Question for you: Do you know the most common form of valuation of stocks? Not discounted cash flows, dividend discount models, but relative valuation. Never would have guessed? I know I was shocked when I discovered this fact. Most analysts’ reports of the sell-side variety use this type of valuation.

Discounted cash flows remain difficult, requiring many different estimates to complete those valuations. The fact of the matter is no valuation method is without issues.

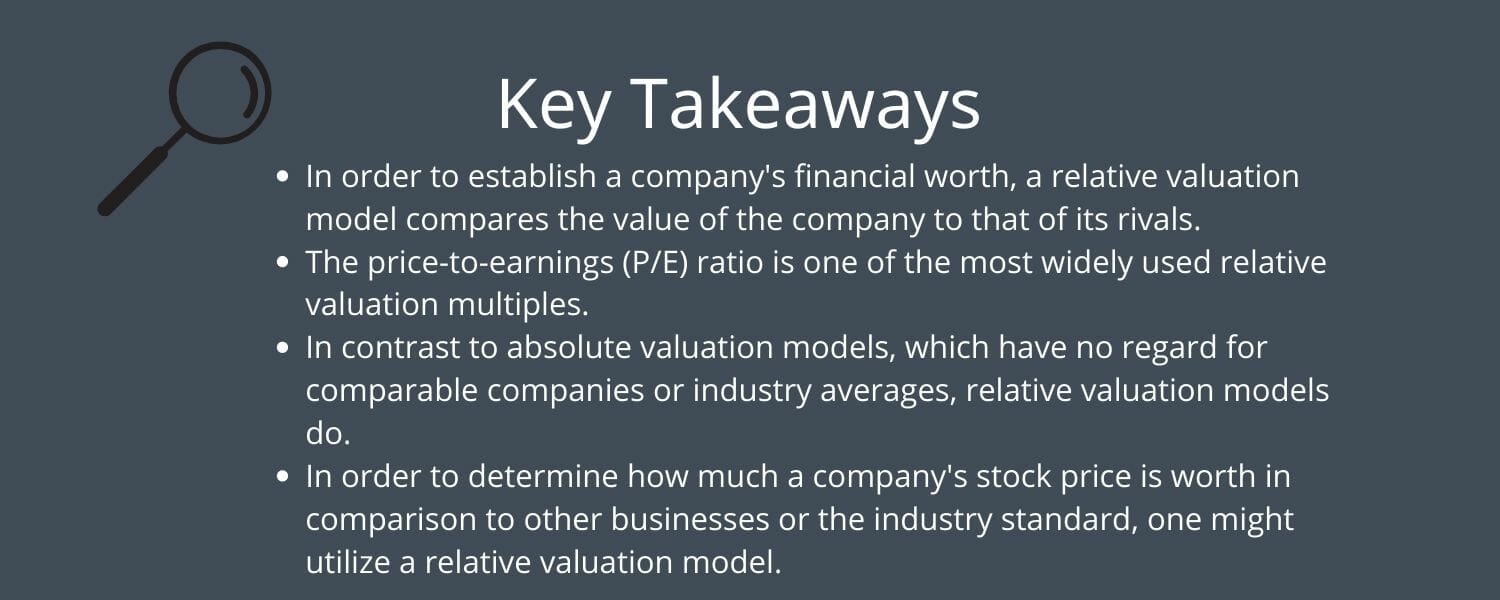

However, relative valuation offers one of the easier methods to use, provided you account for your variable and understand the metrics used; plus, the method remains great for quick valuations to give a quick and easy way to determine whether the company is worth more analysis.

An adage in the investing world goes something like this; an asset is only worth whatever someone else is willing to pay for the asset.

When valuing a stock, we have to remember it is a piece of a business, which we can forget when using relative valuation as it relates more to the price of a stock and tends to forgo other aspects of the business.

A side benefit of learning how to use relative valuation to find the company’s value is you can use the valuation basis to compare your other forms of valuation, such as a discounted cash flow, to see if your story remains off compared to the market.

In today’s post, we will learn:

- What is Relative Valuation?

- How Do You Calculate Relative Valuation?

- Examples of Relative Valuation in Action

- Pros and Cons of Relative Valuation

Okay, let’s dive in and discover all there is to learn about relative valuation.

What is Relative Valuation?

Relative valuation is a method of using comparable metrics, also referred to as comparable valuation. Some of the more common metrics used in this type of valuation include:

- Price to Earnings or P/E

- Price to Book or P/B

- Enterprise Value to EBITDA or EV/EBITDA

- Enterprise Value to EBIT or EV/EBIT

And many more; we will discuss this further in a little bit.

Using the relative valuation, we use the value of an asset compared to the values assessed by the market for comparable or similar assets.

There are many aspects of relative valuation that we need to take into account:

- We need to find comparable assets and assign market values for those assets.

- Next, we need to convert those market values into standardized values since we can’t use the prices as comparables, leading us to use price multiples.

- Finally, we need to compare the value or multiple for the asset we use to compare to the values for comparable assets, allowing us to determine whether the asset remains under or overvalued.

The value of most assets, from the house or car we buy to the stocks we invest in, is based on how closely they align with similar market assets.

How Do You Calculate Relative Valuation?

Using relative valuation, we find the value of an asset deriving from the price of comparable assets, which we standardize using a common variable such as revenues, earnings, cash flows, or book value.

We can use an average industry price-to-earnings ratio to value firms. The assumption remains that the other companies in the industry remain comparable to the firm we analyze. We can base all of it on the belief that the market continues correctly pricing those other companies, thus making the comparison correct.

Another example is the use of price to book, with companies selling at a discount to book value compared to other companies being considered undervalued.

We have many different examples of these examples, and the list of metrics or multiples used in relative valuation remains too great to list them all.

Unlike a discounted cash flow, relative valuation requires our faith in the market is right much more than searching for intrinsic value.

The allure of multiples is that they remain simple and easy for all investors to relate to them. Multiples are useful with many comparable companies, but they tend towards more difficulty with unique firms that don’t have a lot of comparables in their industry or businesses with little or no revenue or negative earnings.

Before we dive in and discuss using relative valuation to value a company, let’s briefly explore the standardization of value and multiples.

Standardizing Value and Multiples

Let’s think about the price of a stock for a moment; that price remains a function of the value of the equity and the number of shares outstanding in a firm. Because the prices of Mastercard and Visa aren’t comparable, we need to use standardized multiples to compare the companies.

We can use four basic multiples when using relative valuation, with many variations on those themes. The four main multiples are:

- Earnings multiples

- Book value

- Revenue multiples

- Sector-specific multiples

Consistency is the most important aspect of using any of these multiples or metrics we choose to use.

Every multiple we use has a numerator and a denominator. The numerator is either an equity value (such as a price or equity value) or a firm value (enterprise value, which is the sum of debt, equity, and less cash).

The denominator can utilize equity measures such as earnings per share, net income, or book value. Or we can use firm measures such as operating income, EBITDA, or book value of capital.

One of the key tests to run on multiples remains identifying whether both sides of the equation are defined consistently. What do I mean by this?

From Valuation by Aswath Damodaran:

“If the numerator for a multiple is an equity value, then the denominator should also be an equity value. If the numerator is a firm value, then the denominator should be a firm value as well.”

A perfect example of the consistently defined multiple is the price-to-earnings multiple. The price per share of the numerator stays an equity value, and the earnings per share of the denominator remains an equity value.

Likewise is the enterprise value to EBITDA multiple, as both numerator and denominator comprise both firm values.

An example of an inconsistent multiple in mixing equity and firm value is Price to EBITDA, which contains equity in the numerator and firm value in the denominator.

Another aspect of consistency; we must define a multiple. For example, using the P/E ratio. We have three forms of the P/E ratio:

So, when using the P/E ratio for any company, make sure the one you compare it to uses the same basis of P/E ratio; for example, if you value a company using the trailing P/E for your company, make sure to use the trailing P/E’s for all the company’s you compare. Otherwise, you risk mixing and matching different definitions, which could lead to errors in valuing companies.

The above example offers an especially glaring challenge in high-growth sectors where the values can make quantum leaps over the previous quarters, whereas the effects in a more mature industry like banking remain far more minimal.

The other mistake when using multiples is avoiding negative numbers or selection bias. For example, using outliers in averages can lead to large leaps in averages; huge P/E ratios can lead to extremely inflated P/E ratios for an industry; likewise, many companies with negative earnings can lead to extremely low multiples.

You have three choices to solve this problem. The first choice is to understand this bias and adjust your multiple to account for this. The other choice is to take all the market value of equity and income, including losses for all the companies in the group, and compute the price-to-earnings ratio for the group. The third choice is to use the median value of the P/E ratio, for example, of the group.

Again, we have no best choice, but rather however you decide, it is best to remain consistent; for my choice, I choose the median. But I reserve the right to change my mind at any time and go with the entire sector as a second option.

These are the consistency options I picked out, which I feel remain the most relevant to our discussion today; however, if you want to dig deep into the weeds on the subject of multiple definitions, then I highly encourage you to explore any of the relative valuations works Professor Damodaran has put out, including his books.

The Steps to Relative Valuation

The relative valuation method has several ways to go about valuing a company.

One is to find a company you would like to value, and then find a median for the multiple you would like to use for comparison and then multiply by its earnings, for example.

Let’s use a simple example to illustrate.

We want to use a P/E ratio to identify the value of a company.

- In an industry, identify five stocks similar to the stock we want to value.

- Assume the median P/E of those five stocks is 11.4

- The stock we want to value has an EPS of 2.5

- The intrinsic value of the said company would be:

- P = P/E x EPS

- P = 11.4 x 2.5

- P = $28.5

- The next step would be to compare the value to the median price of those companies and see how the value stacks up price-wise compared to those five companies.

Pretty simple, huh? You can use the same example to value companies using any multiple you wish across any industry, for example, software, banks, retail, real estate, etc.

The above example illustrates how to value the entire company encompassing all the elements that drive the earnings or revenue of the company.

Another option is to use the relative value of each component of the business to derive the company’s value. Also known as the sum of the parts valuation, which is extremely common in analysts’ reports, particularly sell-side analysts. I like this type of valuation because it helps determine where the value is derived from any given company.

Okay, let’s look at some real companies and relative valuations.

Examples of Relative Valuation in Action

For our first example, I would like to look at the big three of the wireless telecom world, Verizon (VZ), AT&T (T), and T-Mobile (TMUS), and we will use the current EV/EBITDA ratio as a comparison for all three companies.

Before I dive into the relative valuations of these companies, I want to share the data set that I use to find both the multiples and the sectors each company is located in:

Damodaran.com Multiple Data and Industry Data

All the sector data I will reference will come from the above; I highly recommend you check it out.

Getting back to our example…

The current EV/EBITDA for the telecom services sector in which all three companies reside is 6.61. To find the relative value for all three companies is to multiply that number by the current EBITDA per share, which I will list below:

- Verizon – 6.64 TTM

- AT&T – 5.6 TTM

- TMUS – 11.9 TTM

Now, let’s multiply each of these by the sector multiple and compare them to the current market price.

- Verizon – 6.64 x 6.61 = $43.89

- Current market price – $42.44

- AT&T – 5.6 x 6.61 = $37.01

- Current market price – $17.03

- TMUS – 11.9 x 6.61 = $78.66

- Current market price – $145.70

So, interesting results, according to the relative valuation, both AT&T and T-mobile remain undervalued by the market and closely valued in the case of Verizon

The next question is, are those values correct? The better question is to evaluate all aspects of the business and determine that value; the other option is to run both companies through a discounted cash flow valuation and check your value using that method. And finally, run all three companies through a reverse DCF to determine what growth rates the market is using to arrive at the price.

As with any valuation method, we have to determine how legitimate we find these values and decipher the factors that guide these values.

Let’s try the same process using the book values for a bank. Let’s look at the value of some of the big money center banks.

- Wells Fargo (WFC)

- JP Morgan (JPM)

- US Bank (USB)

- Bank of America (BAC)

- Citibank (C)

Using my chart to find the current price to book value, I find the value of 1.21. Now I will find the current price to book value for each bank, then multiply it by our book value per share to find the relative value.

- Wells Fargo – 1.21 x $41.51 = $50.22

- Current market price – $45.43

- JP Morgan – 1.21 x $85.67 = $96.37

- Current market price = $103.66

- US Bank – 1.21 x $32.90 = $39.81

- Current market price = $47.58

- Citibank – 1.21 x $89.62 = $108.44

- Current market price = $50.67

- Bank of America – 1.21 x $28.67 = $34.69

- Current market price = $34.94

Again, an interesting mix of results; at first blush, it appears that most of the sector is undervalued and quite wildly in a few cases. All of this makes sense because, as a whole, the banking sector was hit hard during the market crash in March and has slowly recovered at this point, unlike the Nasdaq.

Okay, let’s try one more example using business segments to determine a company’s value. For our example, I would like to stick with banks and analyze JP Morgan, breaking out each bank segment’s revenues and net income. Unfortunately, not every company does this, so it can be more difficult to analyze them, but JP Morgan does.

All of the numbers for the net income I am pulling from the latest 10-K from 2021 will be in millions unless otherwise stated. And then, I will multiply it by a comparable P/E ratio to determine the bank’s equity.

- Consumer & Community Banking

- $20,930 net income x 9.56 P/E = $200,090

- Corporate & Investment Bank

- $21,134 net income x 11.98 P/E = $253,185

- Commercial Banking

- $5,246 net income x 9.56 P/E = $50,151

- Asset & Wealth Management

- $4,737 net income x 11.98 P/E = $56,749

- Corporate

- $(3,713) net income x 9.56 P/E = $(35,496)

Now we add up all the numbers, and we arrive at an equity value of $524,679 billion in market cap compared to the current market cap of $349,474 billion.

What an interesting exercise as it illustrates where the company’s value resides and how much of an impact any changes, such as interest rates, might make to JP Morgan. I love doing that breakdown to determine what drives the value of each segment.

Okay, we have illustrated many methods to find value using relative valuation.

Let’s look at some of the pluses and minuses of using relative valuation.

Pros and Cons of Relative Valuation

The allure of using multiples remains the ease of use, which offers a much quicker way to value a company. In fact, as I mentioned before, almost 85% of all analysts use relative valuation when pricing firms.

Using the relative valuation to value a company is, in fact, pricing because we are using variables that are based on the price of the company, and we are comparing it to the price that the market assigns to a company.

Using comparables remains easy, but it can lead to misuse and manipulation, especially when comparing one company to another or a group of others. Our bias towards different companies or sectors can lead to subjective choices, and what you consider comparables, others might not. This leads to comparison errors as these assumptions about what you consider comparable are often unsaid.

Another issue with using multiples for valuation is it builds in errors that the market might be making in valuing any of the comparable companies.

For example, if the market has overvalued all computer software companies, then using these companies’ average or median P/E ratio will lead to us overvaluing the company.

The pros of using relative valuation are that it remains quick, easy to use, and gives you a great starting point to determine if you want to continue by digging to find an intrinsic value of the company.

As with any valuation technique, there are benefits and issues, but our job is to understand them and consistently deal with them.

Final Thoughts

Valuation is part art, part science, and relative valuation is part of that combination.

Plenty of assumptions remain built into using multiples to value a company. The biggest issue is that the market is always right and that every company you use for comparison remains correctly priced. We know this remains false, as many companies can face valuation challenges as markets ebb and flow.

I suggest using relative valuation as a guide to help you find undervalued companies and then use that information as a starting point for your further analysis.

Using discounted cash flows and reverse DCFs offer great ways to determine a company’s intrinsic value, plus where the market values the company’s growth.

The hardest part of calculating relative valuation remains determining the consistency of your multiples or ratios and then to determine the comparable multiples you will employ. Once you have those figured out, it is a breeze.

I encourage you to practice these methods with companies you understand and then branch out; you will find it easier with practice.

That is going to wrap up our discussion for today.

As always, thank you for taking the time to read this post. I hope you find something of value on your investing journey.

If I can be of any further assistance, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave

Dave Ahern

Dave, a self-taught investor, empowers investors to start investing by demystifying the stock market.