At times you need to treat yourself, but always make sure to calculate how much you can spend on a car before you go crazy!

Are you tired of driving that old beater car around? Do you finally have some extra money and it’s time to make your first real “big kid” purchase? Or are you tired of putting service dollars into your car and you can no longer afford it? No matter the reason, when it’s time to buy a new car, the first thing you need to figure out is how much you can spend on a car.

Automobiles are an interesting topic. It’s an item that can certainly be called a necessity, but there is a huge variance in what you can spend and what you get back. I can make the argument that a brand-new car in the $30,000 range provides just as much value as a $50,000 car with leather seats, a sunroof, and shiny rims.

And as with anything in life, there is a huge variance between what you can technically afford, and how much you should spend. For example, I can afford an $80,000 truck with a six-year payment plan and maybe cut a few things out of the budget. But does it make more sense to buy a $50,000 truck with a five-year payment plan and live the same life I do today?

There are multiple factors to think about, and at the end of the day, how much you can afford to spend on a car is going to come down to your financial value. How much do you want to put in savings each month, and what other areas are you willing to make cuts for to have a more expensive vehicle?

What do the Experts Say?

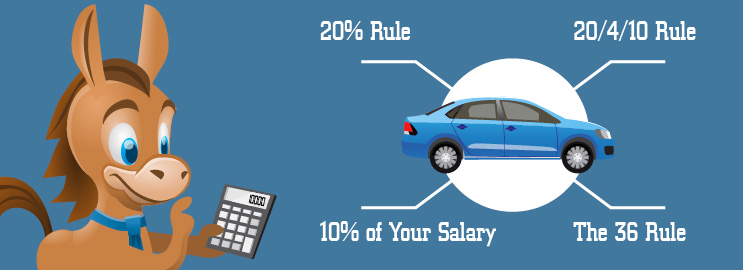

When it comes to finances or budgeting, you can typically find a rule for any type of situation imaginable. Figuring out how much you can spend on a car is no different. The financial experts have a fairly simple rule of thumb on this; you should spend no more than 10 percent of your take-home pay on a payment, and no more than 20 percent on total car expenses in a month.

In the example above, if you bring home $4,000 a month, you should have a car payment of $400 a month, with up to $800 a month in total car expenses. It can be a bit of a liberal decision if you want to make an assumption about a new car having fewer maintenance costs (meaning more can go to the actual payment), but it’s not a bad rule of thumb to follow.

Keep in mind that the 20 percent rule does include all car expenses for the month. That means with fuel costs up 20-30 percent across the board, it’s that much less that you should technically be spending. The less driving you do, the less maintenance and gas you’ll need, meaning you may be able to increase that budget on a new car.

Two other items that you must consider when figuring out how much to spend on a car are your current budget and considering what you are paying for mortgage/rent. Remember, you’re supposed to only spend 30% of your take-home pay on your rent/mortgage each month.

So if you are already maxing that out, you may want to consider scaling back on a car payment. If you have 50% of your take-home pay tied up in a car payment and rent, you could really struggle to pay the remainder of the bills.

Another item you are all tired of hearing me preach about is the monthly budget. For me, this is what I would use for my bible when figuring out how much to spend on a car payment. The good news: if you have a tight budget and plenty of money coming in, it may say you can spend way more than 20 percent of your monthly income on a car. But on the flip side, if you are spending more than you are making already, it may say you can only afford five percent of your income towards a new vehicle.

The only advice I will give you: be honest with the budget. Don’t underestimate costs just so it looks like you can afford a bigger payment. There is no worse feeling in the world than buyer’s remorse after spending a lot of money on a car and then realizing the payment is a stretch.

Also, don’t rob Peter just to pay Paul. What I mean by that is you can always adjust your budget to free up some cash flow. Don’t decrease what you put in your savings each month, don’t stop putting money away for your kid’s college accounts, and don’t stop doing fun things just to afford a car. As a guy that has had far too many cars in my short time, trust me, less is more with a vehicle.

Items to Keep in Mind

Unfortunately, when calculating how much to spend on a car payment, it’s not just a car price you have to think about. As with anything when it comes to finances, there are about a million different variables to consider, but I want to cover a few big ones today to think about before making a big purchase on a new vehicle.

The Interest Rate

With inflation levels and car shortages through the roof right now, interest rates have really spiked, which can make a huge impact on a payment. Just a year ago, you could get an interest rate near zero percent on a newer vehicle and a five-year loan. Now, even with a good credit score, you are talking about a 3-4 percent interest rate on a five-year loan (or 60 months).

Using the example above, a $25,000 loan (assuming no taxes or down payment to keep it simple), the five-year loan payment would be $416.67 per month with a zero percent rate. If you take that rate up to four percent, your new payment becomes $460.41, an increase of $43.74 per month. That is nearly $525 per year, and more than $2,600 extra over the course of the loan just in interest! If you think this is nasty on a car, you should see what a percent does on a $300,000 house if you are looking at moving.

I’m not saying you shouldn’t buy a car if you need one or even want one, but with interest rates higher than they have been in over a decade, it is something you should consider when calculating how much you can truly afford on a monthly payment. If your budget is already tight, waiting six to twelve months could gain you an extra $40-50 per month to spend which can be big in a car payment.

The Loan Term

While an interest rate can certainly affect the payment in a negative way, the loan term is a way that can affect your payment either positively or negatively, depending on your choice. If you lengthen the payment term you will decrease your payment, and if you shorten the term it will increase your payment.

Remember, the shorter the term, the better interest rate you will typically get. Also, you must be careful with depreciation when it comes to a vehicle. It’s very easy to get upside down in an auto loan so you must be careful to avoid that.

What do I mean by upside down? That is when the car is worth less than you owe. If you don’t put a lot of money down and extend payments over 72 or even 84 months, you will quickly find yourself in that situation. While it’s not the end of the world, it will put you in a situation where you can’t get out of the car if you ever needed to.

I, personally, would always recommend a 48-month loan (or four years). This will likely make your payment a little higher than you expected in your head but will help with interest rates and not getting upside down. Additionally, it will also help you pay off your vehicle quicker, which is the ultimate goal.

A 60-month loan would be what I consider the industry “standard,” but I could never recommend an auto loan longer than that. You’ll hear on the radio constantly that you can get a $300/month payment on a brand-new car, but it’s six percent interest and an 84-month term.

If there is a car you absolutely love and need to extend the term to afford it, I’m not here to ruin your day. But you do need to do the math and make sure that it still fits in your budget. When I got married and bought a new car, I went with the 60-month payment just so I could afford my first “big kid” car. I ended up paying extra to make sure I didn’t get upside down, but I was bound and determined to get that car.

The term can be your friend or your enemy. Remember, it will be easy to just extend it to bring your payment down, but you should always push to have the shortest term possible while still affording the payment.

The Down Payment

The last piece I want to talk about to keep in mind when figuring out how much to spend on a car payment is the down payment. We have talked about interest rates and loan terms which can affect the payment, but the down payment is huge as well.

I would say 20 percent down is likely a bit aggressive, but a great target to shoot for when buying a car. Not only will a big down payment help you buy down the payment, it will also assure you that you won’t get upside down even if the loan term is slightly longer.

Unlike a house, getting equity in a car is difficult. Every time you upgrade, you are usually making a pretty big leap, so it eats into your money very quickly. As I mentioned above, the situation you want to avoid at all costs is going to look at new cars and realizing you’ll owe money on your current car after the trade-in.

If you want the big fancy car, my suggestion would be to start saving and come up with a huge down payment to make sure you can afford it. Even if it takes you a couple of years to save up, having a car payment that fits into your monthly budget is a huge stress relief.

Other Considerations when Buying a Car

The main purpose of this article is to help you figure out how much to spend on a car payment. Throughout that explanation, we got into the weeds on the parts of an auto loan and how you can use those to your advantage or what you need to watch for.

When it comes to car shopping, there are a few other big items I would encourage you to consider to help manage the payment and allow yourself to get the exact car that you want.

First, I am a big believer in lightly used. By purchasing a car with 20,000-30,000 miles on it already, you are getting a car that should be well maintained by one previous owner, and you are not paying for that instant depreciation. For some new cars, the old saying goes, “It loses 20 percent the second you drive it off the lot.”

The second item I would tell you to consider to help get a better deal is to shop around. This holds true for almost any financial decision; it’s sometimes a pain to really shop around, but you’d be surprised at the money you can save. You may find a dealership that is one sale away from a huge bonus and ready to wheel and deal on pricing.

An auto loan is a much shorter term than a mortgage but is also a bigger commitment than a 12-month lease. The dollar amount is typically less, but the money you spend on a car payment is likely going to be a big chunk of your monthly budget.

You can always be flexible to make something work but try to remember that less is sometimes more with a car. If it runs well and gets you from A to B, just be happy. I try to view a car as a luxury and never want to have a payment, but for some, that is just impossible (and that’s okay). Do your homework on what you can truly spend, hold yourself to that number and everything will work out just fine.