Updated 3/28/2024

The 401k is one of the most popular tools for investing for retirement because so many employers offer it. But, believe it or not, there’s some skepticism about whether it’s worth it. In this post, I want to dive deep into the 401k and explore the times when it’s the most beneficial and when it might be a hindrance.

Key Takeaways:

- A 401k is a fantastic retirement account with great tax advantages and employer-matching

- It is generally limited to mutual fund investment options

- You can build massive wealth in a 401k, even with a small salary, simply by starting early and investing consistently

- While a 401k is a great retirement account, it ranks third in my Financial Order of Operations for maxing out the account

In this post, I’m going to answer the following questions:

- What is a 401k?

- Is a 401k Worth Investing In?

- Is Your 401k Enough to Build Wealth?

- Is It Possible That a 401k Is Not Worth It?

- Do I Need More Than a 401k?

What is a 401k?

A 401k is an employer-sponsored retirement plan that allows people to sock away some money for their retirement before it even hits their bank account.

There are many quantitative reasons to like the 401k, but I think a major benefit is the psychological aspect. 401k savings are directly deposited into the account rather than the employee having to deposit them. Let’s be real: We would all forget to do it if it was a manual process.

Maybe you or I would remember since we’re both finance nerds but not everyone will.

62% of employers automatically enroll their employees in the 401k plan unless they decide to opt-out, and I think this is a fabulous thing for employees. When the employees are enrolled in their 401k, the funds will automatically come out of their paycheck and go into their 401k account through a popular brokerage firm like Fidelity or Schwab.

At that point, the funds are likely invested in a mutual fund or a target-date fund, neither of which I am a big fan of. However, when the alternative is doing absolutely nothing, I think they’re both great options for someone who otherwise wouldn’t invest at all.

The Advantages of a 401k

Many times, employers will offer a 401k match for their employees. In 2018, the average 401k match was 4.3%, meaning that if the employee made $100K/year and contributed $4,300, or 4.3%, then their employer would also contribute $4,300. Thus, the employee gets an immediate 100% return on their money, not counting all of that time it has in the stock market to keep growing.

You can’t beat a guaranteed 100% return anywhere else.

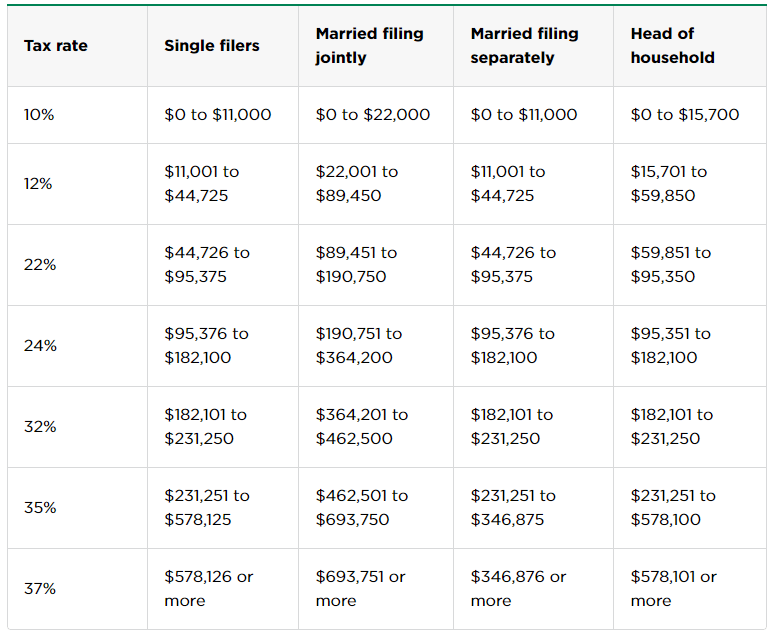

As if things couldn’t get any better, maybe the best part of the 401k is that they are heavily tax-advantaged. Most employers offer a Traditional 401k, meaning the money that goes in is all pre-tax, and some will offer a Roth 401k, where the money goes in after taxes are taken out.

So, if you select the traditional option, you can contribute up to $23,000, the maximum contribution amount in 2024, on a tax-free basis, which ranges up to 37% of your income in 2024. Let me be very clear here….

That means you make 37% ROI immediately by putting that money in a 401k instead of anywhere else. Considering the average year in the stock market gets you around 10%, I would take that all day, every day.

On the other hand, we have the Roth 401k, which means the money is taxed on the front end, but you never pay taxes on it again. This can be a great option for people who plan to have higher taxes in the future and want to get them out of the way now.

To summarize the tax scenario:

- Traditional – Avoid tax now, pay tax later. Better if you think your taxes now are higher than they will be later.

- Roth – Pay tax now, avoid tax later. Better if you think your taxes now are lower than they will be later.

Is a 401k Worth Investing In?

Yes.

Next question!

Seems like an easy answer but let me dive into the details and show you exactly why it’s worth investing in a 401k. Specifically, there are four main reasons, some of which I touched on previously:

1. Tax Benefit

The tax benefit is second to none when it comes to retirement planning. Some people will rave about the IRA, either Roth or Traditional, but the tax benefit is the same: either tax-free going in or tax-free coming out.

If you contributed $5K to a Traditional 401k every year, then you’d avoid the tax on the front end. If you were in the 22% tax bracket, that means that you’d save 22% on your taxes, so while you’re putting $5K into a traditional 401k, if you were to choose to have that money end up in your paycheck instead, you’d only get $3,900, effectively saving an extra $1100 each year.

If you had chosen to contribute to the Roth 401k, you’d pay those taxes up front, and then when you retired and withdrew the money from your account, you’d never have to pay taxes again on that money. But how much exactly would that be? Well, it could truly be hundreds of thousands of dollars that you can save.

Don’t believe me? I’ll show you the math later on!

2. Employer Match

The employer match is free money. If you were to get that average 4.3% on $50K for 30 years, you’re looking at $64,500 of free money from your employer.

And that doesn’t even account for the fact that your money is going to grow. That’s assuming that your $50K salary doesn’t increase at all and that the money just sat there, and let’s be honest – neither of those things are likely to be true.

3. Getting Started Early

The beauty of a 401k is that if you can get in the habit of contributing as soon as you start working, you’ll never notice that the money’s gone, and you’ll be able to maximize the most important benefit—time in the market!

If you start working at the age of 22 after college, that means you’ll have nearly 40 years, at a minimum, for your money to compound.

“But Andy, I’m not going to college, so I won’t have a ‘desk job’ and likely won’t have a 401k.”

Maybe I’d buy this in 2010, but we’re in 2024, and it’s the year of the employee. The labor market has never been hotter, with so many options to find a new job. Many companies that don’t have your typical 8-5 cubicle job offer a 401k, such as Chipotle, Macy’s, REI, Costco, Lowe’s, Staples, Starbucks, and others.

Take your situation into your own hands and find an employer, regardless of your education, that’s going to give you the pay and benefits that you deserve!

4. Hands Off Until 59.5

In a 401k, you are restricted from touching that money until you are 59.5 or older. If you do, you’ll have to pay a 10% penalty on your withdrawal.

Some might say this is a negative, but I think it’s a major positive. Charlie Munger once said, “The first rule of compounding: Never interrupt it unnecessarily.”

By being unable to touch your money until at least 59.5, you’re guaranteeing yourself many years of compounding for your 401k. You’re putting a major restriction in place to keep yourself from accessing this money and I think it’s one of the best parts of your 401k.

Do you know how sometimes your parents would set a bedtime for you that you disagreed with, but it was the best for you and your health? Well, this is a financial bedtime, so don’t you dare think about taking out money early because it’s simply not worth it.

Is Your 401k Enough to Build Wealth?

Uh….YES!

It is.

Not only can you build wealth simply by investing your funds into a 401k, but you have the benefit of the average employer giving matching contributions up to 4.3% as I mentioned previously. If you can simply just invest enough to get your employer match and start early, you can build up some pretty significant wealth.

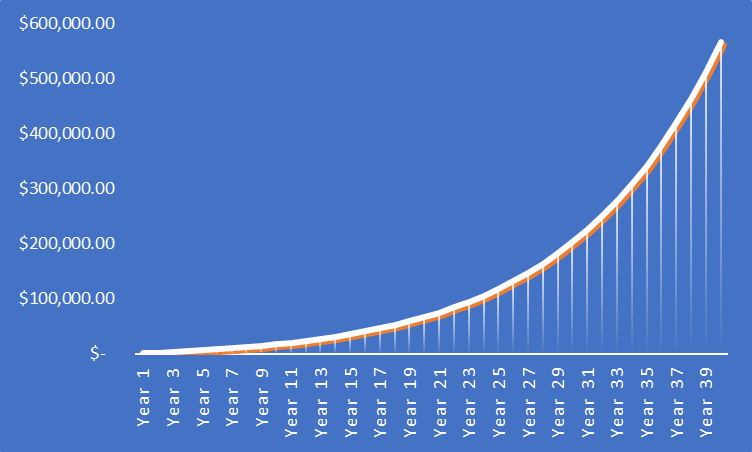

How much, you ask? Take a look!

As you can see, even if you’re making $20K/year now and can accomplish a 3% raise each year to essentially keep pace with “normal” inflation…then you’re going to have nearly $600K in 40 years!

Sure, 40 years is a long timeframe, but that’s why I strongly emphasize the importance of starting early, regardless of how much money you have.

If you can somehow find a way to just eek that % up to 8%, you will end up with nearly $1 million in 40 years.

That is astonishing when you consider that the TOTAL EARNINGS during that 40 years were just over $1 million.

So, is a 401k enough to build wealth? There’s no doubt about it!

Is It Possible That a 401k Is Not Worth It?

Honestly, no – I don’t think it’s possible that a 401k isn’t worth it. There are so many benefits that I think the 401k is a fantastic tool created to help you build massive wealth.

That being said, I do think there are some situations where a 401k might not be as beneficial as other situations.

Lack of Investment Options

One of those scenarios is if you want a larger variety of investment options. This could mean something as simple as investing in individual stocks or ETFs or even crypto. Maybe it’s real estate or maybe you want to fund a startup. The investment options are much more limited and typically only include mutual funds.

Now, some mutual funds in there will likely mimic your major indices and also have a semi-low expense ratio, so you’re truly not giving up much. I view this as a relatively small tradeoff for the massive tax savings, among other benefits, that you’re going to receive.

Take a look through your 401k investment options for a fund that tracks the overall market or the S&P 500.

Early Retirement

The other aspect where I can see a benefit to maybe not fully maxing out your 401k is if you want to retire early. In your 401k, you can’t access the funds before you’re 59 ½ unless you wish to pay a 10% penalty, so your 401k doesn’t help you a whole bunch if you want to retire before then.

In that case, I would be on board with you partially funding your 401k to at least get the company match and likely some extra, and then funding a brokerage account that offers you a little more flexibility.

One very important thing to remember is that “normal retirement” is encompassed in “early retirement,” so funding your 401k is still extremely important. If you want to retire by 50, then you should have a plan in place to fund your life for the 9.5 years before you can access your retirement accounts, but after that, it’s a free game to pull from the 401k, so utilizing all of the benefits would be extremely impactful.

Do I Need More Than a 401k?

This all comes down to what you want from your life. Do you want to retire early? Do you want to invest in individual stocks, real estate, etc.?

Mathematically, no – you don’t need more than a 401k. But realistically speaking, many other investment vehicles are fantastic options for you, and I highly recommend checking them out.

Specifically speaking, an HSA and an IRA. Those are the two most impactful retirement accounts you can take advantage of because they have so much flexibility. Below is the Financial Order of Operations that I implement:

1 – Max out 401k Employer Match

5 – Invest In a Brokerage Account

Steps 4 and 5 are starting to become more interchangeable for me because I want to retire early, so I am willing to not fully max out the 401k to put a little bit more in my brokerage to prepare for early retirement life. It’s nothing but a trade-off!

You just need to take a strong look at exactly what you want in your life, your current investments, and if you’re on track for retirement based on these saving money charts. At that point, you’re going to be more equipped to answer that question.

If you decide to go outside of your 401k and look for some individual stocks, I applaud you! We love to do that here at Investing for Beginners. Whether it’s teaching you how to value companies with the Value Trap Indicator or handpicking a new company to invest in each month with the Sather Research eLetter, we’re here to help!