“It’s easier to fool people than to convince them that they have been fooled.”

-Mark Twain

Understanding a company’s revenue streams and how they generate them remain important parts of analyzing companies. A company’s revenue recognition policy will help investors understand how and when they generate revenue.

Each business operates from a different business model. For example, Salesforce generates revenue from subscriptions, but when do they recognize a transaction, and how does it impact cash flows?

Or, if you look at insurance companies, they recognize revenue at a different rate than SaaS companies. Most of us recognize how Walmart generates revenue, but others offer more opaque business models.

We can read through a company’s financials to determine how it recognizes revenues. They will tell us how, from SaaS to banks.

In today’s post, we will learn:

- What is Revenue Recognition?

- What Are the Five Revenue Recognition Criteria?

- What is a Revenue Recognition Policy?

- Why is Revenue Recognition Policy Important?

- Examples of Revenue Recognition Policies

Okay, let’s dive in and learn more about revenue recognition policy.

What is Revenue Recognition?

A generally accepted accounting standard (GAAP) called revenue recognition specifies the circumstances when recognizing revenue and how to account for the revenue. When a customer has received a product or service, and the monetary amount passes to the business, they recognize revenue.

The foundation of any corporate performance is revenue. The sale is the keystone. Regulators know how alluring it may be for businesses to stretch the boundaries of what makes up income, particularly when not all cash is collected until the task is finished.

Attorneys, for instance, bill their clients according to billable hours and then present the invoice. Construction managers bill their clients by the percentage of completion.

Revenue accounting is quite simple when a company sells a product and they recognize the revenue when the customer makes a sale. However, accounting for income can become challenging when a business takes a long time to develop a product. We can ignore the revenue recognition principle in many circumstances.

Analysts prefer the adoption of industry-wide standards for revenue recognition by all companies. A standardized revenue recognition rule makes it easier to compare similar businesses when we look at line items on the income statement.

A company’s revenue recognition policies should not change over time. Keeping the policies consistent allows for analyzing and examining past financial data for seasonal trends or discrepancies.

“The revenue recognition principle of ASC 606 requires that revenue is recognized when the delivery of promised goods or services matches the amount expected by the company in exchange for the goods or services.”

Investopedia

The accrual accounting standard, known as the revenue recognition principle, states that companies must record revenues on the income statement in the realized period, not when they receive the cash.

For example, SaaS companies realize revenue when they receive the payment, not when the customer receives the product or service. Earned revenue represents the money spent on goods or services rendered.

For companies to include revenue in the accounting period, the company must have finished products or almost finished. Also, the company must be able to assure others they will receive payment. The account principle of matching also plays a part here. We need to match the revenues with the costs to create the revenue in the same period.

What Are the Five Revenue Recognition Criteria?

The Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB) released Accounting Standards ASC (606) in 2014. The ruling covers revenue from contracts with customers. I know it is a lot of acronyms, sorry.

ASC 606 offers a guide for recognizing revenue from contracts with customers. For example, this ruling impacted companies like Netflix, Salesforce, and Adobe.

The previous rules focused on industry-specific policies, creating a fragmented system of rules. The new version of revenue recognition offers a more industry-neutral stance and transparency.

ASC 606 allows for better comparisons across industries with standardized revenue recognition rules.

ASC 606 provides five steps companies need to satisfy the updated revenue recognition rules.

- Identify the contract with the customer.

- Identify contractual performance obligations.

- Determine the amount of consideration/price to a contractual obligation.

- Allocate the determined amount of consideration/price to the contractual obligations.

- Recognize revenue when the performing party satisfies the performance obligation.

What is a Revenue Recognition Policy?

The recognition revenue policy represents a document that recaps the company’s revenue process. Your next question might be, “Why do we care?”

Fun fact: the most common type of fraud remains improper revenue recognition. Over 43% of company fraud stems from improper revenue recognition. The tech sector represents the largest segment committing fraud at 17%.

For example, in 2020, Wirecard, the German fintech firm, reported a fraudulent income of 1.9 billion euros.

To help ensure revenue remains recorded properly, the SEC helped authorities create the ASC 606 ruling we discussed earlier.

When working through the financial statements, we can read the notes, which include revenue recognition.

The notes will contain eight keys to look for to ensure the company reports revenue in the right way:

- Description of the performance obligation.

- Contract arrangement for the performance obligation.

- Information regarding economic factors that impact the nature, amount, timing, and uncertainty of revenue and cash flows of a performance obligation.

- Timing of the transfer of performance obligation to the customer.

- Payment terms for a performance obligation.

- How the timing of satisfaction of the performance obligation relates to the typical payment timing.

- Obligation for returns, refunds, or types of warranties.

- Determine whether the company is a principal agent for the performance obligation and how they make the determination.

Let’s define a few of these terms a little deeper.

What is a performance obligation?

The unit of account for which revenue recognition is a performance obligation. A promise to transmit a specific commodity or service to a customer is known as a performance obligation.

It can be challenging for a business to (1) identify the actions it is conducting that qualify as promises to provide goods or services and (2) ascertain which promises are distinct because contracts with consumers sometimes involve many promises.

To determine whether a promised good or service is unique and hence subject to a separate performance obligation, an organization should respond to the following two questions:

- When used independently or in conjunction with other easily available resources, can the client profit from the good or service (i.e. is it capable of being distinctive)?

- Is the promise made by the party to provide the good or service distinct from other promises made in the contract (that is, is the good or service unique within the context of the contract)?

The promised good or service (or bundle of goods or services) is only distinct and, hence, a performance obligation where the affirmative response to each of the questions above is true.

An entity must combine goods or services until it finds a bundle that meets the two revenue recognition requirements for recognizing a particular good or service.

Companies can answer the first question easily, but this is not always true. The answer to the first question is affirmative if an entity sells a good or service on its own or if it can combine the good or service with another good or service that the entity (or another vendor) sells.

What matters is whether a customer may obtain some financial gain from the product or service or in conjunction with other accessible resources.

The second question is more difficult to respond to. For an entity to determine whether its promise to transfer a good or service is identifiable from other goods or services in a contract, the company must determine whether the nature of the promise is to transfer each of those goods or services or, instead, to transfer a combined item or items to which the promised good or service is an input.

Why is Revenue Recognition Policy Important?

According to the revenue recognition principle, an essential component of accrual-basis accounting, businesses must record revenue as they earn it instead of when paid. Because it directly affects the reliability and consistency of a company’s financial reporting, accurate revenue recognition remains crucial.

We have seen some of the worst accounting scandals over the last two decades. Companies like Enron, Worldcom, and Lehman Brothers remain names many outside the investing world recognize.

They recognize them because of the fraud each company committed. Not all of them included fudging numbers via the income statement. But it highlights the importance of believing the financial statements we read and base our investment decisions on.

Waste Management committed earnings fraud in 1998 by reporting over $1.7 billion in fake earnings, which began with mis-stating income.

Typically, fraudsters attempt to inflate the company’s value to make it more attractive to investors. Some do this to attract investors, others to receive bank loans, and many to justify large salaries or trigger stock options.

Greed remains the typical driver of fraud, and rooting it out by creating easy, transparent accounting rules such as ASC 606 helps investors.

Some typical types of financial statement fraud include:

- Overstating revenue

- Fictitious revenue and sales

- Timing differences

- Inflating an asset’s worth

- Concealing liabilities or obligations

- Many, many more

Because of a few bad apples, we need to make reading the revenue recognition policy a part of our investment process. Reading through those policies will help you understand the business’s operations and how they generate revenue and spot any questionable revenues.

A typical warning sign of possible fraud for revenue manipulation is rising revenues without corresponding cash flows growing. Another sign of possible issues is when competitors are struggling, but company A continues to see growing revenues.

The bottom line: we need to read and understand the revenue recognition policies of most companies we want to buy.

For example, you can exclude companies such as Home Depot or Walmart. When we buy a product from Walmart, they record the sale. These types of businesses remain obvious and don’t require much deep thought.

Instead, companies like Salesforce or Netflix generate revenues via subscriptions, requiring more examination. I am not suggesting any of these companies do anything wrong. Instead, I want you to realize the way they take in money is a bit more opaque.

Examples of Revenue Recognition Policies

Let’s look at several revenue recognition policies to determine how they generate revenue.

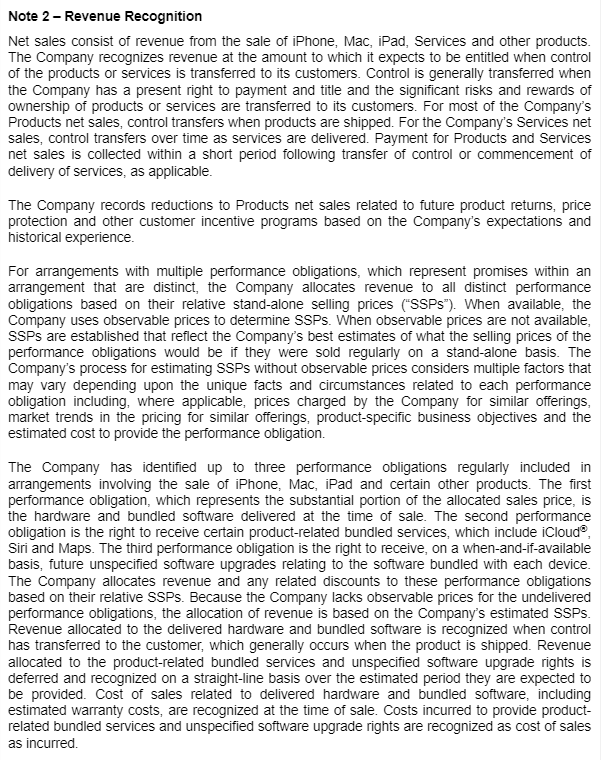

A great first example is how Apple recognizes revenue from sales of iPhones, along with several obligations they operate.

We can see Apple receives payment for their iPhones, Macs, iPad, and others from direct transfer from Apple to the customer when exchanging cash for control. At the point of transfer from control to the customer, Apple recognizes a sale of their iPhone.

Simple, easy to understand. But what about Apple’s other products or services?

Regarding the sales of their iPhones, for example, they observe three performance obligations:

- They must deliver hardware and bundled software at the time of sale of the iPhone.

- Delivery of certain product-related bundled services, including iCloud, Siri, and Maps; all complimentary but with add-on revenue potential.

- At the time of transferring control, Apple commits to deliver software updates related to the bundled software on each device.

Apple also delivers services such as Apple+ TV and iTunes. The company recognizes those revenues on a deferred revenue basis which they recognize on a straight-line basis, meaning they recognize the revenue when we pay for our subscription and deliver access to Apple+ TV.

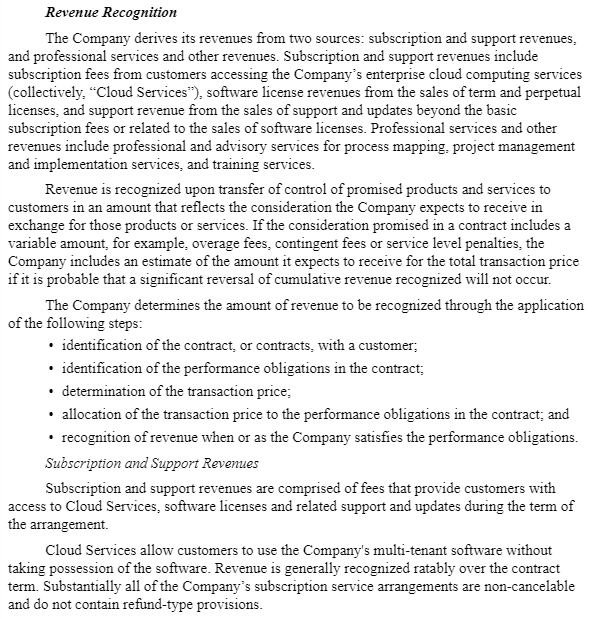

Next, let’s examine Salesforce’s (CRM) revenue recognition policy, as they generate revenue differently from Apple. Salesforce will provide a great example of how complicated the subject can become.

Below is an excerpt from their latest 10-K, dated 3/11/22.

First, we can see Salesforce recognizes revenues from two sources:

- Subscription and support revenues

- Professional services and other revenues

The subscription revenues and services stem from fees the company charges customers for access to Salesforce’s enterprise cloud services, software license revenues, and support. The professional services apply to process mapping, project management, and implementation.

As with Apple, the company recognizes revenues from the transfer of control from Salesforce to the customer. For example, the fees Salesforce charges customers are recognized when they provide access to their cloud services.

But in the case of any long-term contracts, they recognize the revenue ratably over the length of the contract. Typically, they invoice the customer with 30-day terms, and once they pay after 30 days, Salesforce recognizes the revenue.

Depending on the control transfer status, they recognize the invoiced amount in accounts receivable and in unearned revenue or revenue.

So, simple, by and large, but more complicated than Apple.

Investor Takeaway

When we analyze any company, understanding the business model remains crucial. Along with understanding the business model is how the company generates revenues. We need to understand which products or services drive growth for the company.

Along with those understandings, we need to understand how the company recognizes a sale, partly from timing and prevention aspects.

Financial fraud can occur from many different angles. Unfortunately, bad apples come in many different flavors, and sometimes they offer creative ways to cheat.

By reading and understanding how Netflix recognizes revenue for offering its streaming services, we can better understand its revenues and the timing of revenues. But we can also better understand the financials and provide some insight into fraud prevention.

And with that, we will wrap up our discussion regarding the revenue recognition policy.

Thank you for reading today’s post; I hope you found something of value. If I can be of any further assistance, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave