Updated 10/12/2023

The implications for a negative PEG ratio might not be as bad as you think. It all depends on the reason behind the negative PEG ratio, which breaks into 2 possibilities.

One spells trouble while the other might not.

In this post, we will discuss:

- The Simple PEG Ratio Formula

- Why Can the PEG Ratio Be Negative?

- Is a Negative PEG Ratio Good or Bad?

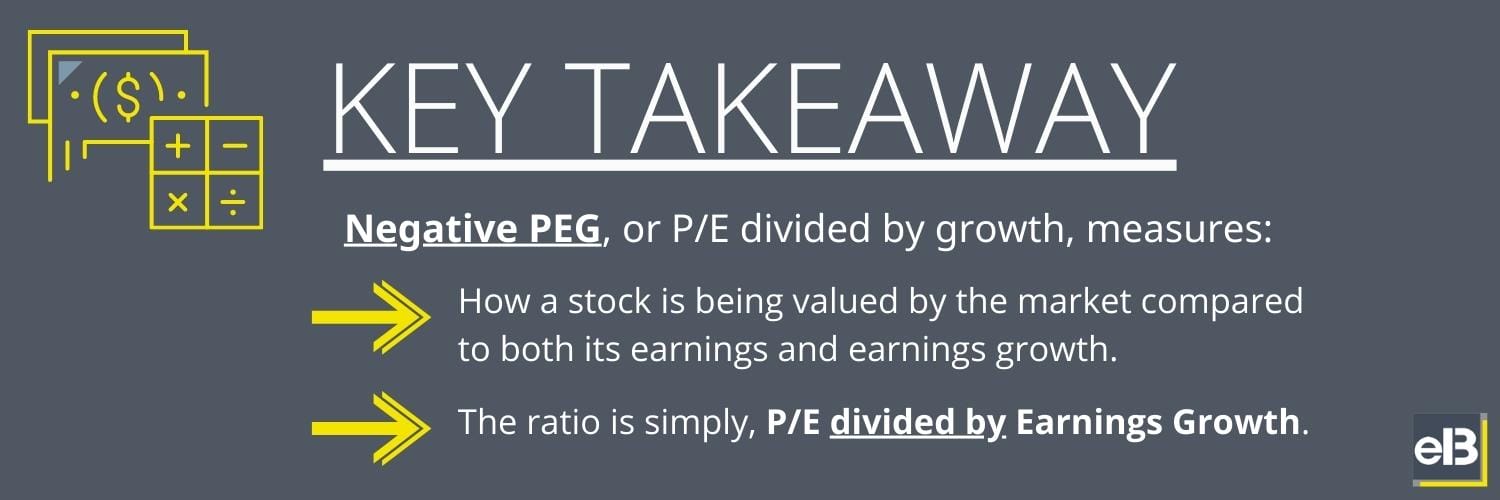

Before digging into the PEG scenarios, we first must know how to calculate PEG ratio, or the “Price divided by Earnings divided by Growth” ratio.

The Simple PEG Ratio Formula

It’s simply division; divide the P/E ratio by the earnings growth.

Now, in most general stock market websites, they use yearly earnings growth to calculate PEG. However, some may use Q/Q (or Quarter over Quarter) growth instead, so it’s important to check the numbers for yourself before trusting any website’s ratio.

PEG = (P/E ratio) / (Growth in Earnings)

If you don’t know how to calculate growth in earnings (or “net income”), you can use the following easy formula for calculating growth:

Growth in Earnings = [(This year’s earnings) / (Last year’s earnings)] – 1

The formula returns a decimal number, which you can multiply by 100 in order to get a growth percentage (%).

The PEG ratio works like the P/E ratio, in the sense that a lower value is generally more desired. Whereas a P/E ratio is showing how much you are paying in relation to earnings, the PEG ratio expresses how much you are paying in relation to the growth.

You can think of a PEG less than 1 as meaning that you are getting more growth than you are paying for, and a PEG greater than 1 as getting less growth than what you are paying for.

This assumption is loosely accurate and widely based on Peter Lynch’s growth strategy, where he wants a growth rate at least higher than the P/E ratio. A stock priced at 17 times earnings is expected to grow 17% next year, which is how this idea is derived.

Of course, the way that things play out in the real world and how conventional wisdom tells you they should play out are rarely the same. But still, this is a mostly accurate calculation that I can endorse the general concept of.

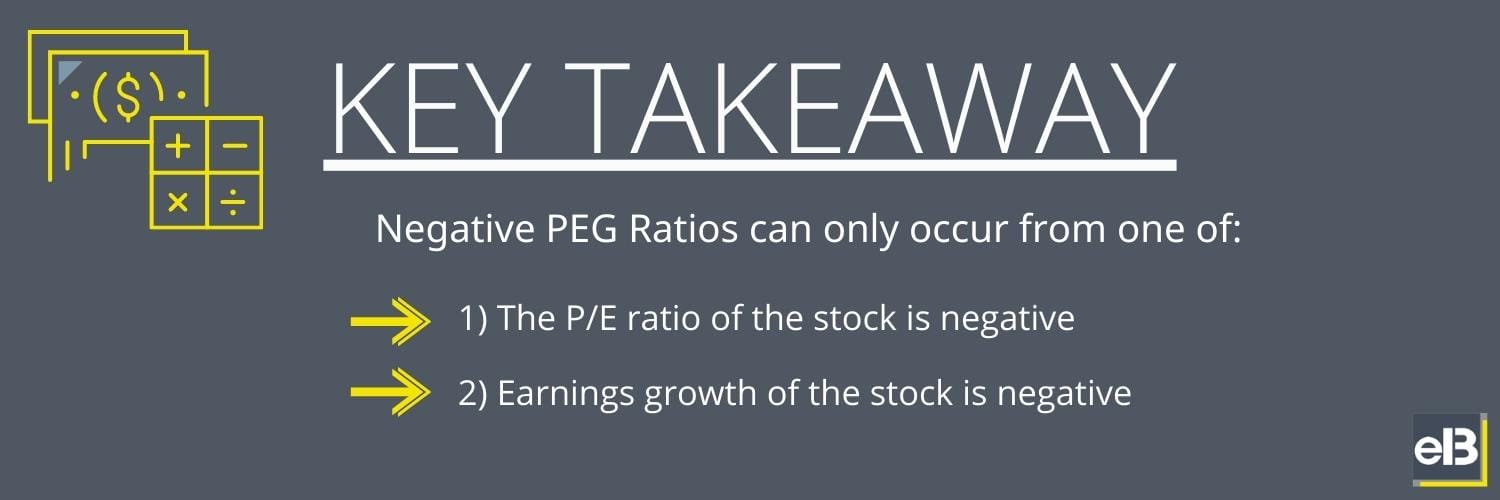

Why Can the PEG Ratio Be Negative?

Looking back at the formula for PEG, we see there are only 2 possibilities.

- P/E ratio is negative

- Growth is negative

1– If the PEG ratio is negative because of a negative P/E ratio, the same logic applies as I shared earlier.

This is a situation to avoid if at all possible, because negative earnings are an extremely risky place for a business to be in. The possible gains that could be made by gambling on a comeback story usually aren’t enough to justify the enormous risk you take by investing in this kind of situation.

2– The 2nd situation isn’t as black and white. If a company’s growth is negative, it could be something you want to avoid.

But, companies lose growth every once in a while, especially temporarily. Even the greatest stocks that have compounded early investor money many times over have fell subject to negative growth from time to time.

I mean, just look at the way the economy functions.

During a depression or recession, businesses just naturally compress even if they are strong leaders of their industry. The impact of economic hardship frequently affects the whole stock market in a butterfly type effect, and so the health of earnings naturally deteriorate during those times.

It’s the scale at which earnings deteriorate that prudent investors need to monitor. If a company gets hit so hard that earnings go negative for the year, thus creating a negative P/E ratio, then again this should be absolutely avoided for most investors.

Is a Negative PEG Ratio Good or Bad?

It depends.

If the 3-year average growth is still strong, or if the company’s valuations and balance sheet are so attractive that short-term under-performance can be tolerated, then I’ll consider still buying the stock. I’ll admit, it takes practice to make the distinction I’m referring to, so beginners might want to beware.

But to think that a negative PEG ratio should automatically disqualify a stock is nonsense.

One last thing you should consider is that a company with negative earnings will have wacky PEG calculations. Not only will the numerator be negative with a negative P/E ratio, but the growth will be impossible to calculate. Try to calculate growth with one year in the negative or even two years.

It’s impossible because the growth isn’t real, and it’s for this reason that you should not bother with calculating the PEG ratio if a company has negative earnings.

The negative sign throws off the calculations and either overstates or understates what growth would’ve been. Plus, a company that’s losing money and then “grows” to lose less money is still losing money. Unless it’s a company growing very quickly, it should probably be avoided like the plague.

Andrew Sather

Andrew has always believed that average investors have so much potential to build wealth, through the power of patience, a long-term mindset, and compound interest.