Podcast: Play in new window | Download

Subscribe: Apple Podcasts | RSS

.

The efficient market hypothesis is one of the hottest debated topics in the investing world. In today’s session, we are going to discuss some of the many ways this theory is flawed. We will talk about many of the efficient market hypothesis assumptions and how they may or many not have gotten it wrong. Pricing is one of the main hot buttons in this theory and we will show why the efficient market hypothesis assumptions are incorrect.

- The efficient market hypothesis states the market can’t be beat

- All stock prices have all relevant information included in them

- Only way to beat the market is with passive investing

- Warren Buffet debunks this with his famous speech

- Value investing has beaten the market over the last thirty years

- The efficient market hypothesis is based on people being rational, which we all know we are not.

- The market can be beaten and there are lots of tools to help.

- If you don’t want to be an individual investor than index funds are the way to go.

Andrew: Well, two weeks ago we took out our weapons and fired them into the financial services industry and probably pissed off a few people.

Today we are going direct it against some other group. Probably make some people mad. Basically talking about the academic types in their ivory tower. There is a theory called the efficient market hypothesis, really based off a lot of the professors at the University of Chicago.

If you pursue an education in relation to investing or the stock market, economics you will get exposed to the efficient market hypothesis.

It is something that there has been a lot of studies on. Ph.D. thesis was done on it. It is also a very hotly debated theory among investors, particularly value investors.

You have the value investor side. Guys who have made billions like Warren Buffett, Seth Klarman, Peter Lynch, Joel Greenblatt, Monish Pabrai, and on, and on.

It’s kind of like them through their performance that has proved the efficient market hypothesis hasn’t held true for them. So, there’s that camp. And there’s the other camp that says the other investors should not try to beat the market because the markets are efficient.

So that’s something we kind of want to address and give our own takes on it to see.

Our audience is a lot of beginners and if there are academic studies saying we shouldn’t try to beat the market. Or is it something we should try to follow, or is it something we should look further into and see if there is a way to mitigate that.

That’s what I hope to do with this episode.

Dave: Why don’t you tell us a little bit about the efficient market hypothesis. Where it originated and who started it, and what your thoughts are on it.

Andrew: It’s been around for a while. Most recently is has been popularized by Jack Bogle and author Burton Malkiel, who wrote a Random Walk Down Wall Street. Where he brought his own inputs into it and gave some conclusions about why the markets are really efficient.

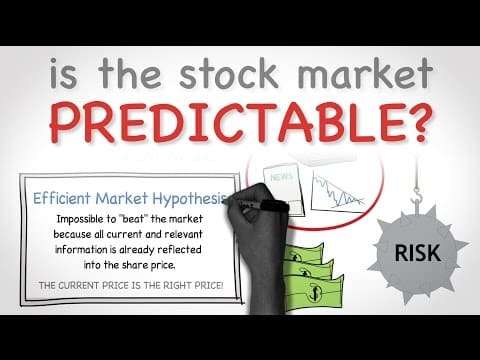

So the whole premise behind it is that there is this idea that every stock available in the stock market is fairly priced based on the information that is available currently.

There is all this financial data, these stocks trade on how they release earnings, what balance sheets look like. So, the whole premise of the efficient market hypothesis is that all this information is freely available. You’ve got millions, perhaps billions who are sifting through this.

Industry professionals, fund managers, individual investors like you and I are all dissecting this data as it comes out and investors react. For examples, you have this earnings report that comes out and it will likely push the stock price up.

But the efficient market hypothesis states that all the stocks are priced fairly. They are priced based on information that is available. So there is no way to get an advantage if the company is pricing what they are releasing what is in their reports.

Dave: The studies that I have read about the efficient market hypothesis says that it basically means that the prices you see on a stock, whatever they may be. All the current factors are factored into that price for that day. So there is no discrepancy between the value of the business. And, therefore you can’t beat the market.

There is no way to beat the price of the market. I know the gentleman you mentioned earlier, Jack Bogle and Burton Malkiel. They are very smart men, learned men. They have written some very good books. And they make some great points in their books. I know that Andrew recently wrote a piece about Burton Malkiel in which you discuss your thoughts on his ideas. I agreed with a lot of the things you were saying in your article.

One of the things I wanted to mention about both of the gentlemen is that some of what they say I have to kind of take with a grain of salt. I am skeptical because they are advocating passive investing. This is one of the things that the efficient market hypothesis advocates.

Passive investing.

Because you can’t beat the market you invest in ETFs or index funds which are passive. Have lower fees and theoretically you are matching the market and that is how you can win, in essence.

Both Bogle and Malkiel have a very big stake in companies that offer ETFs and index funds. Jack Bogle is president and CEO of Vanguard. Which is the largest fund provider in the world. So he has a very large stake in what he is advocating. I am not saying that a lot of the things that he is saying are wrong. But I am saying that I think the efficient market hypothesis is frankly, kind of bunk. And I will say it out loud.

When you talk about guys like Warren Buffett, Monish Pabrai, Seth Klarman, Joel Greenblatt, Bill Ackman. There are all these great value investors that have actually figured out a way to actually beat the market.

I am going to chat just a moment about something that Warren Buffett did. He gave a speech at Columbia School for Business commemorating the 50th anniversary of the release of the great book, Security Analysis. The awesome book by Benjamin Graham that we have discussed many times on this podcast.

This speech was so popular that later he recreated on paper so that it could be remembered. It is called the Superinvestors of Graham and Doddsville.

If you have not read it then I urge you to run out and read it. An amazing article that has lots of great “Buffettisms” in it.

One of the things that he talks a lot about in the speech is he illustrates the performance of eight different super investors. These are all value investors that he has either worked with or knows personally that have beaten the market by an average of 18% to 20% over a 30 year period.

One of the things that he talks about in this article is a coin flip. He talks about the statistics of that and if you take every single person in the US and do a coin flip. Eventually, you are going to get down to very few winners.

He argues that you can take this same this same test and do it with orangutans and get roughly the same result. His point in this whole coin flip is that if you find 40 orangutans that are doing much better than the other orangutans. And these 40 are coming from a zoo in Omaha then you are going to be curious. Why are these orangutans doing so great?

What is their secret? You are going to start analyzing this to try to figure out they are beating the rest of the orangutans flipping coins.

He calls this an intellectual exercise and this is where he comes up with this Graham and Doddsville because he is taking all the gentleman who has been influenced by the works of Benjamin Graham and David Dodd. And lumping them all into a little town that he calls Graham and Doddsville.

Through his explanation of how these gentlemen with all different styles of investing. They are all value investing by a generality but they all have different ways of coming at it. They have all been able to beat the market by finding differences in the value of the companies.

Notice I am not saying the price. They find the differences in the values and the prices are related to that. And because they can find differences in the values they can find great deals on companies which allows them to make millions and billions of dollars.

To me, when you look at that it is not just luck. And I think that is what some of the guys in the academic world would look at Warren Buffett and say it was all luck. They would say he is just one person or just a few people.

There are way more than two people.

I am not a learned investor. I am self-taught and I know Andrew is as well. And both of our performances in our portfolios have beaten the market. By fair amounts and that shouldn’t be possible with our style of investing.

This to me, helps me think that the efficient market hypothesis is wrong.

Andrew: The coin flip thing is something that is really the main points of the Random Walk Down Wall Street that Malkiel wrote.

Like you said I really respect Malkiel and Bogle’s work and we do have a lot in common. For example, if someone does not have the inclination or the desire to commit the time or to learning what the stock market strategies are. Why the numbers work as they work. They I definitely agree that someone should be a passive investor. Buy index funds and they will do great. They will have a much, much higher performance than if they were to try to beat the market with limited information. And no sort of base foundation understanding of what is going to give you that advantage.

When you talk about this advantage and this whole randomness of coin flips it is a really interesting thing to think about. Because like you mentioned, Buffett said that we have these coin flippers, is it a coincidence that they all come from the Columbia School of Business. All were mentored by Benjamin Graham. And all have aspects of philosophies of Benjamin Graham in their investing styles. Is that really a coincidence?

To take that point a step further. Another kind of ideas that could beat the market, surely other fund managers would be able to beat the market? Right.

So we have all these reports and studies. And you can’t refute these studies, these are just facts. And obviously, it depends on which time period you look at. When you look at performance is always something to keep in mind. The longer you can look the better. You mentioned earlier three decades of outperformance. I think that is a much better time to look at, even better than a 10-year performance.

But the studies show that the majority of the fund managers don’t beat the market. Even a higher number aren’t able to beat the market and give the investor that invests his money an even higher return than the market. Especially when you take out management fees, trading fees, and all the other fees that are associated with active mutual funds.

I know the numbers, it depends on which study you look at. And which time period you are looking at. Sometimes they will look at a specific year and show how many people did not outperform the market.

But somewhere, you could say as high as 70%, even a 90% rate when you are including fees. Which means that there is only a 10 to 20% chance you can beat the market. So why even feel like you could even do it.

I will present a different idea. Let’s say you look at a very popular investing resource like CNBC. That is probably the most widely accessed investing resource out there

So, if you look at their online TV viewership it is. From a TV aspect, there are 12 to 20 million viewers a day. Every single month.

Not every person who watches is going to be an investor. You have to imagine that most people are going to use CNBC as some sort of aspect of their investing resource. So CNBC is going to have an influence on their investing.

If you ever turn on CNBC, I love to watch it. And my favorite show on there is Shark Tank. I think that Shark Tank shows you more about investing than any other show they have. And the sharks on there, Mark Cuban, Mr. Wonderful they are all doing valuations in 5 to 10 seconds.

They will buy a business with a price to sales of 1.5. I was watching an episode just the other day where the person trying to get investment funds for their company was trying to value their company at $6 million, which would have been a 4 to 5 price to sales.

Interestingly enough, I think it was Cuban and another investor who went in on the deal together but they valued the business based on what kind of equity stake they would get. Which ended up being 1.5 price to sales.

Is that a coincidence that this a similar type of ratios that we like to use as value investors. There are guys like James O’Shaughnessy that have proven through different kinds of studies that there are these kinds of ratios that have outperformed.

I am getting on a tangent like I always do, I am going to circle back. Don’t worry.

If you CNBC and you have 20 million people watching it a month. Compare that to the Intelligent Investor. By the way, if you have not read Intelligent Investor and you call yourself a value investor. You do not count. If you have not read it, shame on you.

So when Warren Buffett had a speech about the super investors of Graham and Doddsville school. All of those investors have outperformed. Like we said they were influenced by Graham. They had no doubt read a book like the Intelligent Investor and Security Analysis, really the core principles of value investing.

If you look at sales of the Intelligent Investor, you know it is financially incentivized for the publishers to broadcast the numbers of copies sold. To release how many copies have sold. Right now it has sold around 1 million copies since it’s release, in the 1950s. If that number reaches two million you would think they would publicize that.

If you compare all those fifty years only a million people have read that book. Compare that to CNBC where a lot of the monthly viewers are probably counted from month to month. Over a fifty year period, I am sure there is a lot of churn there too. And I am sure you have a lot more than 20 million people that use CNBC as part of their investing resources. So just from looking at that alone, you are looking at a less than one percent, maybe less than .5 percent if you are lucky. Percentages of people that are implementing this value investing strategy.

To look at the numbers and look at what Malkiel’s already talking about with the fund managers already have a low percentage of them outperforming the market. How can you as an individual think that you can do it.

If I know that my strategy is only used by less than a half a percent of the investors out there right now. And I know there is a 25 percent chance I will beat the market. I think the coin flip favors me if I know that there is research behind why it works. If it makes logical sense and I am seeing the results myself.

Then all of sudden being one of the 25 percent who beat the market doesn’t seem so strange when over 99 percent aren’t even considering value investing in their strategy.

Dave: That is a good way of looking at it. I think part of why they may not be looking at the value investing strategy is because it is hard. Not hard in that sense of difficult, but it takes effort.

You have to do research, you have to read about companies, and there is some math involved in value investing.

And I think that may turn some people off from the strategy. I think another aspect is that is has a long-term horizon. Generally, I think that value investors are looking a long ways down the road. Where I think more investors are looking for the get rich quick scheme.

An example would be everyone buying into Snapchat (SNAP) recently.

I was reading earlier about the investing app Robin Hood, that allows you to invest from your phone. They stated a little bit ago that almost 80% of their users bought into the IPO of Snapchat. And being that most of them are millennials was very interesting. They don’t have the exact numbers or maybe won’t release the exact numbers but that shows the power of marketing and the ease of their platform that allows investors to buy into those companies.

It shows that people were excited for the IPO and the ability to buy into a company that they use and are excited about.

But, like we mentioned last week there are no numbers to go off of. It has been losing money since it’s inception and it is not profitable yet. So you are basing your buying decision on emotions, not facts or numbers. To me, this is an example of how the market is inefficient.

When you speak of pricing as it relates to the efficient market hypothesis there is this concept that the current price contains all relevant data know at that moment.

For example, if you buy Apple (AAPL) today then the price will convey all the known information and if you buy it tomorrow it reflects all known information at that time.

But there are so many things that happen in the market that you just can’t explain simply by saying that the price already has everything factored into it.

How can explain the crash in 1989 where the market lost 20% in one day? What does that have to do with efficient? That is people freaking out and not wanting to lose all of their money.

An aspect of the efficient market hypothesis that I haven’t mentioned yet is that it is based on everyone behaving rationally. Which means that no one is going to have fear or greed. And as we all know we are human and we have both of these emotions, sometimes in plenty.

When things go badly we freak out and when things are going well we get greedy and want more. When things like that happen we are reacting to emotion and the efficient market hypothesis doesn’t factor that in. It is saying that the current price of Apple is based on rationality. And when a earnings report is scheduled to come out you will have people that will short the stock believing that it will fall in price because of a bad earnings report. And they believe that people will want to get out of Apple because of a fear of losing money, so that reaction is based on fear. Not rationality.

Or the flip side is the earnings report is really good so now everyone will want to buy Apple which will drive the price up. Again this based on our emotions, such as greed or the fear of missing out.

These are just some of the reasons why I am skeptical about the validity of the hypothesis. Of course, these are just my opinions and I am by no means the smartest person in the room. But I am smart enough to see the patterns and the performance of value investing. When I see the research and investigating that goes on to buy a company and find a deal on something to buy.

Intrinsic value is not just in the stock market. It is a day to day life as well. When we are looking at buying a house or a car we are all looking for a deal. We find something that we value and we put a price on that. Once we have that we will look for a price below what we feel is the value of that item.

When we find a house we think is valued or $150,000 and we can buy it for $120,000. We think that is a steal and are super excited about that. The Same rule applies to the stock market.

If you see that a company you like is selling for less than what you think it is worth, then you think you have made a good deal.

All of these things lead me to the conclusion that this hypothesis is not valid.

Andrew: That leads to another good point about why prices out there reflect what the company is really worth. We have talked about the different philosophies and what you see on CNBC is a lot different than what Benjamin Graham teaches.

In the same token, whoever is going to watch CNBC is going have segments for people that watch charts, people that watch earnings.

Even within individuals, it is very rare to find two individuals that are using the same strategy and doing the same thing. When you take that on a broader scale and you look at the entire market. Everybody is bringing their own unique take into it. It is this idea that we are all human beings and sure there is some of this high-frequency trading or algo that people trade on in these sophisticated platforms. Like Goldman Sachs platforms that have all these alogrhytms that do it for them.

That is not even remotely close to what the majority of the market is comprised of today. So we have human beings, and before you can argue that we are all rational and that we have evolved past the caveman status. I just want to challenge that. Think about the last time you felt your blood pressure rise and you got that tingling sensation in your skin. Or maybe you felt really uncomfortable because you were thinking of what some random stranger was thinking about you. Maybe you do something embarrassing in public. Or the fear of public speaking.

These are not rational fears. We go into flight and fight response when we are confronted with something that makes us upset. It is just something that is ingrained in us. A part of our DNA.

As long as you are having these kinds of shared reactions then I am here to tell you that we are not all completely rational. And number two, if you run into people during your day that are not completely rational than it is safe to assume that the market will react the same way.

So, we have Maybeall these people and they are emotional and now we are talking about how they are bringing their own unique filter into the market. They are all looking at the same amount of data and coming to different conclusions.

For example, say you have a company that grew earnings by ten percent. Because we are looking through our tinted glasses. We are all going to perceive what that stock is worth in a different way. And so this idea what price really is based on what the price is really worth today. I think is fundamentally flawed and too broad of a generalization to really be accurate. To think that such a broad group of people would all value a company the same way. You have analysts, people who are in the industry who spend their nine to five plus looking at companies. They are all looking at how the company is going to do in the next quarter, what are the Christmas sales going to be like and how it will affect Apple’s third line of products.

And on the other side of things, you have people that are really far removed from that. People like myself who are value investors who look at things from a broader sense. We see a company with this certain amount of earnings, a certain amount of debt, and so this ten percent earnings growth really means this to a value investor. And other groups are going to value the company differently.

Because we are not all on a level playing field you can’t confidently say that we are all going to perceive information as being different. Our dollar votes and you see that reflected in the stock price. But that could be based on factors that don’t even have to do with the value of the stock.

Or how we perceive it. How many people have pulled money out of the market because they have an emergency? How many people have taken money out because they are having a financial emergency? Or what about the insider trading or the company employee who is terminated and needs to liquidate their stock options to live on.

So many different factors and so many different people all going through this thing we call life, all at the same time. All with different situations, and you compound that with we are all having our different principles, our own different feelings, and biases, and strategies on the stock market. And I don’t think it’s fair to say just because information is so freely accessible that how information is released will affect the stock price in the market all the same way.

You could have a stock like Apple that grows earnings by ten percent. And you could have a smaller company that is not covered by nearly enough sell-side and buy-side analysts just because the money is not there.

They could also grow ten percent and there could be more value in one or the other. You will see a much greater effect on the stock price as that goes along. There are so many myriads of reasons why the price could fluctuate.

To say that the price of a stock is equal to the value at any given time is not a good conclusion at all. I think it is wrong.

Dave: Price is based on what someone is willing to pay for it.

You and I can look at Walmart and Amazon who are competitors, to a certain degree, especially in the online arena. You can look at Amazon and say awesome company but there is no way I can buy it because it is just way to expensive for me.

Where Walmart is much more in my price point and I would be willing to buy. But I would have to look into why I would be willing to buy it. Another example would be a car. You and I could look at the same car and I really want it. Whereas you like but are willing to wait for the right price. But I want it so badly that I will pay any price for it. This ties right back into the emotional part of investing and how the price will dictate my feelings towards buying that company.

The whole issue with price is that it is just an illusion, to think that everything is factored into a price and that is the fair value at that, time is bogus. Price is a function of the desire of someone to pay it to own that piece of stock, or car, or iPad, and so on.

There are so many factors that go into pricing any item. To take two people that think alike, like two value investors and think that they will have exactly the same thoughts about an investment is flawed. We all have different biases that we bring to any decision. And those biases help shape our thoughts and actions.

This all comes back to help debunk the hypothesis because when you lump all the people in the stock market that make buying or selling decisions with their different biases and thoughts. You are going to get a different reaction from each individual investor on their thoughts of the current price of Amazon vs Walmart.

There is nothing rational about any of that. When someone buys Amazon because they buy all their clothes, shoes, groceries from Amazon. They think it is a great company and buy based on their emotions as opposed to looking at any numbers. Again this shows that individuals are not going to be rational when they decide to buy a company.

Others may look at these companies and decide not to buy because the earnings are down, sales are down, not growing enough, and so on. They may be making a more rational decision based on factors within the business. But everyone will have their different take on this single business.

Andrew and I are looking at investing on our own. We enjoy doing the work, figuring out the numbers, reading the financial documents, and studying related market data. This makes us a little bit different but we want to do this on our own because we feel that there is a discrepancy between value and price of some companies.

If someone doesn’t want to do all that work and want to invest because they think they should. Then by all means dollar cost average using a diversified approach to ETFs or index funds. You will do great and you will be happy later in life that you did.

However, if you want to do the work and are willing to put the time in you can beat the market. It is not a guarantee and it won’t always be easy but it can be done. There are studies that show it to be true and you can see it in the performance of many different value investors.

There are some great tools out there that can help you do this, with frankly not a ton of work. Tools like Andrew’s Value Trap Indicator. It can help you beat the market and in a safe way. This is a system that Andrew is using himself with his life savings and he has been able to beat the market for the last three years.

Beating the market can be done and there are a million ways to do it. We use value investing as a means to outperform the market.

Andrew: I have one more bullet left in the chamber. Malkiel has done some more research that I haven’t discussed yet. He analyzed some charts and came to the conclusion that a stock has the chance of going up or down by 50%. So he debunks the whole idea of technical traders and momentum trading. Saying that studies have shown that momentum trading doesn’t work because there is no correlation between what a stock will do today, versus what a stock will do tomorrow.

Based on the research that I looked at there is a slight tilt upwards based on having the stock be up in price for a day as opposed to down.

I looked at the S&P 500, or the whole market. And slightly bigger chance the price will go up. And if it goes down it is more likely to go down faster.

We see that with big drawdowns and market crashes in the same period of time. And then, in general, you see the market tick up.

Malkiel takes a chart of coin flips again and if you chart coin flips you will see it randomly goes up and down. Which really mirrors what a stock chart looks like.

So it is good exercise and a great visual, but again I have to look at another fact that I feel is a little overlooked.

If you look at the market and it has grown a little over 10% for almost a century. No coin flip is going to replicate that over that long of a time period. I don’t care how many simulations you do with coins. There is just no way that is random. And the reason is because the market and economy expands and contracts in general. The good businesses rise to the top and inflation growth, a lot of businesses grow over time.

Because we know there are businesses behind these stocks and the market is slowly increasing over 10 percent a year over a long time period. You can’t use a coin flip metaphor to say that all stock prices are random.

It is a nice idea and it’s a great way to scare people into indexing but it is not really what reality is.

As value investors, we are not only trying to take advantage of that but we also see that there are businesses behind these stocks. And if we can get our portfolio with some of the high performing ones, then we could get that 10 percent. And maybe get it even higher.

We have explored coin flips from both sides and while it is a great exercise. You just can’t ignore the outliers that are concentrated in Omaha. That are all being mentored by this one guy. Do not discount those outliers and think that as an average investor that you cannot beat the market. Or that you cannot beat the fund managers.

We talked about financial incentives of the fund manager in episode six. And how that skews their returns. So don’t be discourage and find the right principles, find the right paradigm, and shift your mindset. And then if you can be intelligent enough to apply yourself to comprehend what is going on. Then I think you have a good chance.

That concludes this session today. As always thanks for listening/reading and if you have any questions you would like to discuss with us please drop us a line to let us know.

We are here to help and encourage you to reach out. No question is too small and any little way we can help bring some light to your world, we will do so.