I’m not lying – having a sinking fund is literally the best way that you can stay on budget. I mean, sure – you could just go make a bajillion dollars instead but that’s not exactly a feasible path forward for most of us. So, what is a sinking fund?

Before I get into the “what”, let me get into the “why”.

I have a sinking fund for protection. Sinking funds help protect me from the inevitable, largely unplanned, massive expenses that I could occur at any point in time. Those massive expenses that might completely knock you off your budget and say “screw it” for the month are going to be completely avoided because you have a sinking fund in place.

Sounds enticing, right?

A sinking fund is basically a savings account that you have set aside for a specific purpose with the intent to spend. The “intent to spend” part is extremely important because this is not money that you’re saving for your retirement that you then must pull out for some reason. You have a true plan in mind for this spending when you start to save the money.

Example of a Sinking Fund

I personally have many sinking funds, one of which being a “Presents” sinking fund. Every time that I am paid a certain dollar amount comes directly out of my paycheck and goes into this savings bucket for presents. For the purposes of this post, let’s say that it’s $50.

I get my paycheck and it’s immediately $50 less because now that money is in my Presents Sinking Fund. I do absolutely nothing with that money. Nothing at all. It just sits there and sits there until I decide that it’s time that I want to buy a present for someone.

Could be a birthday, wedding, Christmas, or a “just because” present. At that point in time, I purchase the present and will withdraw the money from my sinking fund to cover that. So, if I buy a $25 present, I’ll take out $25 to pay for it and then leave the remainder in the sinking fund.

Then, two weeks later when I get paid, another $50 goes in and now my balance is $75. Two more weeks and now it’s $125. That balance continues to grow until I make a purchase that requires me to make a withdrawal from it.

Effectively, I’m forcing myself to save for presents, which can be a major expense around holidays or if you have a lot of birthdays in your family close to one another. I’ve personally gone through many years without saving and this just helps me get ahead of the game!

I’ve had years where I haven’t been able to buy people the presents that I wanted to because of money, and it was the worst feeling ever. Since I’ve had these sinking funds in place, that’s never been an issue for me!

I also have a sinking fund setup for “Car” purchases. Now, this sinking fund is setup with two goals in mind:

- Protect us when we need car repairs

- Save for a new car

Truthfully, saving for a new car is way more fun than saving for car repairs, but car repairs are just a fact of life that is going to occur. Within the last week, I went to Midas and had over $1300 of repairs done on my car. Oil change, brakes, new tires, and a few other items as well.

I felt SICK spending $1300 on my car that I don’t even like that much. And honestly, I almost didn’t. I was trying to talk myself out of spending the money because I just didn’t want to do so.

But guess what – I told myself that my tires were beyond repair, and they were. Literally when I’d drive around a roundabout at a normal speed, and there are many roundabouts in Indianapolis, I could hear the tires squeal. And if there was rain, I could even feel the tires give out a little bit.

Not safe. And that’s only the rain!

But guess what…do you know what happens when rain gets cold…yes, it turns into snow. And do you know what else? It’s October when I write this…

I have a two-year old son and I’m freaking out about getting new tires, when I clearly need them, to help keep him safe during the winter, and I even have the money saved up to buy them.

If I didn’t have the money saved or had to dip into some other savings that wasn’t planned for that, I honestly don’t know if I would’ve made the purchase. Because I planned with a sinking fund, I was able to make the correct (and safe) decision, even if it made my heart hurt to see that money be spent on something that I get essentially no satisfaction from.

But my family is safe for it. That’s worth way more.

And if for some reason we have some sort of unexpected issue with a car, such as I’m in an accident and must pay for repairs to hit our deductible, we’re taken care of. Because we’ve been planning for the unexpected with this sinking fund, it’s stress free from a financial perspective.

Along with presents and cars, we have a “Vacation” sinking fund. Same concept as the other two but this is purely for vacations, as you’d expect. I love this because by funding a vacation fund, it not only allows us to proactively save for those big vacations that we want to have, but also for the “unexpected” vacation.

And yes, some vacations are unexpected…

Have you ever had that feeling where you’re like “I just got to get away?” Well, if you have a vacation sinking fund, you can do that. My wife and I literally did that a week ago. We really wanted to get away for a couple nights before it got cold, so we booked an Airbnb and went away for a long weekend. Stress free. Because we had been saving for its months with this sinking fund.

Now, if you want to go on a crazy vacation like a Disney trip, overseas vacation, or a cruise, you are likely going to need to save a little more in addition to your normal sinking fund, but that just depends on the dollar amount you want to save. Saving even $50/paycheck, or let’s say $1200/year isn’t going to get you to Europe for quite a while, but when you decide to start planning that trip, maybe you’ve been saving for two years and have a $2400 head start.

Doesn’t sound too bad, right?

At first, I thought keeping track of all these different sinking funds was going to be an absolute nightmare…

I was wrong!

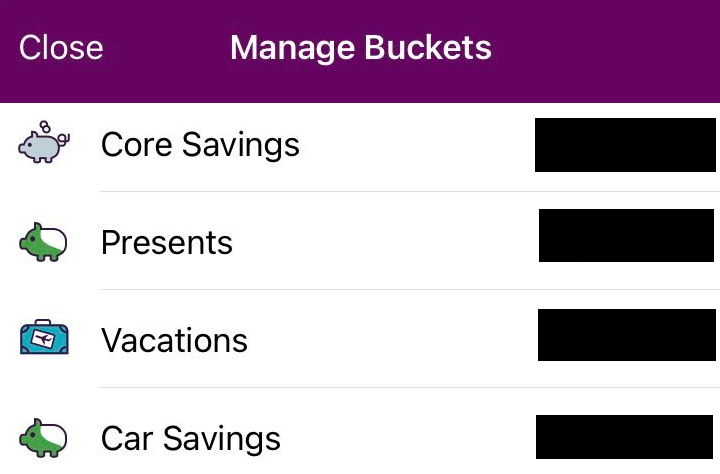

I use Ally bank as my high-yield savings account literally for this reason. They let you pick different “buckets” that you can group money into. Look:

As you can see, I currently have vacations, presents and car setup for this savings as I’ve mentioned, but you’re not limited to these buckets:

Ally is a thousand times better than a normal savings account, even with their APR being only .5%, but that destroys the .01% I have with Fifth Third, so why not at least make a little bit of money while I’m filling up these sinking funds?

One of my favorite things to do with my sinking fund is to not use it. I know that sounds counterintuitive, and don’t hear what I’m not saying. I want you to go on vacations, repair/upgrade your car, and buy presents, but one of the best feelings is to be able to do these things and just pay for it out of your normal income.

For instance, when I had $1300 in car repairs, I only transferred $1000 from my sinking fund. I looked at my budget and said, “Andy, you can find a way to save $300 this month. Only transfer $1000 out of the sinking fund.”

I really was just challenging myself to see if I could get “extra” frugal for a month and in turn, effectively save $300. You don’t have to spend your sinking fund just because you have it. I mean, at the end of the day, they’re somewhat like an emergency fund, right?

Think about it – an emergency fund is literally a sinking fund for…. wait…EMERGENCIES!

Sure, you might not be adding every paycheck, but you have saved some money with the intent to use it when crap hits the fan, right? That’s literally the point.

An emergency fund is something that’s imperative for everyone to have and if you don’t have one, start here.

Not having anything saved up for emergencies can literally ruin your finances so please make sure you have one in order, even if it’s just a thousand bucks. You need to have some sort of buffer to help you out when needed.

Ready to take the next steps on setting up your sinking funds? GOOD! Here’s what I would do:

1 – Think about the sinking funds that need setup

Could be a car, vacation and presents like me. Maybe it’s an emergency fund as well where you add X to your account each paycheck. Maybe you love to go to sporting events, so you want to save $25/paycheck now so that you have a good amount built up when that sports team’s season comes around.

It literally can be anything that you are going to spend money on that might throw you off your budget. Plan for it now so you can spend worry-free in the future.

2 – Determine the amounts that you need

If you want to go to two NFL games each year and you know they cost you $200/each, then you need $400. So, maybe aim to save $50/month from now until then so you have $600 saved for that season’s games. Then you have a nice $200 buffer in case your friends want to go to another game or maybe your team makes the playoffs, and you want to see them play.

Sure, a playoff game would likely cost more, say $300 instead of $200, but now you only need to come up with $100 because you saved an extra $200 to begin with.

Same with your presents, car, or anything else. Think about what’s likely on the horizon for you. Christmas is coming up – how much do you normally spend? How are the tires on your car doing? If they’re bad, maybe inch up your savings number a bit faster…. you can always ratchet it down later.

For instance, if you need new tires in 3 months, why not try to save $200/month to cover those? Then once you buy them, go down to $50/month to fill up that sinking fund. It doesn’t have to be a “forever” amount…

3 – Set your money up to auto-transfer

This is so huge because if you don’t do this, you likely won’t save the money. You’ll find a reason not to save it and instead just blow it and then come Christmas, or the time you need the new tires, or your team’s playoff game, you’re SOL. You don’t have any money so you can either spend anyways and ruin the budget/go in debt, or just miss out on the thing you want/need.

Both options are crappy, huh?

Instead, setup either an auto transfer from your account each month or work with your employer payroll to have it automatically come out of your paycheck like I do. I like this the most so that every time I get paid, I have a lump sum go into my Ally account and then I divvy it up between presents, vacations, and car, just as I’ve explained previously.

Honestly, it’s a pretty fool-proof system to implement and one that will help you out a ton in the future.

At the end of the day, a sinking fund is nothing more than a dedicated savings account for a specific purchase, but the lack of one is literally a budget killer – I can speak from experience.

Determine what sinking funds you want, pick the amount, auto transfer that money, and plan it all out with your budget calendar, and bada boom bada bing – you just became a budget savant!