Updated: 9/21/2022

There are retail investors and institutional investors. Real estate, stocks, and bonds. And then you have mounting worries about the influence of institutional investors on real estate prices.

To try and contextualize these, this post will break down the following [Click to Skip Ahead]:

- Why Are Institutional Investors Moving into RE?

- How Interest Rates Played a Part in the Institutional Imperative

- By How Much Are Institutional Investors Buying Up Real Estate? (Pt. 1)

- By How Much Are Institutional Investors Buying Up Real Estate? (Pt. 2)

- Key Takeaways

Note that all of the statistics are estimates; they are from credible sources but they might not be 100% accurate due to the difficulty of measuring both public and private wealth.

Going back to real estate, there are ample worries about the move of institutional investors into both residential and single family homes and commercial real estate which was traditionally owned by owner/operators rather than faceless investors. And the reasons are not unfounded—this has been a growing trend recently.

Why Are Institutional Investors Moving into RE?

We have to understand the big picture of money in order to understand this growing phenomenon. And we have to understand who exactly institutional investors are.

You can think of institutional investors as stewards of large piles of cash; some common institutional investors include:

- Pension funds

- Sovereign wealth funds

- Asset managers

- Insurance companies

- Central banks

Each category of institutional investor can come into stewardship of their large piles of cash in various ways.

For example, even though pension funds are fading away in the private sector, they still play a big role for public (government) employees. These are funded by taxpayers generally, and each fund will have a manager who must invest that funding into assets which can pay out the liabilities as people retire.

Insurance companies sort of face a similar reality—in their case, the company collects premiums from customers and invests those for income. They must make smart investments in order to keep enough liquidity to pay off any future claims from their customers.

Even central banks can get into the ballgame; even though central banks like the Federal Reserve primarily buy U.S. government bonds, they have also historically purchased investments such as MBS (mortgage backed securities) which have tranches of real estate as the underlying assets for these investment vehicles.

Asset managers play a huge role as institutional investors as well, as they have been reported as managing as much as $100T in AUM and can manage the money of wealthy individuals or even other entities like pension funds or endowments and the like.

How Interest Rates Played a Part in the Institutional Imperative

Traditionally, institutional investors had an “easier” time managing their large piles of cash due to decent interest rates across the entire spectrum of assets.

This is because when interest rates were higher, they could take very little risk and still meet their financial obligations.

For example– if pension retirees were promised income equivalent to a 4% return, and the pension fund can earn 5% investing in a government bond, the pension fund can just buy those and pay off their obligations while still growing in size.

Everything changed when interest rates dropped to close to zero.

Now all of a sudden, pension funds couldn’t buy government bonds yielding 1% to make payments on 4%, because eventually it would run out of money.

Institutional investors had to find other places for stable yield—thus the move to real estate.

By How Much Are Institutional Investors Buying Up Real Estate? (Pt. 1)

This becomes a much harder question to answer. Like I said before, all of the statistics about market size and wealth are estimates, and must be especially with something (real estate) in which every single asset is not priced in a market every single day (in contrast to the stock market).

However, we will do our best.

We can see in a recent Global Wealth Report that Credit Suisse had estimated a $463.6 trillion size for all of the world’s wealth, with Savills attributing around $280 trillion to Real Estate (in 2021).

How much of this is owned by institutional investors? Here are a few estimates of total wealth from some of the largest institutional investors (by category):

- Pension and Sovereign Funds ~ $11 trillion (source)

- Global asset managers ~ $100 trillion AUM (source)

- Insurers ~ $26.8 trillion AUM (source)

- Billionaires ~ $8 trillion net worth (source)

- Central banks ~ $30 trillion (source)

- Hedge funds ~ $3.8 trillion AUM (source)

Then of course we have retail investors (everyday people) and corporations and businesses (publicly traded and private) which can also own lots of real estate and assets.

Unfortunately, it’s not as easy as adding up all of our estimates for institutional investors above and subtracting it from the Real Estate total value.

Much of the value of Real Estate could be completely hidden out of view.

Let’s take a HNW (high net worth) individual as an example, with about $10 million in wealth.

Say that this person has $3 million in savings/investments, around $4 million tied up in a small business, and $3 million in a real estate property.

Maybe this rich person has a mortgage on the real estate, with $500,000 in equity. So although this rich person owns the real estate, there’s still $2.5 million due on a loan to a bank. This mortgage will end up on the balance sheet of the bank, which may or may not repackage and sell it to another investor (or Fannie/Freddie).

Maybe the $3 million in savings/investments for this rich person is being managed by a private wealth manager such as BNY Mellon.

And maybe this rich person’s small business owns a piece of commercial real estate which also carries its own loan.

So within just this one example, we have our $10 million man with part of his wealth represented as an individual (with a personal residence), some of it represented by institutional investors (through the private wealth manager), and some through institutions or privately held (through the business’s ownership of commercial real estate, or through institutions if the business rents the property).

What a mess, right?

Then you have the publicly traded corporation’s role in (commercial) real estate.

Due to accounting rules, publicly traded corporations are required to record the value of any real estate owned outright as its value at cost.

So regardless if land purchased by a public corporation was purchased 20 years ago and has appreciated 100%, that value is still recorded at its original cost.

That means that estimating the value of real estate held by public corporations in addition to the difficulties in estimating those held by institutional investors and retail investors/small businesses/individuals is also extremely difficult and has its own problems.

Combine that with the presence of REITs (Real Estate Investment Trusts), whose sole purpose is to raise capital and buy real estate and are also publicly traded and subject to the GAAP accounting rules on real estate, and the mess becomes messier even still.

By How Much Are Institutional Investors Buying Up Real Estate? (Pt. 2)

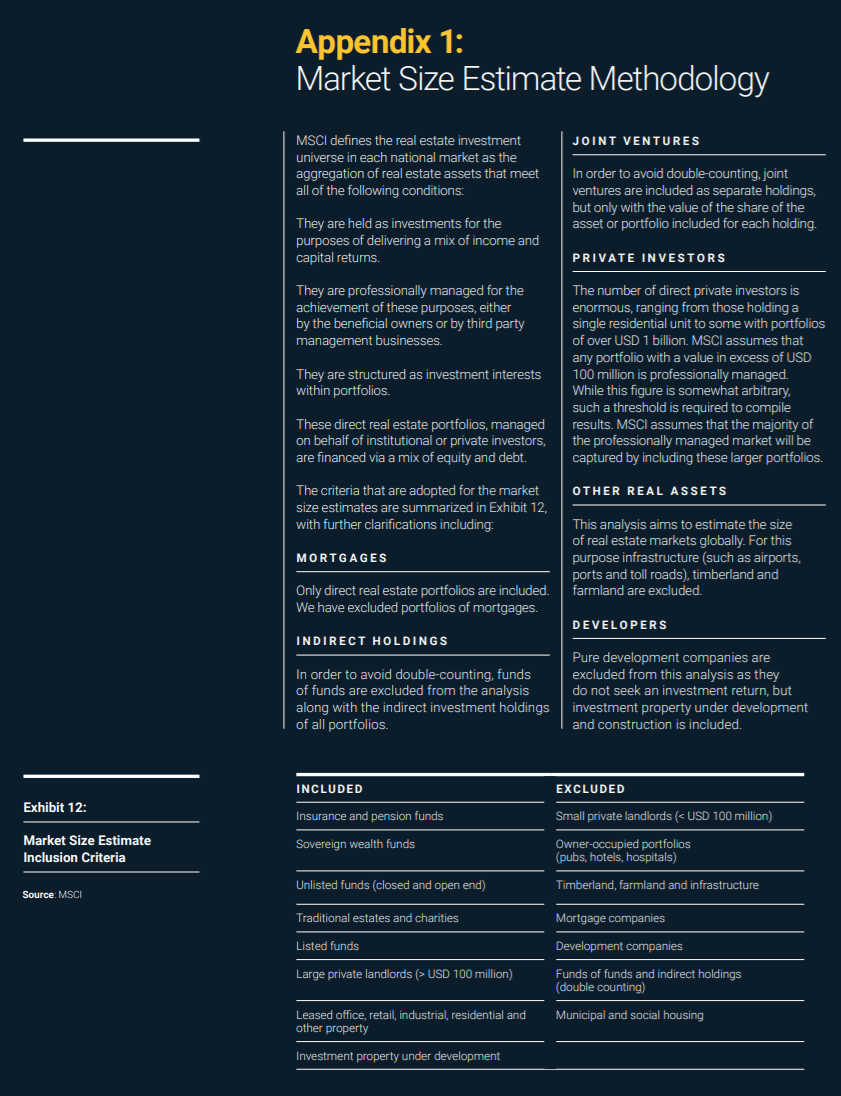

The closest thing I could find after some fruitless and frustrating searching was this recent report by MSCI about the Real Estate Market Size for 2019/20, specifically “investable” real estate.

The company came up with an estimate of $9.6 trillion for 2019, up from $8.9 trillion one year prior.

Here’s how they defined “the real estate investment universe” globally:

I’ll highlight that basically these were properties purchased specifically for income and/or capital appreciation, which fits the narrative for institutional investors’ yield hunting.

It’s likely that much of this almost $10 trillion market is being swallowed up by institutional investors.

However, this research implies that the percentage of Residential Real Estate ($220T) being gobbled up by institutional investors is relatively small, while it’s a much more significant percentage compared to a market such as Commercial RE ($33T).

Some examples of the land owners who were included in this $9.6T estimate:

- Pension and sovereign wealth funds

- Insurance company funds

- Large private landlords

Some examples of the land owners excluded from the $9.6T estimate (making up the vast majority of the remaining global real estate market):

- Owner-occupied

- Small private landlords

On the one hand, I saw another investor stating “at the end of 2018 less than 500 institutional investors owned approximately 84% of the entire global real estate market.”

I really doubt the validity of the second statistic especially considering all of the other statistics and estimates we’ve looked at in this post.

But the reality could lie with one of these extremes or the other, or it could be somewhere in between.

Key Takeaways

I’d be remiss if I didn’t at least highlight that although the size and scope of the institutional investor presence in the global real estate market is most likely relatively small today, that doesn’t mean that it will continue that way or that they don’t currently have a large presence in certain markets.

Industrial real estate in particular looks to have some steep competition, particularly as a similar evolution seemed to happen in industrial plants formerly owned by corporations and largely sold off during the mid 1980’s to early 1990’s.

A source like a commercial realtor has much better visibility into the true environment of these markets than an outsider looking at big picture numbers as I am, and so this trend should be watched closely.

If published sources seem to be reporting on these kind of changing winds, it’s also the logic behind the drivers of real estate ownership and investment which seem to confirm this sort of a movement.

Think about it.

A lender would be much more likely to offer an attractive rate on a property-tied loan to a large institutional player such as a commercial RE private equity fund than a small mom and pop shop with little in liquid assets.

This means that over time, those with better access to cheaper capital should have competitive advantages over the small players, driving them out and essentially eradicating them from the market.

But the world of finance and investing doesn’t always come down to cost of capital and the bottom line.

Companies, owners, and users of real estate are comprised of individual people at the end of the day, and they might not share the same institutional imperative of sole focus on returns on capital and the bottom line when making financial decisions.

And the interest rate environment could change again, which could reverse this trend in a very similar fashion to what has put us here in the first place.

It is all interesting points to consider and does help explain why institutional investors are increasingly being linked to real estate investments.