative and Numbers, which I highly recommend you check out!

With that, we will wrap up our discussion of the Graham formula; please remember it is a tool in our toolbox, not the final answer.

As always, thank you for taking the time to read today’s post, and I hope you find something of value in your investing journey.

If I can be of any further assistance, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave

Dave Ahern

Dave, a self-taught investor, empowers investors to start investing by demystifying the stock market.