Long story, short, the answer is yes – you are going to have to pay taxes on reinvested dividends. While there are a ton of advantages to having your portfolio set up for Dividend Reinvestment Plans, or DRIP, tax avoidance is unfortunately not one of them. But don’t be discouraged – if you buy and hold, you’re going to be just fine!

As they say – nothing is as certain in life as death and taxes and guess what, that certainly applies to your dividends as well. The good news is that even though you’re receiving a dividend, which is technically considered a form of income as your stocks are paying out a portion of their earnings directly to you, there are actually ways that you can avoid paying your entire income tax rate and save a little bit of cash – you just need to be knowledgeable and understand how to take advantage!

Like I mentioned, you are going to have to pay some tax, but the question is, how much tax are you going to be on the hook for?

Well, that question is one that comes down to one overarching question – are the dividends considered qualified or ordinary? Chances are, you have no idea, and that’s completely fine! Let me breakdown the key differences for you.

The way that I would think of it is that all dividends are considered ordinary, but some meet certain qualifications that then therefore make them qualified. So, they’re all dividends but can become qualified if you meet certain criteria.

To be a qualified dividend, they must:

- Dividends must be paid by a US Corporation or a qualified foreign corporation

- Since you’re likely buying shares of a company on a publicly traded brokerage platform like Fidelity, Schwab, TD Ameritrade, or even Robinhood, you’re going to be completely fine.

- You must hold the stock for at least 60 days during the 121-day period that includes 60 days prior to the ex-dividend date, the ex-dividend date, and 60 days after the ex-dividend date

- So, if the ex-dividend date is on 7/1, then the 121-day window would range from 5/2 (60 days prior to ex-dividend date) to 8/30 (60 days after the ex-dividend date).

The rules are not that hard to follow, truthfully, especially if you’re a long-term investor like we are. Even if you were to buy the day prior to the ex-dividend date (so you got that dividend!) and then held on for the long-term, you’d still qualify because you held the stock for the 60-day period after the ex-dividend date.

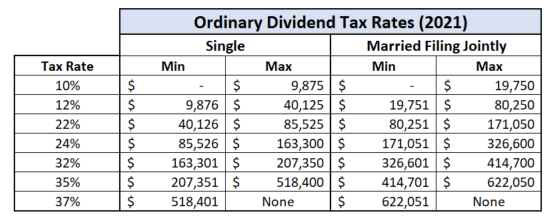

Now, the question that is likely coming into your mind is what the impact of this really is to you. Well, first let’s look at the Ordinary Dividend Tax Rates in 2021, otherwise known as your normal income tax rates:

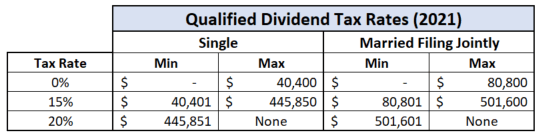

Hopefully none of this is a surprise to you! Now let’s look at the qualified dividend tax rates in 2021:

The first thing that stood out to me was that these tax rates are the exact same as long-term capital gains, which is the tax rate that you’re going to pay if you hold shares of a company for a year or longer.

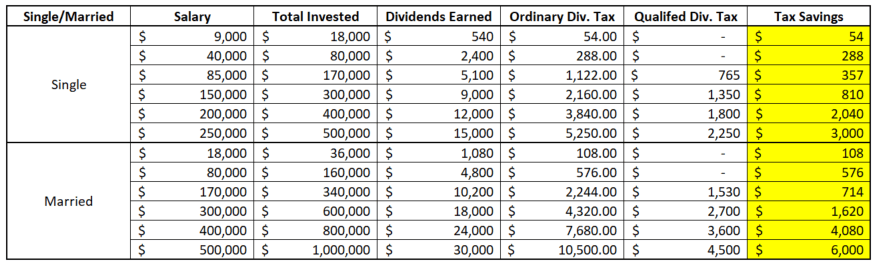

Obviously, the tax advantage is substantial, but just how substantial is it going to be? To examine more, let’s look at a few different scenarios to really understand the impact on your taxes for an ordinary dividend vs. qualified.

Essentially what I did was I took 6 different situations at various incomes, one in each of the ordinary tax brackets, and calculated the total amount of dividends that you were likely going to have to pay on an annual basis. To do so, I had to make a few assumptions:

- I assumed that your total amount invested in the stock market was going to be 2X the salary. Of course, that may be high or low but it’s an assumption that I made.

- I assumed an average dividend of 3%. That is slightly higher than the S&P 500, but many of the heavy hitters in the S&P do not pay a dividend (such as Tesla, Amazon, Facebook, Google, and Berkshire). In fact, the top 10 holdings make up 27% of SPY, a great S&P 500 ETF, and half of that doesn’t pay a dividend. So, since a lot of us are long-term dividend stockholders, I opted to use a slightly higher yield of 3%. Now, remember that some of these big companies in the S&P 500 do pay great dividends such as Apple and JNJ!

After making these assumptions, you can see the following tax savings in the chart below:

Pretty substantial savings, right? Even for the single filer that is only making $9K/year, that tax savings is worth .3% of their total investing portfolio. .3% might not seem like some astronomical amount, but it can really add up quickly, especially as your dividends continue to compound year over year.

I ran through another scenario in the chart below that I think is one that is extremely realistic. It considers the following assumptions:

- Single person currently making $50K/Year

- $0 Saved/Invested currently

- Will plan to start investing 15% of their salary/year

- Will get an 8% return in the stock market (100-year average is over 10% so this is a conservative look)

- Average Dividend Yield of 3%

- Will receive a 3% raise on their salary each year

- Dividends are not reinvested and rather held in cash.

- While I always think that dividends should be reinvested, this makes it simpler to comprehend for the purposes of looking at taxes.

When I input all these variables into Excel, the results are astonishing – look!

As you can see, not only are you going to have to pay a lot of stinkin’ taxes, but the tax savings is HUGE when you get to the end of these 40 years of investing.

In the grand scheme, $66K isn’t an amount that’s going to make or break your retirement goals, but it is a pretty nice amount for doing nothing other than holding onto these stocks for that 60-day period to make sure that they classify as qualified dividends rather than ordinary.

If you’re the type of person that lives and dies by the 4% rule, or even just someone like me that really likes to use it for planning purposes, then you basically just gave yourself an extra year of income if you’re planning to spend $66K/year in retirement, meaning you might be able to actually retire multiple years earlier…for doing literally nothing other than buying and holding.

Tax advantages are one of the main things that I really like to talk about when we start getting into the weeds of investing and retirement discussions because I think that so many people are leaving tax advantages on the table.

If you’re using a 401k, IRA, and HSA for your retirement planning then I applaud you – you’re definitely doing a great job! But if you also have some money in a normal brokerage account, that’s where your tax planning really is going to make a huge difference.

The benefits of a Roth IRA or Roth 401k is that you’re never, ever going to have to pay taxes again on that balance as long as you wait until you’re 59.5 to start withdrawing those funds. The beauty of that is that you’re tax-advantaged and you can do literally anything you want without having to send that check to Uncle Sam at the end.

Yes, you can buy a stock for 1 day just to get the dividend and then sell it immediately and not have to pay that tax because it’s in a tax-sheltered account. I mean, I’d highly advise against doing that for other reasons (such as the fact that the stock is likely to drop that same day by the same amount of the dividend) but that’s for a different blog post.

The one thing that I really want to caution you on is to never make long-term/permanent types of decisions simply to take advantage of a tax-advantage. So what exactly do I mean by that?

Well, I mean that you shouldn’t basically start moving stocks and funds around from account to account just to take advantage of tax-benefits, especially ones that might be likely to change. Let me explain exactly what I mean with a real-life situation from yours truly!

As you may know, I have various accounts that have different purposes in my portfolio. I find that by doing this, I can more easily segregate my emotions into different philosophies and not get drug down by certain companies or sectors doing great or getting crushed.

So, because of this, I have many accounts with different purposes, but the two that I really want to focus on are a brokerage account called “Dividend Aristocrats of the Future” and then my Roth IRA.

Essentially my goal is to always pay as little of taxes as possible, as should anyone’s goal be. Now, you may know that I am personally a big fan of having some speculative investments in your portfolio, especially if you’re a young investor that has plenty of time left in their investing career. I think that taking smart, well-calculated risks is one of the best ways to jumpstart your path to financial independence, but that’s just my opinion!

On the other hand, I also think that having some great, consistent dividend-paying companies is a fantastic thing to have in my portfolio to balance it out. I have read and studied dividend kings quite a bit and I actually have some companies that I like to have as Dividend Aristocrats of the future. Not many, but there are a few that are in that portfolio that I think will compound fantastically over time for me.

By nature, the speculative investments can change their outlook quickly, meaning that I may be selling more regularly than with a different stock, so I would naturally be incurring more taxes. To help protect myself from this, I put my speculative investments in my Roth IRA because I will pay the taxes upfront and then never have to pay taxes on them again, at any point in my life, even if I receive an ordinary dividend.

On the other hand, my Dividend Aristocrats of the Future account is simply held in my brokerage account. Sure, I am going to have to pay taxes on those dividends that I earn each year, but because my thought process is to try to find stocks that I can literally buy and hold forever, it makes sense to put them in a taxable account because I am getting that extra incentive for holding onto the stocks longer than I might a speculative investment.

This isn’t some magic trick that is going to allow you to get rich quick, but it’s going to help you get rich on this slower, realistic, sustainable path that we’re all trying to teach.

I’ve learned over time that there really isn’t some magic sauce to get us to get rich quick, but there are many things that we can do to simply make our portfolio a little bit more optimized than what it might currently be, and over time, all of those little adjustments are going to make a really big deal!

As I mentioned, DRIPping your dividends unfortunately isn’t going to protect you from having to pay a tax on the dividend that you receive, but I still think that it’s a fantastic option for the normal investor. I have many of my different accounts setup to DRIP every time that I receive my dividend payments each month because I think it maximizes the amount of time that my money is in the market and working for me!

But don’t just take the advice from me – take it from the DRIP King, himself!