Updated 7/6/2023

Global mergers and acquisitions (M&A) volumes hit a record high in 2021, overtaking 2020’s deals. According to Refinitiv data, the total volume of completed deals and those in the pipeline is $3.6 trillion in 2021, with three months to go, passing the $3.59 trillion of 2020.

Mergers and acquisitions are on the upswing, typical during bull markets; the longer the market, the more companies look for acquisition targets or mergers.

But how much, as investing beginners, do we understand mergers and acquisitions beyond the excitement and hype we see from analysts on TV?

Today, we will uncover some of the basics of mergers and acquisitions and learn how they work, what drives companies to undertake this activity, and shareholders’ impact.

In today’s post, we will learn:

- What are Mergers and Acquisitions?

- What are the Reasons For Mergers and Acquisitions?

- An Example of a Merger & Acquisition Process

Okay, let’s dive in and learn some mergers and acquisitions basics.

What Are Mergers and Acquisitions?

First question, what the heck is a merger and acquisition?

Mergers and acquisitions are a broad term that combines two companies’ assets through various financial transactions such as mergers, acquisitions, or consolidations.

In financial circles, it also is a term that refers to the investment bankers that specialize in mergers and acquisitions for the bank, either on buying or selling side.

So why would companies want to go through this process?

There are several reasons, but the main reason is that many companies are looking for strategic ways to grow by acquiring proprietary tech or combining the strengths of market leaders. For the seller, it allows them to cash out and live on a beach or share in the possibilities of the new company.

The big idea behind mergers and acquisitions in the two companies isn’t as valuable as they are together.

We can use these terms in conjunction, but they mean different things. For example, an acquisition is one company buying another, whereas mergers combine two companies that become a new entity.

A few recent examples of the difference would be Microsoft’s purchase of LinkedIn, which folded that business under Microsoft’s umbrella, and the merger of Chrysler and Daimler changed the company’s name to DaimlerChrysler.

As we can see, Microsoft continued as a standalone company by acquiring or buying LinkedIn, where the others combined to create a new business. In the merger of equals, Daimler and Chrysler created a new company, with both companies surrendering their stock for the new company stock.

There are six types of mergers to consider:

- Mergers – In a merger, the board of directors for both companies approves the combination and works to get shareholders’ approval.

- Acquisitions – the acquiring company buys a majority stake in the acquired company while not changing the original name or structure of the purchaser.

- Tender offers – in a tender offer, one company offers to buy another’s stock at a preset price instead of the market price. The acquirer communicates directly to shareholders, bypassing the management and board of directors.

- Acquisition of assets – here, one company buys another company’s assets, barring shareholders’ approval. Acquisitions like this are typical during bankruptcy proceedings, with other companies bidding on the assets as the bankrupt company attempts to liquidate.

- Management acquisitions – these types of acquisitions occur when management is working to take the company private. The corporate executives buy a controlling stake in the business, and approval from most shareholders is a must.

- Consolidations – A consolidation creates a new business from two separate core businesses. Shareholders must approve the deal and receive shares in the new company.

The structuring of mergers and acquisitions comes in many different flavors. To learn more about these structures and how it affects our investments, check out the below link:

The 5 Types of Mergers and Acquisitions and Its Impact on Your Investments

What Are the Reasons For Mergers and Acquisitions?

Why do companies go through all this? Does it sound like a ton of work?

Management and the board would want to take on this effort for multiple reasons. Remember that combining two companies creates more value for the company and shareholders. Many companies merge or acquire others to improve efficiency or take a larger market share.

Let’s explore some of these ideas briefly:

- Improve the target company’s performance: One of the most common reasons for M&A activity is to improve the target company’s performance. Think of it this way: if you buy a company and increase its cost efficiency, improve its margins and cash flows, or improve its revenue growth.

Those improvements greatly increase the value of the target company and, by proxy, the acquiring company.

- Create more efficiency: as companies mature, they tend to create excess capacity, and many companies combine to capture that efficiency by reducing capacity in the industry, which in turn drives up prices.

- Accelerate distribution of products and services: in the SaaS world, tons of small companies offer innovative products or services, but their scale is small enough that they can’t expand enough to get their name out there. Bigger companies can acquire smaller companies and use their bigger distribution networks to accelerate their services and products. These ideas are popular in the pharmaceutical industry and common in the tech world, i.e., software.

- Acquire innovative tech or skills at a lower cost: many companies can buy the tech or skills they need to compete in an industry at a lower cost than they would to build them on their own. A great example is Cisco, the king of acquiring new tech to build their platforms; over the years, Cisco acquired companies to help fill out their platform to stay competitive in the internet tech industry.

- Pick winners early: many companies will make acquisitions early in the life cycle of a new industry or product line before the industry or product grows to a larger size. Many in the pharmaceutical industry, such as Johnson & Johnson, employ this practice. One pitfall is you need to make many bets because not every company will succeed.

An Example of a Real-Life Merger and Acquisition Explained

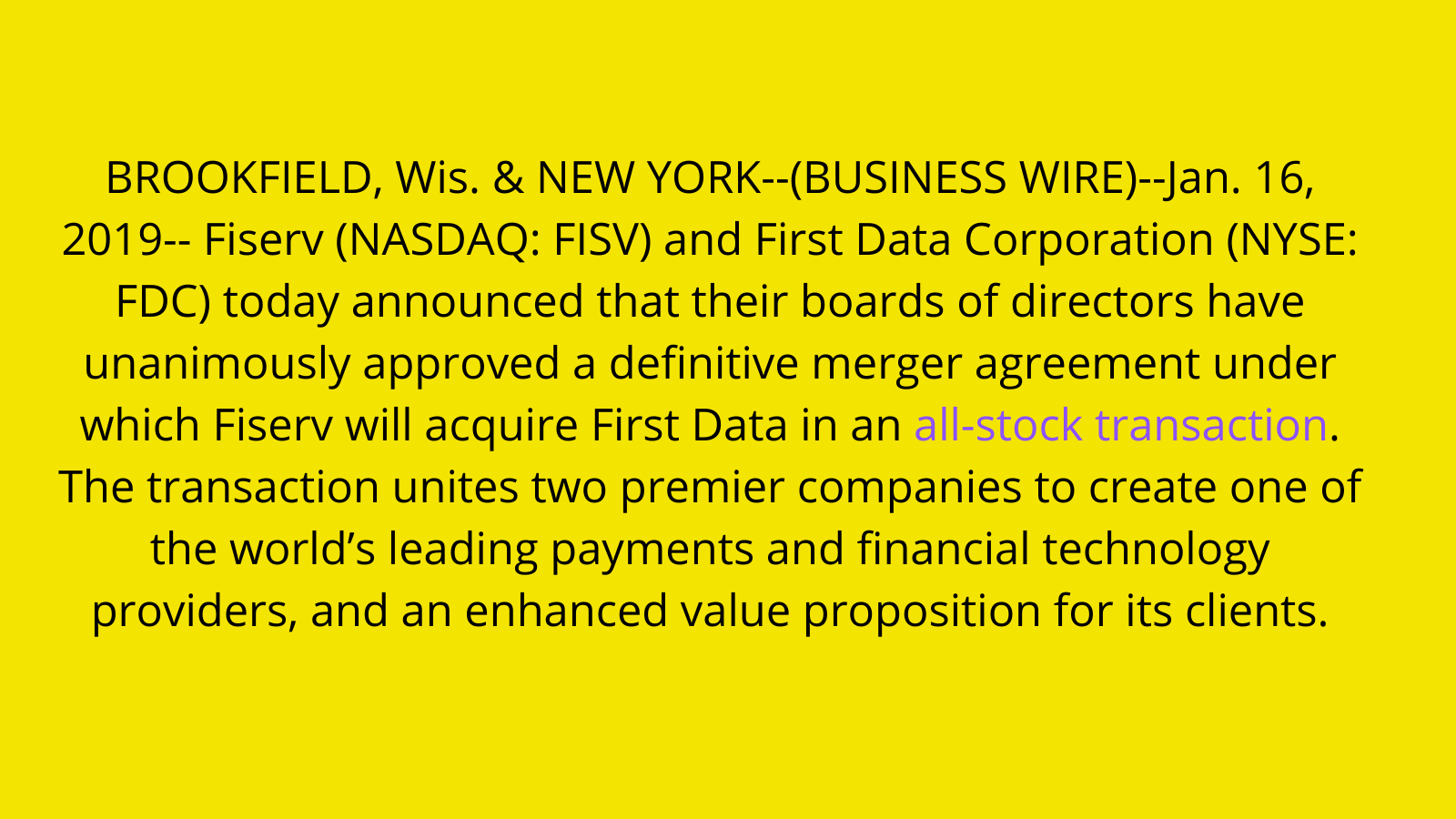

The best way to understand the M&A process is to look at a real-life example, and for our guinea pig, we will look at the recent merger of First Data (FDC) with Fiserv (FISV), which occurred on January 19, 2019.

First Data and Fiserv operated in the same financial industry, focusing on core banking and merchant payment solutions. The expectations of the merger of two equals will bring technology and distribution outlets for both companies over time.

Barring media leaks, generally, the first investors learn about any merger or acquisition is through a press release issued from both companies, which is how we learned about the upcoming merger of First Data and Fiserv. You can download the press release here.

From the start, we see a few things:

- The combined company will have a new CEO and Chairman, with the First Data CEO becoming president and joining the board.

- The company expects many synergies, such as revenue and cost efficiencies, in the next three years.

Financing the transaction

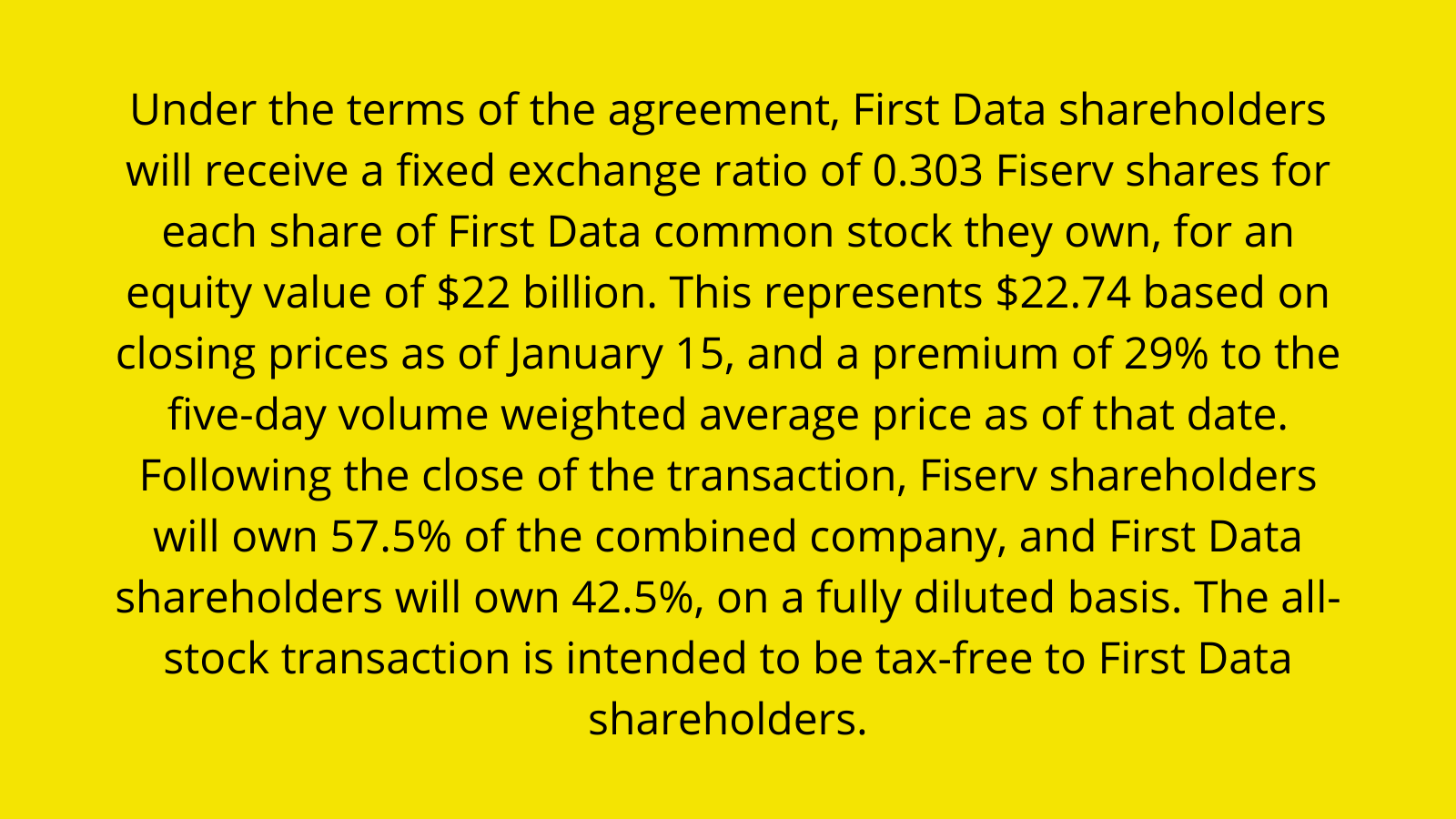

The following data we want to determine is how the merger was accomplished, cash or stock or a combination?

We can see from the above shows the merger was an all-stock transaction. The First Data shareholders will receive Fiserv shares in the transaction; the next press release highlights the transaction.

Premium Paid

The press release lays out what kind of premium the First Data shareholders receive, a 29% premium. Unfortunately, that is not always the case, and sometimes we need to research the price of the acquired company five days in advance to determine the premium.

The premium exists because for the shareholders of the acquired or merged company to agree to the transaction, they would naturally expect some premium for giving up their rights as a company shareholder.

Studies have shown that the lower the premium paid, the more possible value creation for existing and continuing shareholders in the long run.

According to Bloomberg, 10-50% of premiums are the norm, with 30% being the industry standard.

Company Structure

The deal’s structure is up next, and as we saw from the first line screenshot, the boards of both companies unanimously agreed to the terms of the deal to merge, under which Fiserv will acquire First Data in an all-stock transaction.

It also shows that the current CEO of Fiserv will take control of the new company as CEO and chairman of the board, while the current CEO of First Data will remain president and COO and join the board of directors.

The bottom line, both the company boards approved the merger and settled on the new company’s leadership in the future.

These announcements are common in a friendly merger or acquisition, with both companies announcing jointly in a press release. The press release would only come from Fiserv if it were not a pleasant transaction.

Shareholder Approval

Buying or selling a whole company is a big deal, and it isn’t enough for only the board and management to sign off on the deal. For the deal to go through, 50% or more of a company’s shareholders must approve the deal and, in some cases, a supermajority.

Upon further reading of the press release, we see that:

In addition, after reading through Fiserv’s proxy statement from the same period, we see that the company needs a 50% majority to approve the merger.

If you are unsure where to look in the proxy, a simple search method is using the CTRL-F function or Command-F on the Mac. It works wonders; I live and die by the search command.

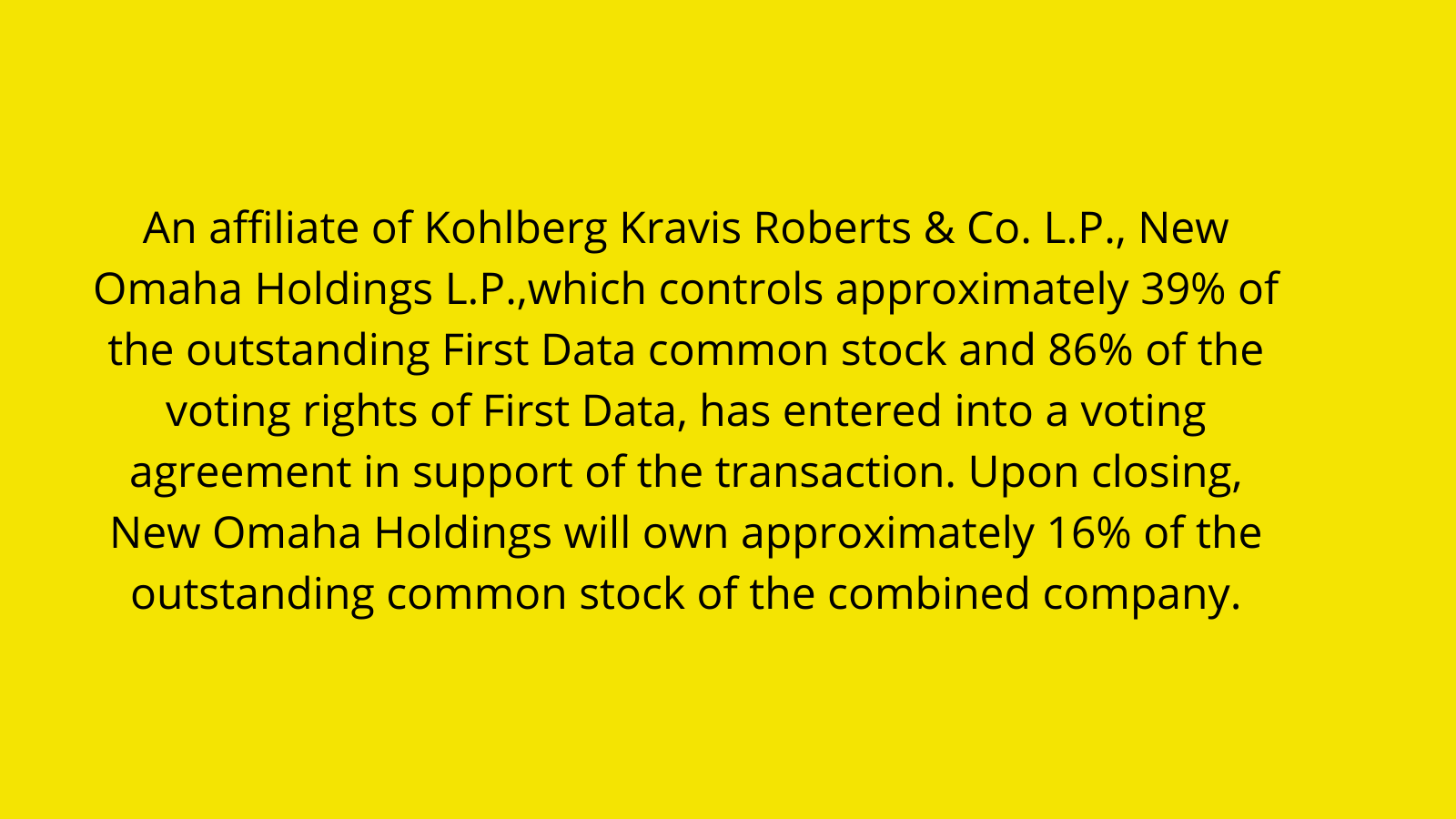

By combining the information from the press release and proxy, we see that one of the major shareholders of First Data has already signed off on the deal. Still, it is contingent on voting from Fiserv’s shareholders to approve the deal.

In some cases where the CEO/owner controls more than 50% of the company, many mergers or acquisitions bypass this step because majority shareholders approve it.

In Fiserv’s case, no majority shareholders approved the merger before the announcement, and the company needed to hold a vote at its next annual meeting, which they announced in their proxy filings.

Looking further into the ownership of Fiserv, we see that 43% is in investment firms such as Vanguard, T. Rowe Price, and Blackrock—only 1% ownership from insiders, CEO Jeff Yabuki.

We have been dealing with the press release for information regarding the Fiserv/First Data merger. But there are additional documents we can dig into to learn more about the deal.

In a public merger or acquisition, which is our focus, there will be two additional documents we can use:

- The merger proxy

- The definitive agreement (merger agreement)

Merger Proxy

Because Fiserv must receive shareholder approval before the merger can finalize, it must file a proxy statement with the SEC. If the vote concerns a merger, the proxy is a merger proxy, and a merger prospectus if the vote includes stock. The filed document is a DEFM14A.

The merger proxy and agreement layout in more detail the terms of the deal, including:

- Conditions that would trigger the break-up fee

- If the seller can solicit other bids(go-shop or no-shop)

- In what situation could the buyer walk away(material adverse effects)

- How shares will convert to acquirer shares

- What happens to acquirer options and restricted shares

Additionally, there is lots of fun legalese describing all the ins and outs of the deal-making, company projections, and other details that can be important, so wade in with both hands and a cup of coffee.

A few comments about a couple of terms above:

- The breakup fee refers to a buyer’s payment if the deal falls through based on conditions agreed to in the merger agreement.

- No-shop refers to locking up the agreement and not allowing the buyer to shop with other competitors looking for a better deal. If the buyer breaks the deal by shopping for others, it automatically triggers the breakup fee.

- Material Adverse Effects refer to different clauses and conditions that help protect both buyer and seller during the gap between the announcement and closing of the deal.

Definitive Agreement

After distributing the press release to all the media outlets and their website, companies will also issue an 8-k through the SEC to announce the official acquisition or merger. The 8-k document will typically include the merger agreement in full and any other relevant information.

Investor Takeaway

When Fiserv sought to merge with First Data, it looked like a merger of equals, as the market caps for both were similar. But the merger would allow one company’s strengths to complement the other’s strengths and make a stronger company in the future.

When companies acquire or merge with other companies, there are many different reasons, and understanding those strategies and methods will help better understand the reasons. Understanding those reasons helps investors better anticipate how those acquisitions will help their current and future investments.

Capital allocation is one of the most important skills a CEO must possess, and learning the ins and outs of M&A will help us analyze a CEO’s decisions and their impacts on the company’s returns.

If the CEO pays too much for an acquisition, it could backfire and hamper the company’s returns for many years, and we lose out on better returns with another company. It is important to understand how the management uses the capital the company creates and what kind of returns they earn. Long-term value creation comes directly from that capital, and the best capital allocators are the best companies to own, i.e., Warren Buffett and Mark Leonard.

And with that, we will wrap up our discussion on merger and acquisition basics for beginners.

As always, thank you for taking the time to read today’s post, and I hope you find something of value in your investing journey. If I can further assist, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave