Now is as timely as ever to discuss the importance of an Emergency Fund, and if you don’t have one currently and are wondering how you can get one going, don’t worry – I’ll show you how to begin your starter Emergency Fund.

First off, what is an Emergency Fund? An Emergency Fund is just that – it’s a fund that is used for emergencies. If you or a spouse loses a job, if you have some unforeseen major health expenses, if a family member is in major issue and you need to help provide for them – emergencies only.

Maybe a better way to describe it is to say what an Emergency Fund is not – it’s not for when you get a flat tire, it’s not for when you want to take a vacation, it’s not for when there is a downturn in the market and want to invest like we’re experiencing right now!

An Emergency Fund is for emergencies ONLY!

The point of the Emergency Fund is to cover yourself if crap hits the fan. If you invest it in a market downturn then sure, that might be great long-term, but what if you were to invest half your Emergency Fund right now and then you get laid off a month later, after the market has gone down even further?

The point of the Emergency Fund isn’t to be the most optimized use of your money – it’s to have it in times of dire need. This is something that was really hard for me to fathom at first because I am such a numbers oriented person it was very tough, conceptually, to put money into a place where it was just sitting there, not really capitalizing on the potential gains that were out there.

The mindset that I took that finally put me over the edge was trying to envision what I would do if I lost my job and didn’t have an Emergency Fund – I’d likely have to pull money out of the market and pay some major fees, as well as taxes for selling my stocks, and that just seemed like an awful situation.

I’d rather just have the money sitting there, ready for my use, if I ever truly did need it.

So how much do you need? A lot of people will say that you need 3-6 months of expenses locked up, and I think that’s a fine rule of thumb, but it really just depends. But let me show you the steps to how you should figure it out:

1 – Determine the bare bones of your monthly expenses

What I mean by ‘bare bones’ is the things that you have to pay for every month. This doesn’t just include fixed expenses like your mortgage, car loan and student loans, but also things that are variable, but you have to buy, such as groceries, gas for your car, and your electric bill.

Cable? Cut it!

Gym membership? Gone!

Eating out? Adios!

Of course, nobody wants to lose these things from your lifestyle, but if you were to lose your job and you had literally $0 of income coming in, what would you do? Would you spend $100/month on cable if it meant you had to take that money from another category like groceries? Hopefully not!

If you’re budgeting your money, then it should be pretty simple and quick to find your essential monthly expenses. If you aren’t then I highly suggest you start budgeting your money ASAP, not only for Emergency Fund purposes but also just because there is no better way to get on your path to financial autonomy than there is with a budget.

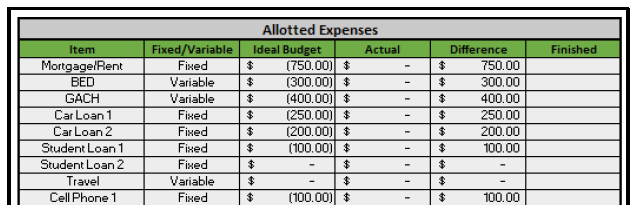

The screenshot below is a sneak peak at the Doctor Budget spreadsheet tool that shows some the expenses that you might experience, and how you can simply change the ‘Ideal Budget’ to 0 if it’s something that you can cancel out that month if things get tough, like ‘Travel’:

Let’s imagine that your monthly expenses are $2500 – what now?

2 – Determine how many months you need to have saved up for in your Emergency Fund

This is the hardest part of the Emergency Fund. Essentially, you need to look at many different factors and think about what is best for you. Some of the things that I consider are:

- Income

- You are the only income-producing member of your

family

- If so, assume you’ll lose your job and have $0 of income.

- What will you do? How long will you wait and have $0 of

income?

- Will you spend 6 months trying to find a job equivalent to what you had, or will you download uber that day and start having some sort of supplemental income coming in.

- Will you file for unemployment?

- What is the unemployment in your state?

- You are in a two-income household

- Who is more likely to lose their job?

- Is that the higher or the lower income?

- Is it unrealistic to think you both might lose

your job?

- If it is unrealistic, do you want to assume you lose the higher income job for a more conservative look?

- Who is more likely to lose their job?

- You are the only income-producing member of your

family

- Family

- Who relies on the income in your family?

- Is it just you? Spouse? Children?

- The more people in your family, the more months that you should have set aside for an emergency

- Is it just you? Spouse? Children?

- Who relies on the income in your family?

These are really the two main factors that you need to understand when you’re figuring out your Emergency Fund. As I mentioned before, let’s imagine that your monthly expenses are $2500. Let me outline my thought process for how I would shape my personal Emergency Fund if I was:

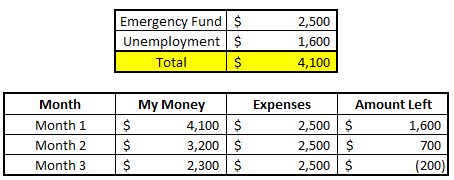

Single – I would have 1 month saved up, so $2500. I know that’s very low compared to all of the suggestions of 3-6 months, but my reasoning is this:

- I would file for unemployment. So, I would only need the $2500 to cover me until I got that money, which is usually about half of your income and capped around $500-$600/week, based off your state.

- While I was on unemployment, I would immediately start looking for other jobs to help cover my expenses, both full-time and also part-time, like Uber, delivering groceries, blogging, literally anything to help cover the expenses. If my unemployment was $400/week, then I could theoretically last for not even three months:

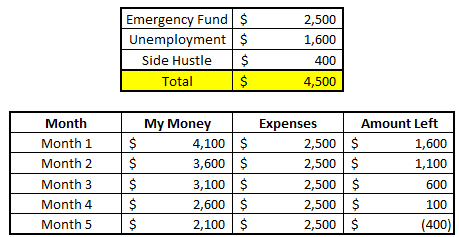

But, if I was willing to work a side hustle, assuming it didn’t void my unemployment, and it brought in $100/week, then it would extend the amount of time my money would last drastically – from less than three months to over 4 months.

Might not sound like a lot, but that essentially doubled my time.

Married with two incomes – I would have 3 months saved up, minus the lowest income. So, if the lowest income was $1000/month and our expenses were $7500, then I would make sure we had $4500 ($7500 – $4500). I know that’s very low compared to all of the suggestions of 3-6 months, since I’m still assuming an income, but my reasoning is this:

- I’m assuming we wouldn’t both lose our jobs. If I thought this was realistic, I would assume $0 income and have $7500 saved up.

- I’d use the same thought process as above with unemployment and a side hustle. To be honest, this mentality will never change with me, and it’s a mentality that I hope a lot of you too! When things get rough, buckle up, and let’s get through this!

Married with two incomes and children – I would have at least 4 months saved up, likely more! When a child is relying on you, it’s a bit different than a spouse or just yourself.

You’ll inherently do whatever it takes for that child so it’s not the time to be “skimping” on your Emergency Fund. You need to make sure that you have an adequate amount of money saved up to protect your child at all costs.

Now, the way that I approach this is to think what I would have to pay if we did lose both our jobs. So, let’s say the formula might be: Months Needed * (Monthly Expenses – Child Expenses that are no longer needed). What does this mean?

Primarily, daycare.

If you and your spouse are at home 24/7, you should probably stop paying for daycare and watch your child, potentially saving up to $200/week, or even more in some cities. Daycare isn’t cheap, and if you don’t see both you and your spouse getting back to work anytime soon, then you should stop.

I know that some daycares take forever to get into, so it might not be that simple if you think you’re going to both get jobs soon, so that’s just another factor that you’ll want to take into account when planning your Emergency Fund.

So now that you’ve decided your Emergency Fund amount, what do you do with it? I think it’s worth it to consider a high-yield savings account like Ally, especially since you’re likely going to have this Emergency Fund for your entire life.

Even a small increase in savings account APR can result in large gains, like my personal Fifth Third savings account that was .01% interest vs. Ally, which is 1.5% APR now. It takes a couple days to get your money out of Ally, so I still do keep some in my Fifth Third account for immediate access if I need it, but 80%+ is in Ally so I can optimize but also have my money if that emergency really does occur.

In today’s world with all of this coronavirus uncertainty, things are extremely scary. It’s more important than ever to have an Emergency Fund and if you don’t have one, you need to start now.

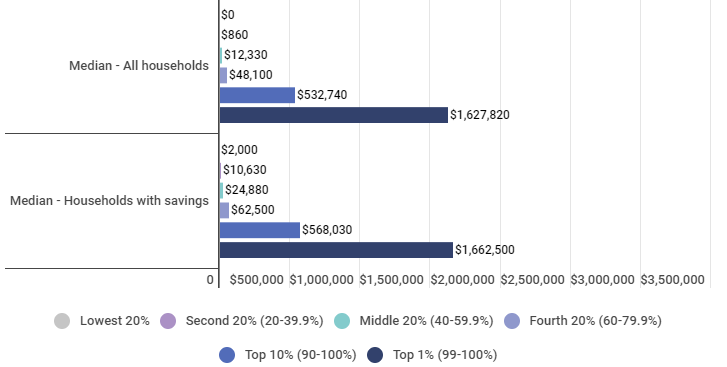

Per Magnify Money in the graph below, the based off the median household (which is really the best way to find a true average and throw out outliers, but sorry lol), 40% of households have under $860 in savings. That is not good.

$860 is only sufficient if your monthly expenses are $286.67, which if they are, please let me know how. In other words, these people do not have an adequate Emergency Fund. This is a terrifying statistic to me. Please, please, try to build this buffer up a little bit or you’re going to be in serious trouble if something ever was to occur.

Want to know what my recommendation is? A lot of you are about to get a $1200 stimulus check in the mail, and maybe some more in the future. The nature of the stimulus is for us to spend that money to help the economy but if you only have $860 in savings, like 40% of the US has, then take that entire $1200 and save it. Put it into your Emergency Fund and never touch it again until you need it for EMERGENCIES ONLY!

Look, I get that the stimulus isn’t meant for us to save the money, but you need to look after yourself first and foremost and building up that Emergency Fund is essential.

If you can get your savings from $860 to over $2000 with the Stimulus Check, then you just got a huge bump in the amount of time you can last without going into debt, right?

Once you do that, take the time to really think about your situation. What sort of household do you live in, income wise? Are you planning for the worst? Are you being as safe as you should be to protect yourself, your spouse, your family? Are you planning to file for unemployment or work for some supplemental income until you get a new job? Do you even have any retirement savings you could take out if you absolutely had to?

At the end of the day, it’s a personal decision – you have to assess the risk and the alternatives to properly understand how much you need to have saved up. So, is 3-6 months an appropriate recommendation? As a blanket, sure.

But if you’re wanting to really make sure that you’re optimized and are properly planning for the future, then you need to get much more specific than that.

As with anything in the personal finance world, this really comes down to knowing your numbers and being able to track your potential exposure. Don’t be lazy – your family’s livelihood might depend on it.