A return on any investment refers to the return of capital achieved over a certain period of time. In financial statement analysis, we are using many different ratios to understand how effectively a company is using its assets or its resources to generate a profit and create value for its shareholders. Yet, some of the most commonly used ratios are the return on equity (ROE) and the return on assets (ROA).

Editor’s Note: This is a guest contribution by Christina Pomoni.

Understanding Return on Equity

Return on equity is a financial indicator that shows how efficiently a company uses the funds invested by its shareholders to generate additional earnings. Put simply, it shows the relationship between the firm’s net income to the funds available during a fiscal year to estimate the performance level of own funds.

ROE is expressed in percentage points, and it is calculated as:

ROE = Net Income / Shareholder’s equity

Given the fact that ROE is calculated for common shareholders, preferred dividends, if any, are excluded from the calculation of the net income. Therefore, if a company has a shareholder’s equity of $12 million, a net income of $1,25 million, and it pays $125,000 in dividends to preferred shareholders, the ROE calculation should be as follows:

Net income = $1,250,000 – $125,000 = $1,125,000.

ROE = $1,125,000 / $12,000,000 = 0.0937 = 9.38%.

Practically, this means that the company has achieved 9.38% return on equity from the funds invested by its shareholders. Hence, every dollar of common shareholder’s equity earned about $9.4 in this fiscal year.

What is a good ROE?

ROE is not the same for all industries. Capital-intensive industries like shipping, automobile, or airlines require substantial amounts of capital for expensive equipment and raw materials.

Conversely, labor-intensive intensive industries like insurance or banking require more human capital than physical assets to achieve a higher level of performance. Also, there are industries that require R&D, and their ROE should be adjusted for the R&D expenses.

Due to the particular nature of each industry and the different accounting practices used in each, ROE should be used for comparing firms that operate in the same sector or industry.

The Dividend Effect

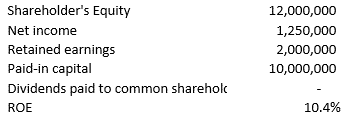

Dividend payments reduce the shareholder’s equity on the balance sheet through retained earnings. For example, assume that company A does not distribute any dividends. Also, the sum of its retained earnings and paid-in-capital is the shareholder’s equity. Therefore, the ROE is $1,1250,000 / $12,000,000 = 10.4%.

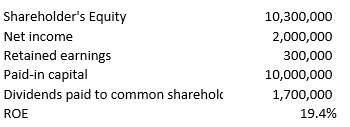

Now, consider that the company makes a profit of $2,000,000 and decides to distribute a $0.85 dividend per share and it has 2.0 million common shares outstanding. This makes for a total of $0.85 x 2,000,000 common shares = $1,700,000, which will be deducted from the retained earnings. Therefore, the retained earnings become $2,000,000 – $1,700,000 = $300,000 and the shareholder’s equity is also reduced by $1,700,000 to $10,300,000. Now, the ROE is $2,000,000 /$10,300,000 = 19.4%

You see that a reduction in the retained earnings reduces the shareholder’s equity, which translates to a smaller denominator in the ROE equation. So, you get a higher ROE as a results of higher earnings / lower shareholder’s equity combination.

The Debt Effect

One of Warren Buffett’s best quotes is “I do not like debt and do not like to invest in companies that have too much debt, particularly long-term debt.” That said, think that a firm with a high ROE is likely one that can generate cash internally. Usually, the higher a firm’s ROE compared to peer companies, the better. However, you should dig deeper into the analysis to find out how the debt level of the company.

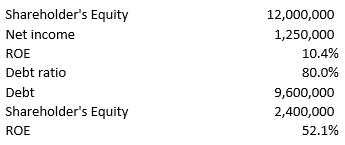

For example, in the above example assume that the firm has a debt ratio of 80%. This means that:

Debt = Equity x debt ratio = $12,000,000 x 80% = $9,600,000.

If you don’t have this information, the ROE will be 10.4% as before. If you have this information, you should deduct the debt from equity to the net shareholder’s equity in the ROE equation. Thus:

ROE = $1,250,000 / ($12,000,000 – $9,600,000) = $1,1250,000 / $2,400,000 = 52.1%.

You see that debt makes ROE higher because shareholder’s equity goes down. Yet, the ROE generated is misleading with respect to how effectively the company is being managed.

As a rule of thumb, firms create value for their shareholders if the return on equity is greater than the opportunity cost of the invested funds. That means that the expected return required by the shareholders to invest in the company should be higher than the return on alternative forms of investment with a similar level of capital risk. So, you may have a company that uses all its net income, borrows more money than it has raised by its stock offerings, buy back shares and distributes dividends, thereby creating a negative shareholder’s equity. As the shareholder’s equity portion of the calculation continues to shrink, the ROE metric gets larger.

Limitations

Generally, companies with a higher debt ratio have a better ROE. A higher ROE allows a company to invest less of its own funds to achieve its growth goals and leaves the company with more capital available to use either on share buyback or to pay an extra dividend. Also, as seen already, debt can technically increase the ROE. On the other hand, a higher debt raises a red flag for bankruptcy. So, these strategies could improve ROE, but they do not create long-term value for shareholders.

ROE is also a matter of good management. If a firm simply retains its earnings waiting for them to yield a 4% annually in a savings account, it does not create value for its shareholders. So, as a value investor, you need to look for firms whose ROE considers the retained earnings from previous years as well as the company’s debt. In that way, you will be able to know how effectively your capital is being reinvested.

Summing up, ROE can serve as a valuable metric to find interesting, prominent investments. But this is not enough. You should make sure to compare the ROE of the firm you are interested in investing to the ROE of similar companies in the industry. Become a financial analyst for a while and look into the firm’s debt and equity structure. For value investors, ROE should become a tool for long-term growth, provided that you spot on companies capable of generating a continuous, high return on equity over many decades.